10’000 Hours

Investment summary

My recommendation for Tyler Technologies (NYSE:TYL) is a buy rating. TYL is a leading software solution in a large market that is expected to continue growing, supported by strong secular tailwinds. As the leading player, TYL should be well positioned to benefit from this. In addition, the transition to cloud is well underway and should support TYL growth as cloud customers are economically more profitable.

Business Overview

TYL

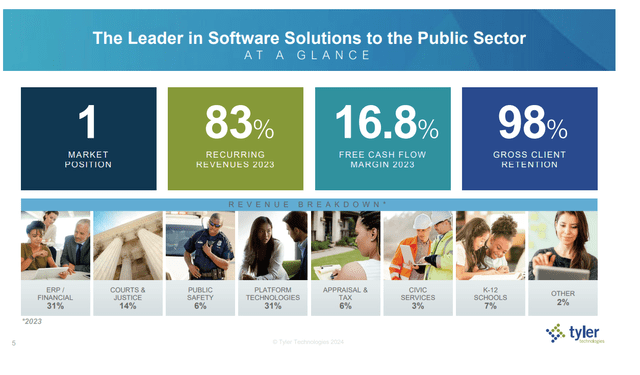

TYL provides software, hardware, and maintenance solutions primarily to the public sector in the United States, mainly to support the back-end functions. These solutions are broken down into main categories such as: financial management, planning, regulatory, and maintenance for the education entities and municipal courts; courts; justice and public safety; data and insights; appraisal and tax; land and vital records; property appraisal; development platform; and digital government and payments. TYL is the leader in the industry, and as of FY23, it has generated more than 80% of its revenue on a recurring basis.

Released on 24th April, TYL’s 1Q24 reported non-GAAP annual revenue growth of 8.6% on a reported basis and 7.8% on an organic basis. Gross margins expanded 130bps vs 1Q23 from 45.6% to 46.9%, driven mainly by the shift towards SaaS revenue. This, along with improved productivity, drove non-GAAP EBIT margin expansion by 210bps from 21.7% in 1Q23 to 23.8%. As a result of the strong EBIT margin, TYL reported non-GAAP EPS of $2.20, beating consensus expectations by $0.10.

Competitive advantages

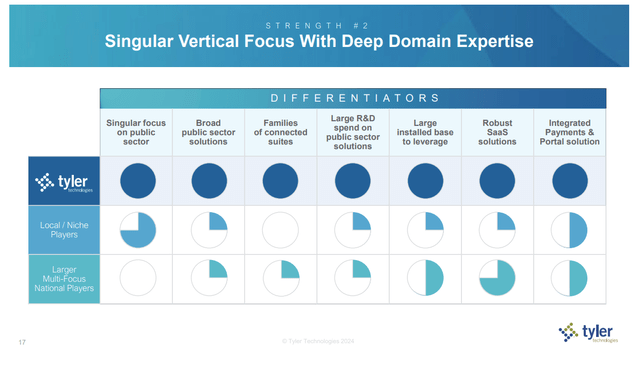

TYL’s competitive moat is its leading position and its deep domain expertise. TYL’s client base predominantly consists of county and municipal agencies, school districts, and other local government offices. These customers are typically more risk-averse and would only adopt solutions from a reputable player (i.e., since other government entities have adopted TYL, it is deemed safe for adoption). As the leading player, TYL benefits from this dynamic. Deep domain expertise also meant that TYL became a one-stop-solution for its customers, which is a big advantage as government entities are typically slow in adopting IT solutions (a lot of hurdles to pass before they can adopt a solution because they are paid by tax payer money), so it is easier for them to have one vendor to settle everything rather than sourcing multiple point solutions that may not integrate well together. Lastly, because of the nature of these solutions, TYL is also very sticky by nature, which makes it hard for its customers to rip and replace easily, as doing so could potentially disrupt the entire operation flow. This is well seen in TYL achieving 98% gross client retention in FY23.

The beauty is that these competitive advantages snowball as TYL scales larger. The bigger TYL becomes, the more reputable it gets, which increases its chance of winning deals and thereby gives it a larger base of recurring revenue. Larger financial capacity also means that TYL can reinvest more aggressively into R&D to further expand its solution offerings, enhancing its position as a one-stop-shop for its clients.

TYL

Large and growing TAM

TYL

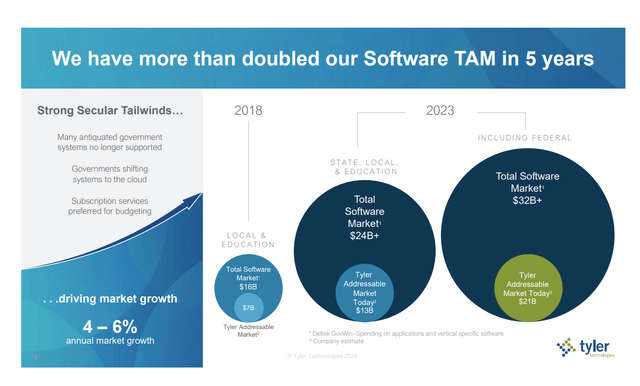

TYL operates in a very large and growing total addressable market [TAM] that should enable it to grow over the long term. As per the latest investor day, the TAM is sized between $37 billion and north of $50 billion (if including the federal government) and is expected to continue growing in the mid-single digits. My opinion is that TYL can continue to capture share here because of the need for public sector entities to transition to new platforms, as many legacy government systems are likely no longer supported by vendors. Importantly, these legacy solutions are just not capable of delivering the required performance in the current digitalized world. For instance, digital analytics is getting more important, and this can only be efficiently done if data is integrated into the cloud.

TYL

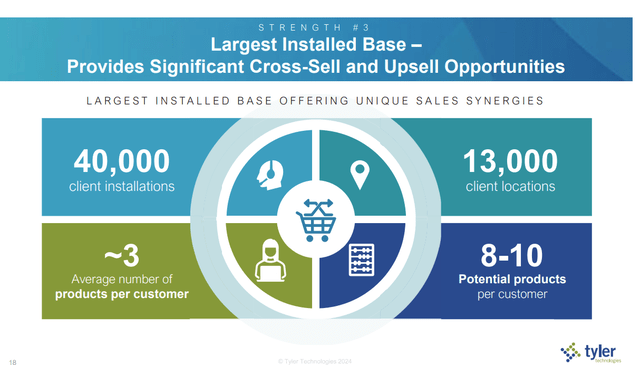

What would help TYL further grow above market level is through its very successful cross-selling efforts. Currently, TYL’s clients adopt around 3 products per customer, and management noted the potential for 8 to 10 products. Just doing the math on this implies a potential for TYL to more than double its revenue base (assuming the same pricing per product). In this regard, 1Q24 results gave a very encouraging update, as TYL witnessed solid execution in the sales organization following adjustments to focus on more cross-selling throughout the company, especially in its efforts to attach more solutions when customers switch to the cloud. Two notable cross-sell deals cited during the call was an Enterprise ERP win with the Texas Legislative Council, an existing client of TYL, and a Records Management and ERP Pro win in Ada County, ID, which involved payments and made use of Tyler’s current state enterprise agreement.

Cloud transition well underway

TYL

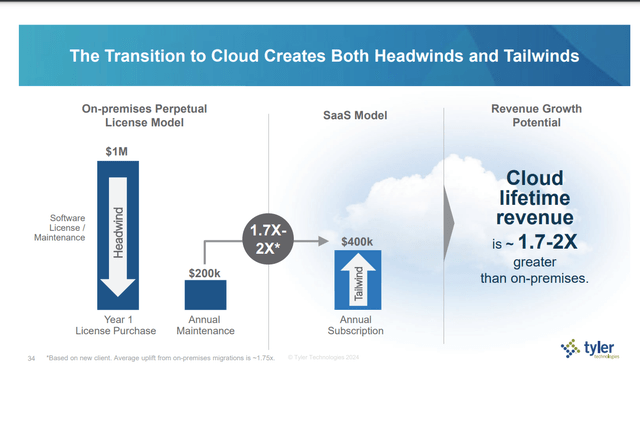

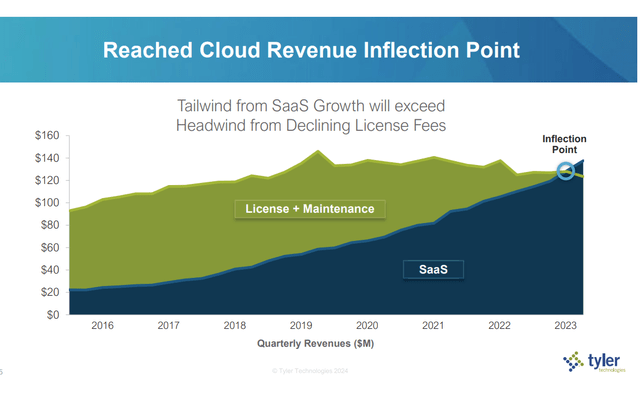

In the past, TYL sold on-premise solutions, but in late 2019, the business started its transition into a cloud model. The financial impact is huge because the customer lifetime value [CLTV] of a new cloud customer was estimated to be 1.7x to 2x the value of an on-premise customer. Execution on this transition has been nothing but spectacular, as seen from the steady increase in the percentage of new software clients choosing the cloud model in recent years, as evident in the total SaaS revenue data, which on a quarterly basis has crossed legacy on-premise revenue stream.

TYL

The momentum has been strong even in the most recent quarter (1Q24), when TYL increased the number of customers converted from on-premise to SaaS to 90 (up from 73 in 1Q23) and bookings from SaaS conversions were up 50% compared to 1Q23. Bookings from new SaaS deals were up 6% in the quarter after falling by 22% in 2023, which is encouraging. Average SaaS annual recurring revenue also increased sharply by 22%, indicating that TYL is successfully converting larger customers. Since management has already stated their intention to convert over 20,000 existing customers over the next 8-10 years, I expect that conversion runway will remain strong.

Valuation

Redfox Capital Ideas

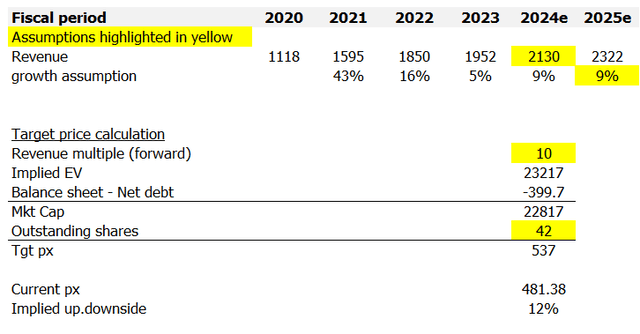

I model TYL using a forward revenue approach, and using my assumptions, I believe TYL is worth $537. I believe there is a high likelihood that TYL can achieve management guidance of 9% growth in FY24 and a similar growth strength in FY25 given the industry growth (supported by strong secular tailwinds) and the ongoing cloud adoption momentum. At this rate of expected growth, I believe TYL should trade at 10x forward revenue when compared to similar peers like Thomson Reuters, which has a similar expected growth rate of high single-digits.

Risk

Although the secular tailwind is strong, entities in the public sector might take longer than expected to switch to the cloud, and this would impact TYL’s growth rate. Furthermore, any increase in interest rate may also reduce the rate of implementation as entities allocate their resources to more pressing matters (i.e., the legacy solutions can still work in the near term, so it is not an urgent matter to upgrade them).

Conclusion

My view for TYL is a buy rating due to its dominant position in a large and growing market. With the ongoing cloud transition and successful cross-selling efforts, I believe TYL is well positioned for long-term growth. While there are risks associated with the speed of public sector cloud adoption and rising interest rates, the execution and results so far have been positive.

Credit: Source link

{kind=link}