")

PM Images/DigitalVision via Getty Images

The First Trust Municipal High Income ETF (FMHI) is an actively managed exchange-traded fund that seeks to provide its investors with a very high level of current income that is exempt from Federal income taxes. This might be appealing to investors who are in a high federal income tax bracket, especially considering that the fund has historically had a tax-equivalent yield that is comparable to that of a junk bond ETF such as the State Street SPDR Bloomberg High Yield Bond ETF (JNK). However, this fund’s portfolio does not consist of junk bonds, but is instead comprised primarily of a mixture of investment-grade and unrated municipal bonds. As such, the securities contained within this fund should have a lower default risk than the bonds that are held in the portfolio of a junk bond fund. These characteristics could make the First Trust Municipal High Income ETF an interesting fund for anyone who is in a high-income tax bracket and wants to hold an income-focused investment in an ordinary taxable account.

About The First Trust Municipal High Income ETF And Municipal Bonds

The First Trust Municipal High Income ETF is an actively managed exchange-traded fund sponsored by First Trust that aims to provide its investors with a high level of current income by investing in a portfolio of municipal bonds. The fund’s website offers the following description of the fund’s strategy:

The First Trust Municipal High Income ETF is an actively managed exchange-traded fund. The Fund’s primary investment objective will be to seek federally tax-exempt income, and its secondary objective will be long term capital appreciation. Under normal market conditions, the Fund seeks to achieve its investment objectives by investing at least 80% of its net assets (including investment borrowings) in municipal debt securities that pay interest that is exempt from regular federal income taxes.

As this description makes clear, the First Trust Municipal High Income ETF invests the bulk of its assets in debt securities issued by local and state governments. This is a popular asset class among some investors due to the fact that the coupon payments that these bonds make to their investors are exempt from federal income taxes. In a sense, the tax rate that an investor has to pay on the income that they receive from most municipal bonds is 0%. This is obviously a much lower tax rate than the income that they receive from corporate bonds and U.S. Treasury bonds, which is taxed at ordinary income rates. For an investor with a high income, that is potentially as high as 37%, with state taxes on top of that. In addition to this, municipal bonds are also frequently exempted from state income taxes as long as the issuer is a municipality in the same state. This second tax exemption is the reason why we frequently see funds that focus on municipal bonds in a single state. For example, the following ETFs invest only in municipal bonds issued by entities in a single state:

The purpose of these funds is to invest only in bonds that provide income to investors in those particular states that is free of any income tax at all. High-income investors in California and New York have among the highest marginal income tax rates in the country when both federal and state taxes are combined, and, of course, taxes reduce the total returns that investors earn from their portfolios. As such, investors in those states who have already maxed out their contribution limits for their IRAs and still have money left over to invest have an interest in holding tax-exempt assets in their taxable accounts. A single-state exchange-traded fund can work pretty well for investors in this situation, as they provide these investors with a source of tax-free income. However, the coupon income provided by California, New York, or Minnesota municipal bonds might still be taxable on a state level for investors who are based in a different state. As such, these funds are not as attractive to individuals who do not live in those states.

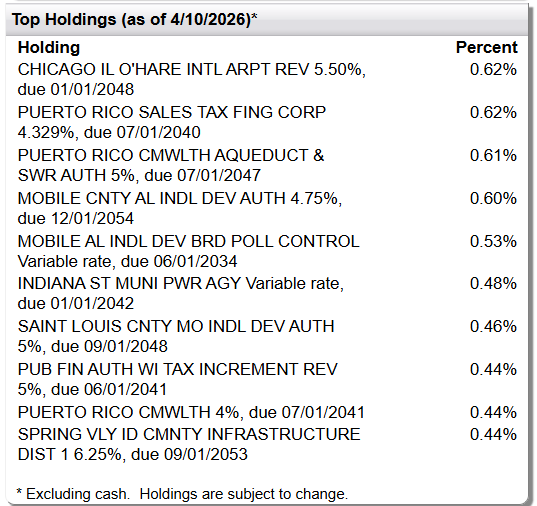

The First Trust Municipal High Income ETF is not a single-state municipal bond fund. It does not put any real effort into minimizing state-level income taxes for its investors. Rather, it attempts to earn as high an income as possible from a portfolio of municipal bonds regardless of where their issuer is located. As of April 10, 2026, FMHI held positions in bonds backed by Chicago’s O’Hare International Airport, the government of Puerto Rico, Mobile County, Alabama, the Indian Municipal Power Agency, and other municipal issuers located in other states:

First Trust

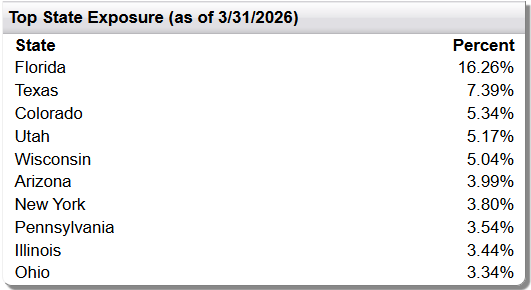

Furthermore, the fund’s assets were fairly well diversified by state as of March 31, 2026:

First Trust

With the exception of Florida, no individual state accounted for more than 10% of the fund’s assets on March 31, 2026. As was already mentioned, the coupon payments made by municipal bonds are typically exempt from federal income tax (although there are a few exceptions, such as Build America Bonds), but they might still be subject to income taxes on a state level. As is the case with all regulated investment companies, investors in the First Trust Municipal High Income ETF pay the same tax rate on the fund’s distributions as they would if they held the fund’s assets directly in their own individual portfolios. The First Trust Municipal High Income ETF receives the coupon payments from the bonds in its portfolio and then distributes them to its investors after deducting its own expenses as fees. As such, investors in this fund should pay no federal income taxes on the distributions that they receive, but they might still have to pay state taxes on the income.

In exchange for their tax-exempt status, municipal bonds usually have lower yields than ordinary taxable bonds. FMS Bonds, an underwriter of municipal bonds for municipalities around the country, provides the following yields for AAA, AA, and A-rated municipal bonds as of April 13, 2026:

Here are the yields on U.S. Treasury notes and bonds as of the same date:

As we can immediately see, even the A-rated municipal securities have lower yields than U.S. Treasury securities of the same maturity. This is in spite of the fact that municipal securities do have default risk, whereas U.S. Treasury securities do not have default risk (at least in theory). Corporate bonds, naturally, also have higher yields than municipal bonds or U.S. Treasuries, regardless of their rating. This allows us to conclude that investors should not put municipal bonds or a municipal bond funds such as FMHI into a retirement account. Due to their higher yields, taxable bonds will deliver higher total returns than municipal bonds, and the retirement account protects the holders of these bonds from taxes, so there is no reason to accept a lower yield from municipal bonds when the tax-exempt status is not needed. In addition, an investor who is in a low tax bracket might receive a higher after-tax income by purchasing a taxable corporate bond or U.S. Treasury security than would be the case with municipal bonds. The only investors who would benefit from investing in municipal bonds are those individuals who are in high tax brackets and intend to hold their position in a taxable account.

The First Trust Municipal High Income ETF Versus Peer Funds

The First Trust Municipal High Income ETF has an inception date of November 1, 2017. This makes it one of the youngest municipal bond ETFs in the market. We can see this by looking at the inception dates of some of the other funds in the market that invest in the same asset class:

As we can see, the only two funds shown that have an inception date later than FMHI are the JPMorgan Municipal ETF and the Capital Group Municipal ETF. A fund’s inception date is not necessarily the most important consideration for a fund due to the fact that it does not really influence the fund’s behavior in the markets. However, there is frequently a correlation between a fund’s inception date and its assets under management. This is because assets under management tend to increase over time as investors put more money into the fund over time and its investment returns compound. This is similar to how an individual’s retirement account at age forty will normally be larger than it was at age twenty. We can see this correlation in this chart, which shows the assets under management for each of the funds shown in the peer comparison chart:

As clearly shown, the First Trust Municipal High Income ETF is the smallest fund out of this peer group. The iShares National Municipal Bond ETF and the Vanguard Tax-Exempt Bond ETF are by far the largest of the two funds. The iShares fund is also the oldest, so that may play a role in its size, but the Vanguard fund is younger than several of its smaller peers. As such, the correlation between the age of a fund and its size does not fully hold true. The iShares and the Vanguard funds are both very low-cost index funds, which may contribute to their popularity. As was already mentioned, the First Trust Municipal High Income ETF is an actively managed fund, and as such, its expense ratio is higher than most passive index-tracking funds. There are some investors out there who do not like to pay high fees, so this could explain the relative popularity of the Vanguard fund.

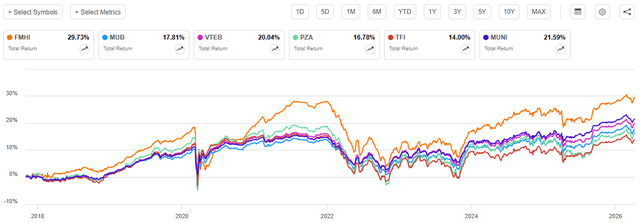

One other reason why a fund’s inception date could be important is that the longer its history, the more time it has had to acquire a performance track record. This may be more important for an actively managed fund than for a passively managed fund due to the fact that an index can generally be backtested. Active management cannot be due to the subjective judgment calls that are involved in passive management. Admittedly, though, past performance is no guarantee of future results, but many investors still like to look at how a fund’s management has performed in the past when attempting to make predictions about how that management will perform in the future. In terms of past performance, the First Trust Municipal High Income ETF has done very well against its peers:

Seeking Alpha

This chart shows the total performance of FMHI against all of the funds in the peer group shown above that have inception dates of November 1, 2017, or earlier. That grouping includes all of the funds except for the JPMorgan Municipal Bond ETF and the Capital Group Municipal Income ETF. As you probably assumed, the starting date for this performance chart is the inception date of FMHI (the terminal date is April 10, 2026). Furthermore, I made the assumption that investors in each of these funds reinvested all of the distributions that each respective fund paid out into additional shares of that fund on the date of payment. While it is certainly true that many income investors might choose to take the distributions and spend them, it is best to assume reinvestment when comparing the performance of different funds, as that is the only way to get a true apples-to-apples comparison. As we can see, the First Trust Municipal High Income ETF outperformed all of its peers by a fairly significant margin with this assumption in place. Over the period from November 1, 2017, through April 10, 2026, FMHI delivered a 29.73% total return. The second-best performance over the period came from the PIMCO Intermediate Municipal Bond Active Exchange-Traded Fund, which delivered a 21.59% total return over the same period. Thus, FMHI outperformed MUNI by 8.14% over the period. It is also worth noting that in this case, the two best-performing funds were both actively managed funds.

The First Trust Municipal High Income ETF pays a monthly distribution, which is fairly common for a bond fund. After all, the Vanguard Total Bond Market Index Fund ETF (BND) and the iShares Core US Aggregate Bond ETF (AGG), which are the two largest exchange-traded bond funds in the United States, both pay monthly distributions, and as such, investors have generally come to expect that. In March 2026, the First Trust Municipal High Income ETF paid a distribution of $0.1750 per share, which works out to $2.10 per share annually. At the fund’s April 10, 2026, closing price of $48.03 per share, this would give the fund a 4.37% yield. Investors should naturally expect the fund’s distribution and share price to vary with interest rates. After all, while its holdings pay coupons that are exempt from federal income tax, they are still bonds, and their price and yield tend to move in response to interest rate changes. Here is how that compares to the peer exchange-traded funds:

(All figures are calculated by annualizing the most recently paid distribution as of April 10, 2026, and then dividing it by the then-current share price of the fund. These yields will vary over time.)

As this chart shows, the First Trust Municipal High Income ETF is one of the highest-yielding municipal bond ETFs on the market. This is likely a big reason for the fund’s historical outperformance versus its peers. After all, the only net investment return that a bond delivers over its lifetime is the coupon payments that it makes to its investors. This makes sense due to the simple fact that an investor first purchases a bond at its face value and receives the face value back whenever the bond matures. As such, while a bond’s price may vary over its lifetime, it does not deliver any net capital gains. Due to this, the higher the yield of a bond, the greater its lifetime return as long as the issuer does not default. This also tends to apply to bond funds and it could be a reason why the First Trust Municipal High Income ETF has outperformed many other municipal bond ETFs since its inception.

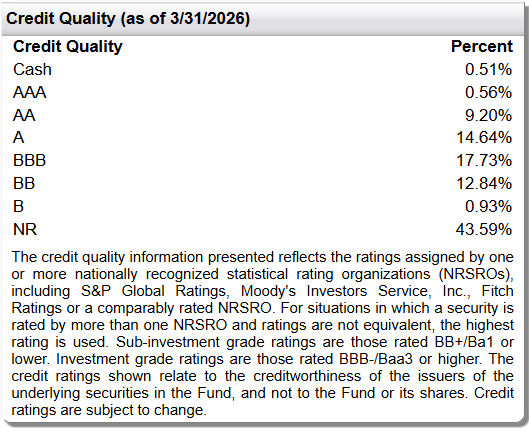

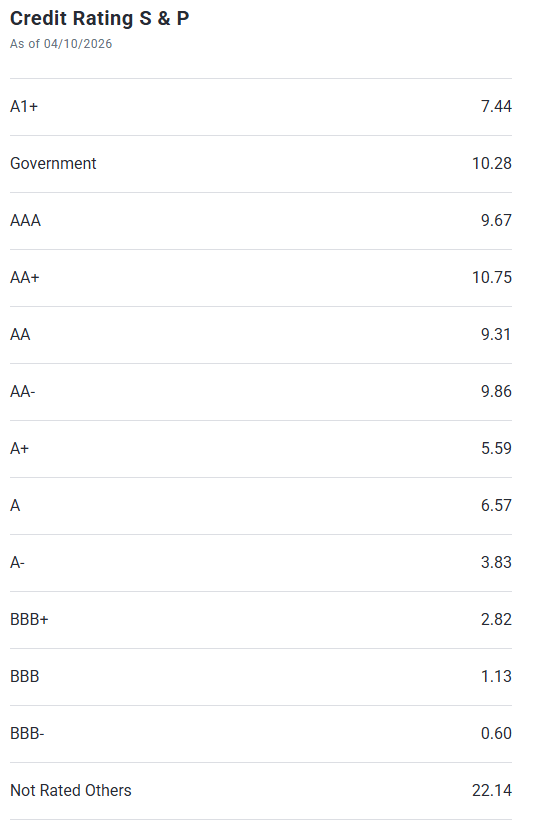

One thing that is worth noting, however, is that the bonds that are included in the portfolio of the First Trust Municipal High Income ETF are lower-rated than what we see in some of the other municipal bond funds shown in the above charts. The fund’s website provides this credit breakdown of the bonds in FMHI’s portfolio as of March 31, 2026:

First Trust

An investment-grade bond is anything that is rated BBB or higher. That only described 42.64% of the bonds in the fund’s portfolio as of March 31, 2026. The remainder of the portfolio is invested in bonds that are either rated speculative-grade (“junk bonds”) or not rated at all.

The website for the PIMCO Intermediate Municipal Bond Active Exchange-Traded Fund provides this breakdown of the bonds in its portfolio as of April 10, 2026:

PIMCO

The PIMCO fund actually had 10.28% of its portfolio invested in U.S. Treasuries and agency securities, which are not federal income tax-exempt. That by itself is very different from FMHI’s portfolio. In addition to that, MUNI is entirely invested in investment-grade bonds, with the exception of the 22.14% of its assets that are invested in unrated securities. As such, we can see that one of the ways that FMHI is achieving a higher yield than its peers is by investing in lower-rated bonds that theoretically have a higher probability of defaulting. This could suggest that FMHI is a riskier fund. However, the First Trust Municipal High Income ETF had 700 different bonds in its portfolio as of April 10, 2026, and as these are municipal bonds, the probability of default is lower than that of similarly rated corporate bonds. As such, FMHI should be relatively safe for most investors as its assets are relatively safe and there is enough diversification within it to ensure that a single default will not have much of an impact on the fund as a whole.

With that said, one area in which the First Trust Municipal High Income ETF may have a greater amount of risk than its peer funds is its duration. Investopedia describes duration thusly:

Duration measures how long it takes in years for an investor to be repaid a bond’s price through its total cash flows. It is also used as a tool to determine the change in a bond’s value in relation to interest rate movements.

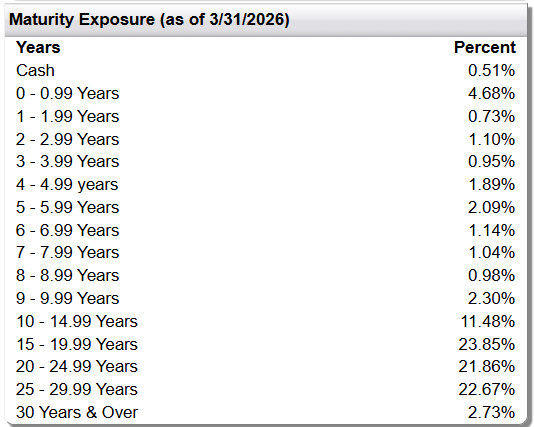

The second sentence in this quote is more important than the first for understanding how FMHI may perform in real-world conditions. In short, what this description is stating is that bonds with a higher duration will exhibit greater price movements whenever interest rates change than will bonds with a lower duration. As duration is measured in years, this means that a bond with a ten-year duration will experience a greater price decline than a bond with a five-year duration if interest rates increase. This is important because the First Trust Municipal High Income ETF has a higher duration than its peer funds. The fund’s website provides the following maturity schedule for all of the bonds held in FMHI’s portfolio as of March 31, 2026:

First Trust

As of March 31, 2026, the First Trust Municipal High Income ETF had a weighted average effective duration of 8.55 years. The PIMCO Intermediate Municipal Bond Active Exchange-Traded Fund had a weighted average effective duration of 5.04 years as of the same date. Thus, we can see that FMHI has a higher effective duration, which means that we can expect its shares to rise more than its peers whenever interest rates are falling, and we can expect FMHI’s shares to decline more than its peers whenever interest rates are rising. We can actually see this if we compare the price performance of FMHI to MUNI over the 2020-2023 period:

Seeking Alpha

This chart shows the share price performance of each of the two funds over the period from January 1, 2020, through December 31, 2023. As you may recall, this was the period of time covering the COVID-19 pandemic and the inflationary surge that occurred afterwards. During the COVID-19 pandemic, primarily in 2020 and 2021, interest rates fell to very close to all-time lows. We can see that, while both FMHI and MUNI rapidly rose in price beginning in early May 2020, the First Trust Municipal High Income ETF delivered greater price appreciation. In late 2021, interest rates started to rise due to the surging inflation that was present in the economy, and interest rates continued to rise through late 2022 (Please note that I am specifically talking about bond interest rates, not the federal funds rate, which rose consistently over the 2022 to mid-2023 period). In late 2022, interest rates fell temporarily, but then rose again following an interest rate hike by the Federal Reserve in July of 2023. We can see that the First Trust Municipal High Income ETF experienced a greater price decline than MUNI did in this period of rising interest rates.

The takeaway here is that while the First Trust Municipal High Income ETF has a higher yield than many other municipal bond funds in the market, it also has greater volatility. Potential investors should consider how much volatility they are willing to tolerate before deciding which fund to purchase.

Tax-Equivalent Yield

As was already mentioned, municipal bonds typically have lower yields than U.S. Treasury securities or corporate bonds with the same credit rating and term. This is due to the fact that investors do not have to pay taxes on the coupon payments that these bonds make to their owners. This can make the yield of a municipal bond fund such as the First Trust Municipal High Income ETF seem very low when compared to the yield of the State Street SPDR Bloomberg High Yield Bond ETF. After all, as was already stated, the annualized yield of FMHI was 4.37% as of April 10, 2026. The yield of JNK was 6.54% as of the same date. This could make it appear as though JNK is providing more spendable income.

However, this is not an apples-to-apples comparison because JNK’s distributions are subject to income taxes and FMHI’s are not. In order to accurately compare the two funds, we need to either calculate JNK’s after-tax yield or FMHI’s tax-equivalent yield. Tax-equivalent yield is the yield that an investor would need to earn from a taxable bond (or taxable bond fund) in order to have the same after-tax income that a municipal bond (or municipal bond fund) provides. The formula for tax-equivalent yield is:

Tax-Equivalent Yield = Municipal Bond Yield / (1 – Tax Rate)

For this formula, the “Tax Rate” should be expressed as a decimal. This is best illustrated with an example. Let us assume that a hypothetical investor is in the highest tax bracket (37%) and wants to know what yield they would need to receive from a taxable bond fund in order to have the same after-tax income that FMHI provides. They would perform the following calculation:

Tax-Equivalent Yield = 4.37/(1-0.37)

This gives a tax-equivalent yield of 6.94%. Thus, the First Trust Municipal High Income ETF would actually provide the investor with a higher after-tax income than the State Street SPDR Bloomberg High Yield Bond ETF.

As might be expected, this fund’s tax-equivalent yield will be lower if an investor’s own tax bracket is lower. Thus, investors in lower tax brackets might actually get better returns out of a taxable junk bond fund. This is also the reason why FMHI is not particularly attractive for anyone who is looking to hold their investment in their retirement account. Such an investor would be sacrificing yield for no benefit.

Expenses

The First Trust Municipal High Income ETF has an expense ratio of 0.49%. This is higher than its peers:

The fact that the First Trust Municipal High Income ETF is an actively managed fund is one reason for this, as active management is more expensive than a passively managed fund due to the need to pay financial professionals to make investment decisions and perform research on behalf of the fund.

Conclusion

In conclusion, the First Trust Municipal High Income ETF is one of the highest-yielding municipal bond funds on the market. This could potentially make it attractive to investors who are in a high federal income tax bracket and wish to have an income investment in an ordinary taxable account. This fund is not particularly attractive for a retirement account, however, as an ordinary taxable bond fund will deliver a higher yield and there is no need to worry about taxes with a retirement account. In addition, investors in low tax brackets will also likely not benefit as much from this fund as they might still get higher after-tax income from a taxable bond fund. This fund is also likely to be a bit more volatile than other municipal bond funds, so your individual risk tolerance should play a role in determining whether it would better suit your needs than its peers.

This article answers these three questions about FMHI:

- Does FMHI provide tax advantages over other bond funds?

- From a risk perspective, how does FMHI compare to other municipal bond funds?

- What type of investor is likely to be attracted to FMHI?

Editor’s note: This article is intended to provide a general overview of the ETF for educational purposes only and, unlike other articles on Seeking Alpha, does not offer an investment opinion about the ETF.

Credit: Source link

{kind=link}