")

SomeMeans

The financials sector has faced significant tumult in recent months as last year’s record bond market crash impairs the fair equity value of many financial institutions. Virtually all stocks in the financials sector have seen material declines since March as investors begin to understand the depth of this issue better. Of course, not all financial companies have been impacted to the same extent, with those not allocated toward bonds facing much lower drawdowns. However, other subsectors, such as insurance, have taken a more significant hit due to immense realized losses on devalued bonds.

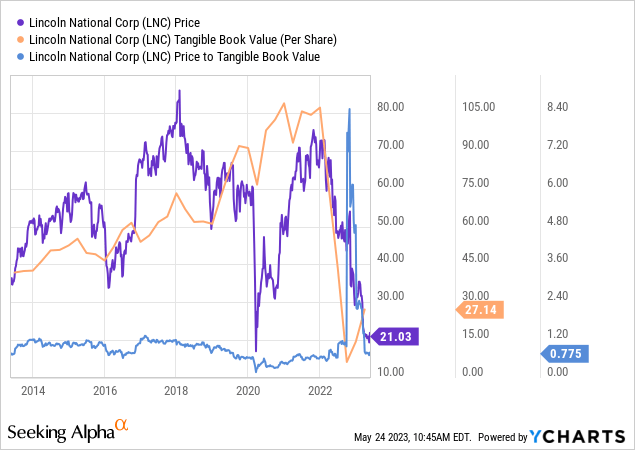

Unlike banks, most insurance companies cannot place securities in the “held to maturity” category, where they do not need to realize bond devaluations. Most insurance company assets are “available for sale” because insurance providers are expected to sell many of their holdings as benefits. One interesting example is Lincoln National Corporation (NYSE:LNC), which has seen a ~$10B asset devaluation due to declines in the value of its fixed securities assets. Most of those securities are corporate bonds ($80.5B today), with most due after ten years – giving them exceptionally high duration price risk exposures. Over time, LNC’s cash flow will be impacted by these losses as it is generally likely to sell those assets at a loss unless long-term Treasury yields fall back to extreme lows over the coming years. As shown below, this loss has had a substantial negative impact on the company’s valuation:

LNC’s price-to-book ratio is back in its normal range, closer to the low end associated with further expected losses. Many analysts are bullish on the stock due to its high 8% yield and extremely low 3X forward “P/E” ratio. While its valuation is undoubtedly low, I believe many bulls may fail to realize the likely ~$10B cash-flow hit the company will eventually take due to its bond portfolio’s colossal devaluation. Accordingly, with a solid bullish and bearish case facing LNC stock, I believe it is an opportune time to take a closer look at the company’s fundamentals in the economic landscape context to determine its potential better.

LNC’s Huge Bond Market Risk Exposure

Lincoln National operates through multiple insurance brands focused on life insurance, annuities, group protection, retirement, etc. Like all insurance companies, it collects premiums and invests that cash into various assets, primarily fixed-income securities (~$100B) and mortgages ($~18B), as well as its larger portfolio for separate account assets associated with its annuity program.

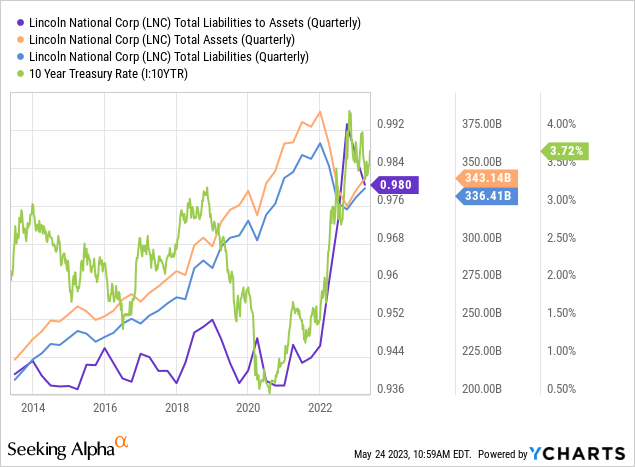

Of its assets, the greatest “risk” is in the category generally perceived as “low risk,” fixed-income bond securities in investment-grade corporations. As discussed in earlier articles, “lower credit risk” securities can be higher risk in rising interest rate environments because low-yielding assets naturally have higher duration risk (price declines as interest rates rise). For example, the “low-risk” IG corporate bond ETF (LQD) fell ~23% from its peak in 2021, while the “junk bond” ETF (JNK) only fell by ~16% over the same period. The same ~2.5% yield increase has a more considerable impact on lower-yielding assets, such as those owned by Lincoln. Thus, LNC’s book value and leverage level are closely tied to the interest rate paid on longer-term Treasury bonds. See below:

Since 2020, LNC’s correlation to the 10-year Treasury bond rate has become much larger as the company’s exposure to fixed-income securities has risen, as has the volatility in those securities. While bond yields may reverse lower and improve its portfolio, it is also possible that they rise even higher, potentially pushing LNC’s book value to zero, exacerbated by its highly leveraged equity position today. Today’s extreme yield curve inversion and the sharp ~35bps increase in 10-year Treasury bond yields this month indicates this may be likely. Long-term Treasury yields remain well below the current inflation rate, suggesting investors may eventually seek higher returns on these assets should inflation remain around 5%.

In my view, there is a greater probability that fixed-income securities will devalue further than reverse higher, mainly due to inflation and related issues in the oil and labor markets. While LNC is likely trading at slightly below its book value today (based on current assets’ fair values), it would only take a ~2% decline in its asset portfolio value for LNC’s book value to fall to zero. However, most LNCs’ total assets carry less direct exposure to interest rates. At the end of last quarter, ~$50B of its assets (by fair value) wherein fixed-income securities with a > 10-year maturity, and $16.5B were in those with a 5-10 year maturity. Most of these assets are of an “investment grade” or “IG” credit rating, meaning their “spread” to Treasuries is relatively low. “IG” corporate bond credit spreads can rise to 2-3% above Treasuries in the case of a recession, a minor risk factor that could become important.

Assuming the total ~$66.5B of LNC’s “at risk” fixed-income securities assets carry an estimated ~12-year maturity (given $16.5B is in the 5-10 bracket and $50B is over 10) and a had a weighted-average yield of 4.03% at the end of March (as stated in its 10-Q pg. 120), the “duration” of these assets is likely around 9.5. This calculation implies that a 1% rise in longer-term Treasury yields would cause a ~$6.3B decline, or a 9.5% decline, in the fair value of LNC’s fixed-income securities assets with maturities over five years.

Since the end of March (its last reporting date), there has been a 29 bps increase in the 10-year Treasury rate. Assuming no change in corporate bond spreads since then, this slight rate increase has likely had a ~2.76% (or 0.29 X 9.5%) impact on the value of this $66.5B securities asset section, lowering their fair value by an estimated ~$1.83B. If so, given no change in the value of any other of LNC’s assets, the company’s tangible book value today is estimated to be closer to $2.77B (or $4.6B – $1.83B). Given its $3.7B market capitalization, LNC is likely trading for around 30% more than its actual book value today. Further, based on this bond match, a 4.1% decline to its $66.5B in “high duration risk fixed income assets” may cause LNC’s book value to reach zero, associated with a ~44bps increase to longer-term US Treasury rates. Given we’ve seen a 30bps increase in long-term rates in May alone, I do not believe that is an unlikely possibility.

In reality, LNC is unlikely to suffer immediate financial strain due to unrealized losses on its bond portfolio. This potential loss falls into the “AOCI” category, which, if excluded, LNC’s book value would be closer to $64. However, LNC is not a bank generally expected to see its securities held to maturity, given no deposit declines. Insurance companies usually payout over 95% of premiums as benefits, so as benefit payments grow, LNC will eventually realize these losses should long-term interest rates fail to decline quickly.

Excess Mortality Risk Compounds Issue

Where banks face falling deposits that force sales of devalued bonds, life insurance companies face increased customer mortality. From 2020 through 2022, there was no significant change in Lincoln’s life insurance segment’s operating revenue, fluctuating from $7.1B in 2022, $8.1B in 2021, and $$7.5B in 2020. However, its benefits payments surged from $4.2B in 2021 to $7B in 2022, resulting in a staggering operating loss on life insurance of ~$2.5B (see 10-K pg. 54). Most of those payments are associated with mortality from 2020-2021 that was paid-out in 2022; as the company stated that mortality claims declined in 2022. That said, as mentioned in its last earnings call, mortality claims remain above pre-COVID levels

Despite a >95% decline in COVID national deaths, US mortality levels were generally 20-30% above the projected level at the end of 2022. Some recent data suggests the “gap” closed in 2023, which may be due to significant reporting delays. Other studies indicate the excess mortality gap is still rising, with the most notable increase among younger people who typically carry very low life insurance risk. Potential factors include the sharp rise in heart-related events, cancer, strokes, and self-inflicted death (which does not directly impact LNC).

At any rate, life insurance companies are racing to understand this issue better as it is impacting their bottom line. Should benefits continue to be much higher than insurance premiums, Lincoln must sell more securities at a considerable loss. Instead of fixing its operational profitability, Lincoln is seemingly much more focused on continued business expansion which does not necessarily benefit shareholders since its assets and liabilities will grow proportionately. In my view, the company continues to assume that its risk levels will return to “pre-COVID” levels when the data seem to suggest that the “new normal” is a slightly permanently higher mortality (and benefits expense) world.

Finally, the company’s annuities business may face higher risks today due to the recent declines in stocks and bond prices. The US demographic pyramid is significantly skewed toward the 55+ age group, with more Americans expected to retire over the next five years than ever before. This is a significant risk factor for LNC because bond and stock values have declined over the past year and could fall further as its payments grow. Lincoln’s retirement business has been its one hold-out of strength since 2020, mainly because many older Americans are racing to save for retirement. Demographic trends suggest this pattern will reverse over the coming years as retirement savings become retirement spending, potentially as asset prices are lower – leaving more significant losses for LNC, which bears some burden to considerable market risk.

The Bottom Line

Overall, I believe LNC is a risky stock today, and I am slightly bearish on the company; however, due to its low forward “P/E” ratio of ~3X, I do not believe it is a short opportunity. In reality, I doubt that the company will achieve the EPS level expected by most analysts today, mainly due to a potentially more significant rise in Treasury rates and evidence suggesting a sustained excess mortality level. If mortality levels normalize, Treasury yields remain where they are or lower, and equity and real estate markets remain healthy. LNC’s outlook would be relatively stable, with decent “deep value” potential.

However, I believe excess mortality is more likely to remain an issue than widely assumed. Based on my views regarding commodities, I also think long-term Treasury rates may rise further, most likely causing the company’s tangible book value to fall below zero. Lastly, should equity markets crash on recession risk, then the company’s annuities business may face significant headwinds that could coincide with an increase in retirement payouts due to demographic trends (particularly if equities fail to recover 2-5 years out, as is often the case in cyclic recessions).

Since LNC is essentially operating at ~50X leverage today (from assets to book value), there is no reasonable way to provide a long-term price target for the stock since a slight change in its asset value could dramatically alter its book value. Further, my outlook for LNC is based on speculative possibilities, which I believe are more likely than most analysts and investors currently assume. All of these issues could entirely impair LNC’s equity value if prolonged. Because these are more speculative risk considerations, I would not bet against LNC today. However, bullish investors should not underestimate the risk regarding LNC, and I believe most LNC analysts fail to appropriately cover the significant risks facing (and harming) the stock today.

Credit: Source link

")

{kind=link}