MF3d

Standard Lithium Ltd. (NYSE:SLI) announced some rather large news recently. In this article, we are going to explore the partnership with Equinor (EQNR) and what it means for SLI from a big picture viewpoint.

Note: If you want a detailed explanation of the Standard Lithium projects, please read our coverage from last month. That explains in great detail all project costs and should be considered “required reading” for those not familiar with Standard Lithium.

Acceleration of The Lanxess Project

In today’s news, SLI landed a partnership with Equinor. At first glance, I can’t say I was overly excited. My initial reaction was more similar to “We are selling off some percent of ownership in two of the three projects and not for chump change but also not an earth-shattering amount. Kind of surprising, given how incredible the lithium grades are in Texas.”

The market seemed to concur; the stock was slightly down. Then I pondered it a few minutes and thought: “What does this bring to the table for SLI? Would I carry out the same actions that they did?” The answer is yes, I would.

You see, Standard has a limited amount of capital, and they need to move forward. Thus, the partnership makes sense. The amount of capital required to fully explore Texas and the South-West Arkansas project is slated to require tens of millions of dollars, along with an unknown tincture of time. The cost to actually develop the projects could be in the low billions. This partnership provides the capital needed to push the projects forward at an accelerated pace, but more importantly, it accelerates the Lanxess1A project.

Mining Overview

Before we get into why this all matters from a strategic corporate viewpoint, we must understand the mining process from discovery to pulling pay dirt out of the ground (or in Standard’s case, pay dirt from the brine). Typically, in the life of a mining project, you see various phases:

- Prospecting and Exploration

- Development

- Extraction

- Closure.

The process of getting to extraction can take hundreds of millions to billions of dollars in capital and over a decade in time (if not more) for a lithium clay or brine lithium project. It can be a very long and very painful process. Not everyone is cut out for mining stocks, much less penny mining stocks. However, some are, and while the risk is obscene, the rewards can be equally obscene and unnatural. Getting from finding good mineral assets to extracting said mineral assets can be challenging. Not only does one have to deal with local, state, and federal government permits, you also have to attract capital. Many companies, quite frankly, need a large partner with deep pockets to bring a project online.

The Standard Lithium Big Picture

Sometimes you just have to do what you have to do. It is unrealistic to think that the least developed projects (Texas and SWA) will arrive first before the most developed project (Lanxess 1A).

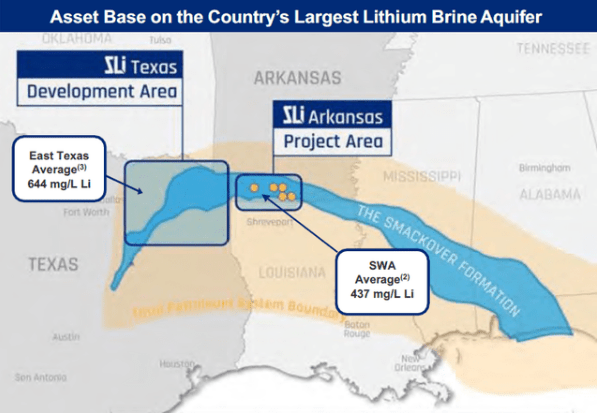

SLI Project Locations (SLI)

It is also unrealistic to think that the company can push all 3 projects forward alone and in any respectable timeline. So what does the partnership bring to the table?

1. No dilution to existing shareholders. This deal is not for stock, but rather Equinor is buying 45% of the Texas and SWA projects. (Standard owns the remaining 55%)

2. A payment to Standard of $30 million.

3. A work program to further develop the Texas project for $20 million and SWA for $40 million: a total of $60 million in development funding. After which point, costs are divided among the two parties as a percent of ownership (SLI 55%, Equinor 45%).

4. Up to $70 million in payments to SLI (subject to both parties taking positive Final Investment Decisions).

And something that is critical:

5. While Standard sold 45% of the projects, they also now have a partner that is going to incur 45% of all future costs. That is massive and will provide potentially hundreds of millions in funding.

First Exxon Entered Arkansas, Now Equinor Joins The Fray

Exxon Mobil (XOM) moved in next door to Standard Lithium for $100 million, which was intriguing. Now you have Equinor, an energy company (with a market cap almost $82 billion) taking a percent of ownership in SLI. Will they have the deep pockets needed to be a valuable partner? Can they actually pony up the potential hundreds of millions? The answer is yes, they can. Per an SA article, we can see that even with depressed natural gas prices, they have managed to pull in adjusted earnings of $7.53 billion:

Q1 adjusted earnings – the company’s preferred measure – fell to $7.53B from $11.92B in the year-ago quarter but still topped the $7.2B in a company-compiled analyst consensus, while revenues fell 14% Y/Y to $25.1B.” – Source: Carl Surran.

Government Funding of Standard Lithium

It is my limited understanding that one thing the government wants to see is a project partner with deep pockets before they fund projects. Lithium Americas (LAC) jumped into bed with General Motors (GM) and the government pushed $2.26 billion at LAC. It stands to reason that Equinor more than meets these requirements for the Texas and SWA projects, given how large the company is. Granted, they are going to have to spend time and capital to develop these projects, but if we go forward in time, we should see some action on them via government funding.

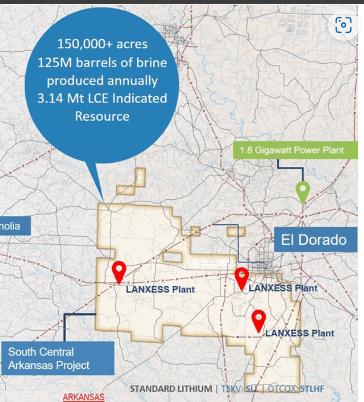

Accelerating The Lanxess 1A project

The Lanxess 1A project is the most advanced of the 3 projects in Arkansas. This project has 3 areas noted by red pins below.

The Lanxess / SLI project (Standard Lithium)

Observing the financials of the deal: Upon closing, SLI receives $30 million and potentially an additional $70 million if conditions are met. Government loans can cover roughly 65% to 75% of a project’s cost. Looking at the DFS for phase 1 of the Lanxess 1A project, we note a smaller initial project of 5,400 tonnes at a capex of $365 million. Mix in inflation and we should be at $400+ million. Thus, SLI could obtain roughly 25% of the required capital to fund the Lanxess project in this deal. Adding government loans, we might have the majority of capital needed. Then again, with inflation rather active, there might be a small amount we need to cover. Digressions aside, this potential $100 million accelerates the project and could allow SLI to get this phase going faster, gain a partner, as well as a DOE loan for this portion.

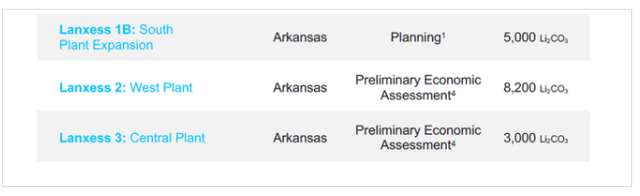

If they gain a partner that for the Lanxess project, that could result in favorable news. Remember, the Lanxess project has 3 phases. Thus, we could get to the other 2 phases of the Lanxess project faster once phase 1 is going.

The 3 phase Lanxess 1A Project (Standard Lithium)

Risks

Standard Lithium is a penny stock with limited (but potentially expanding capital due to this deal). The lithium market is fickle and can quickly go from despondency to exuberance in months (and reverse just as quickly). Frankly, it is a roll coaster. Mining stocks require great patience and also require that you study a project and a market. If you are unable to devote the time, it might be best to hire an investment advisor or altogether avoid the sector. As a side note:

- Cash and cash equivalents and working capital of Ca$15.7 million and Ca$7.7 million, respectively, as of March 31, 2024.

We will soon be able to add $30 million USD to that figure above.

Lithium Outlook By Albemarle

Albemarle (ALB) offered up some future crystal ball predictions concerning lithium. Per the May 02, 2024, earnings call transcript:

We continue to believe in the EV transition and the growth in lithium demand, as well as the opportunity it creates for Albemarle. Despite a downshift in demand growth in Europe and the United States, global EV sales were up 20% year-to-date, led by strong growth in China, which represents over 60% of the global EV market.

We continue to anticipate 2.5x lithium demand growth from 2024 to 2030. Additionally, we see battery size growing over time, driven by technology developments and EV adoption. These factors all translate to significantly higher global lithium needs. To put all this in perspective, we expect that this industry needs more than 300,000 metric tons of new lithium capacity every year to satisfy this growth. This means, we need more than 100 new lithium projects across resources and conversion between now and 2030 to support this demand.

More than 300,000 metric tons of new lithium capacity EVERY year to satisfy growth? That is quite a powerful prediction.

Conclusion

Today’s deal should be considered an evolution of the two SLI projects. The projects receive development money and now have a deep pocket partner who will fund 45% of Capex. Meanwhile, Standard’s most advanced project receives a massive capital infusion, which could accelerate it to obtaining a partner as well. This evolution is a necessary stepping stone in the right direction for all three projects.

Credit: Source link

{kind=link}