Stanislaw Pytel

Twist Bioscience’s (NASDAQ:TWST) second quarter results were strong on the back of NGS demand, and based on guidance, this strength is likely to continue. While Twist’s losses remain large, the company still has a sizeable cash balance, and cash burn should moderate in coming quarters.

I previously suggested that near-term upside was likely limited but that Twist had significant potential longer term due to multiple growth drivers (NGS, Express Genes, Biopharma, Data Storage).

Market Conditions

While Twist’s performance has been somewhat disappointing in recent years, this must be viewed in light of the tough operating environment. Market conditions remain tough for biotech companies, particularly with higher inflation readings in early 2024 contributing to expectations of higher for longer interest rates. The cost of capital is a significant concern at the moment, with rising rates generally leading to lower stock prices. Many companies offering tools and services to biotech customers have seen growth evaporate over the past two years, and in comparison, Twist continues to perform quite well.

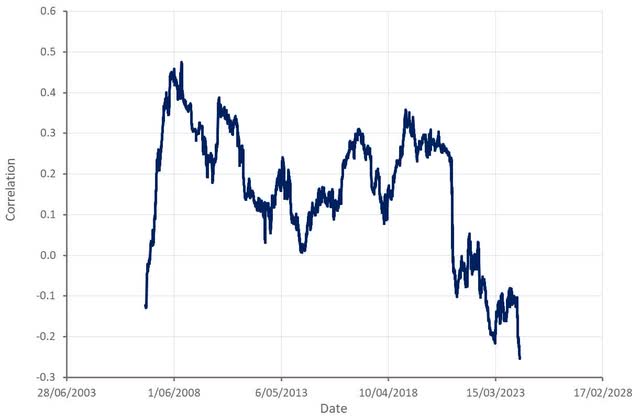

Figure 1: XBI and Treasury Yield Correlation (source: Created by author using data from Yahoo Finance)

Twist Business Updates

Twist’s Express Gene service had a broader launch in January. In excess of 700 accounts have ordered Express Genes, including 100 net new accounts, and approximately 15% of Q2 clonal genes revenue came from Express Genes. Express Genes are a premium priced product, with pricing based on available production capacity. Express Genes utilize the same production process, meaning that premium pricing is expected to fall through to profits.

NGS drove strength in the second quarter, with NGS revenue increasing 40% YoY to $40.8 million. Twist believes that it is gaining market share in NGS. Twist’s customers are advancing clinical studies and commercializing their services, which is supporting growth. Liquid biopsy demand in particular will provide a multi-decade tailwind. Twist wants to capture 10% of the COGS of its customers, which could mean in excess of $500 million revenue within the next decade.

Twist’s NGS product portfolio has traditionally been focused on target enrichment of DNA, RNA and mutations. The company is now trying to offer customers a complete workflow solution, which should support revenue growth and competitive positioning.

Twist recently added a cell free DNA library that helps to capture molecules that may have otherwise been missed. This can help to improve the signal-to-noise ratio of liquid biopsies. Initial commercial performance has reportedly been encouraging.

Twist also recently announced early access to the Twist Flex Prep Ultra High-Throughput Kit. This is designed to accelerate the conversion of microarray to NGS by enabling increased throughout and lower costs. Twist believes that the AgBio opportunity could be worth $500 million.

Twist’s Biopharma segment generated $4.7 million in revenue in the second quarter, with $5.8 million of orders. This was a fairly soft result, exacerbated by the fact that Twist reduced its full-year Biopharma guidance. Somewhat surprisingly, Twist has suggested that there are no market headwinds. While Twist now has a full team, newer personnel are still ramping. Twist will need to start reporting improved results in coming quarters, or the viability of this business will come into question. On the plus side, at least one partner is expected to initiate human studies with an antibody discovered by Twist’s platform in the next year.

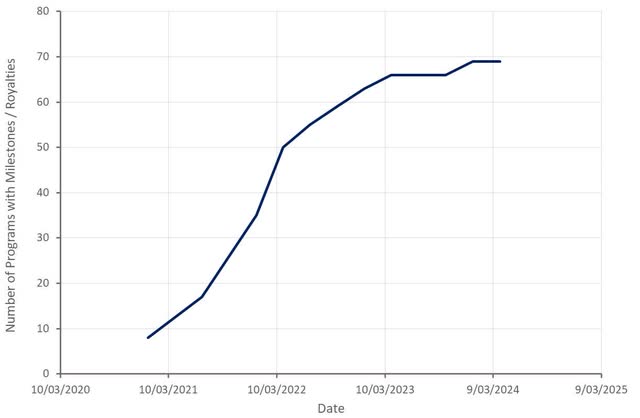

Figure 2: Twist Biopharma Programs with Milestones/ Royalties (source: Created by author using data from Twist)

Financial Analysis

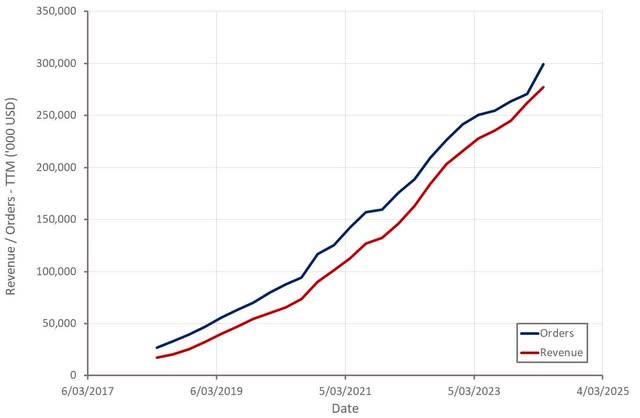

Twist generated $75.3 million revenue in the second quarter, a 25% increase YoY, driven primarily by the NGS business. Orders increased 45% YoY to $93.2 million, although much of this strength was due to a large blanket purchase order that is expected to be used over the next three quarters.

Twist shipped 193,000 genes in Q2, a 27% increase YoY. The company also shipped product to 2,253 customers in the second quarter, up 7% YoY.

Synthetic genes revenue was approximately $22.4 million, up 24% YoY. Approximately $15.6 million of this was from clonal genes, with $2.2 million from Express Genes. Twist served 558 NGS customers in Q2, with the company’s top 10 customers accounting for approximately 36% of NGS revenue.

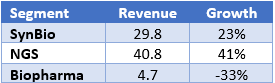

Table 1: Twist Revenue by Segment (source: Created by author using data from Twist)

In Q3 FY2024, Twist expects:

- Total revenue – $77 million

- SynBio revenue – $31 million

- NGS revenue – $41 million

- Biopharma revenue – $5 million

For the full financial year, Twist now expects $300-$304 million, an increase of 20-24% YoY.

Figure 3: Twist Revenue (source: Created by author using data from Twist)

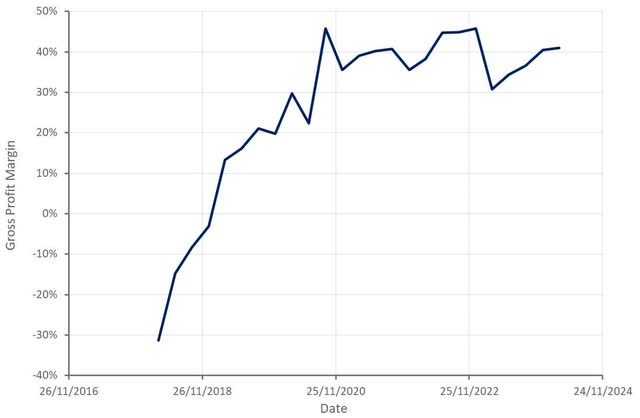

Twist’s gross profit margin increased to approximately 41% in the second quarter. Express Genes growth supported gross profit margins, but this was offset by a large, discounted order from a SynBio customer. Twist’s NGS business also continues to have solid margins.

While Twist’s gross profit margins continue to improve, I consider the result disappointing given the scale up of the Wilsonville facility and the launch of Express Genes. More time is needed to ascertain the ultimate impact of these initiatives, though.

Increased revenue will be a primary driver of improved margins going forward. Twist is also focused on margin improvement initiatives like:

- Product investments

- Insourcing

- Process optimization

- Contract negotiation

Twist expects a 41-42% gross profit margin in Q3 and 43-44% gross profit margins in Q4. The company is targeting a gross profit margin in excess of 50% by the end of FY2025.

Figure 4: Twist Gross Profit Margin (source: Created by author using data from Twist)

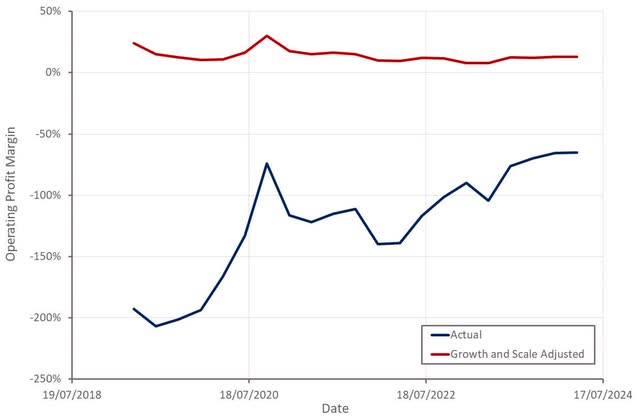

Twist’s operating losses and cash burn continue to narrow, although they are still relatively large. I estimate that the company is on track for operating profit margins around 15% as it matures. Biotech and data storage could provide upside, though.

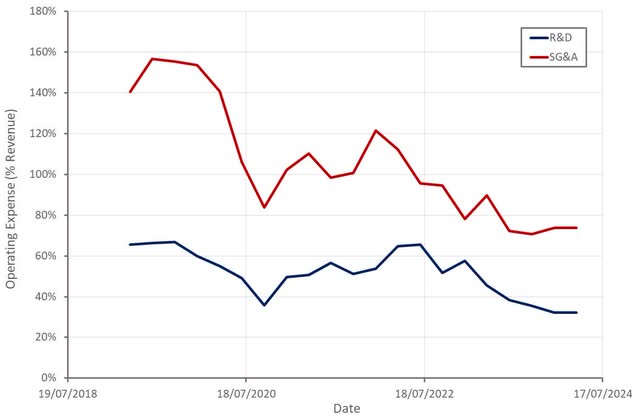

Twist’s R&D declined 12% YoY to $24.1 million, driven by reduced headcount and lab supplies. SG&A was $55.6 million up modestly YoY on the back of SBC and bonus accrual catch up. Operating expenses included approximately $7 million for data storage.

Twist’s cash flow used in operating activities was $42.4 million in the first half of FY2024 and continues to moderate. Twist plans on investing approximately $15 million in CapEx in FY2024.

Figure 5: Twist Operating Profit Margin (source: Created by author using data from Twist)

Figure 6: Twist Operating Expenses (source: Created by author using data from Twist)

Conclusion

Twist’s financial performance looks strong given the difficult macro environment. Liquid biopsy demand appears to be supporting growth, which should continue as adoption in screening begins to ramp. SynBio growth should also pick up when the cost of capital moderates.

It is not all positive, though. Twist’s Biopharma business is still struggling, and little has been said about data storage recently. Investors will also likely remain focused on Twist’s losses while interest rates are elevated. Twist expects to end FY2024 with more than $245 million, though, which should be sufficient for the company to reach breakeven over the next few years.

While Twist’s valuation probably limits near-term upside, the company is still attractively priced for long-term investors. Twist should generate strong growth over a multi-year period and will transition to profitability in coming years. The company’s Biopharma and Data Storage businesses also both have the potential to become valuable in their own right, but are still nascent.

Figure 7: Twist Price / Sales Ratio (source: Seeking Alpha)

Credit: Source link

{kind=link}