Drone Shot of Summerlin South, Nevada on Clear Day halbergman/E+ via Getty Images

Above: Las Vegas locals market continues to benefit from migration from all over the US, predominantly from California. – US Census Bureau.

- In an otherwise sluggish sector at the moment, Morgan Stanley now sees an upside of 23% to overweight with a $74 PT for Boyd (NYSE:BYD). BYD online revenue gains are the key to the upgrade.

- BYD’s 2020 deal with FLUT for 5% equity traded for access to its 28 properties, 10 state portfolio for Fan Duel is one of the smartest deals in the sector made by brick and mortar operators.

Premise: The most recent upgrade by Morgan Stanley analyst Stephen Grambling validated my own long-standing bullish take on the stock. He moved his call on BYD from equal weight to overweight, indicating a 23% runway ahead within 12 months to $74. According to NASDAQ reports, the analyst liked BYD’s EV/EBITDA ratio vs. peers MGM and CZR. The PT was raised from $59.38 to $74. Given the overall sluggishness of the sector, this change is welcomed by holders.

I agree with this change was well-thought-out given Grambling’s thesis. His bullish take cites many elements of the BYD business I have also long used to build my own case for the stock going back at least four years. He also cited BYD’s ownership of 90% of its own realty as a plus. Most peers have long sold off much of their realty to REITs. But the central catalyst is online growth.

Alpha Spread DCF value at writing $74.50 on target with the Morgan Stanley PT upgrade. Its best case is $~87.

My own long-standing bull thesis on the BYD stock has come out even firmer than Morgan’s. The July 12, 2022, price at our writing was $49.67. We cite similar rationale to support our upside PT. My own follow-up SA take on the stock bears a PT ~$78-$85 (last February 25th) is up to ~$7 above Grambling’s. My higher PT emanates from a more bullish view of brick and mortar revenue gains related to a diminishing competitive impact.

I believe I calculated a bit more bullish is because I have baked in estimates of the business ahead based on trading trends in the sector. But I have also drawn from my inside the business years. I have been encountering similar headwinds and competitive pressures as has BYD, including its most recent 2Q24 results.

google

Above: (Source: Sam’s Town archive). It all started with one guy (Sam Boyd), one property and customer focus that was vital in the locals market.

In brief: 2Q24 BYD Earnings highlights 2Q24

EPS: $1.58, revenue $967m, a beat by $57m, virtually all sprung from gains in online sports betting. Overall, BYD posted a 5.5% revenue gain, led by a solid 52% rise in the online business segment. This online performance is evidence I believe that the rapid growth of the company’s online business compensated for much of the softness in some brick and mortar segments. It’s been somewhat soft across the entire regional segment and will work through the system as it always does, back to organic growth.

google

Source: BYD gaming archives.

Above: Like all great deals, it was a win-win for both companies.

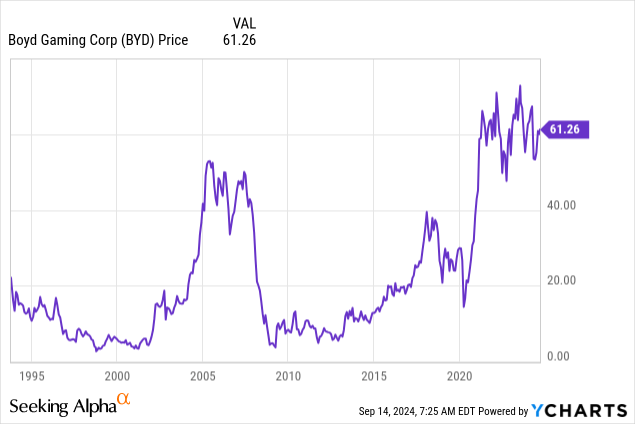

Above: Up, yes, but lots of run room ahead.

One key result we drilled deeper in amid lots of strong upside segments like online was the aforementioned softening during the period Jan-June 2024 in BYD’s Las Vegas locals market. This is a traditional strength of the company. During the earnings release call, management attributed the softening in locals revenue to a general “competitive” environment.

I think we need to go down for a granular look at that segment. There are two culprits here. One perhaps is the leading edge of what I call bankroll fatigue. It is a little cited or understood effect that visits gaming in little-noticed cycles. It contains the seeds of a bit of recession fear in public thinking. But mostly player concerns about playing too much. Players get “burned out” as we refer to this development. However, for BYD I believe the spearhead of the local market softness also has much to do with the debut of Red Rock Resorts (RRR) December 2023 upscale new locals property, the Durango.

BYD archives

Above: The Durango is a new, upscale property that has taken share in various degrees to the two entire locals market

My latest inquires among industry friends in Vegas have validated my feeling that the Durango has, in its early stage, poached share from BYD – others as well. It has just left the initial period when curiosity visitation is highest.

I’ve seen this competitive pressure sequence many times before. There are three phases of the impact of new, same market properties on existing market leaders. Phase one, Debut (December23) to first six months, which shows with considerably “gotta see” visitation to the new property. That is followed by the next six months, where trail visits have sunken into a pattern. Usually, we saw during this next Phase Two, as the wide majority of play that has sampled the new property begins to slowly return to where their mainstay was. And then we have Phase Three when the process ends in a permanent loss of some visitation – usually not massive – to either a sharing trends or a full return to the property previously selected first.

I have cited this phenomenon from my personal archives in a prior post, but that was early in the debut of Durango. This update from my discussions with industry friends in the locals market was conducted 10 days ago.

The 2Q24 earnings release to me indicated that the Phase one “gotta see” trial was responsible for a significant loss of payer visits. That’s the first six months of Durango. That would put the impact against BYD’s locals business all behind the market share poach. We are now at Phase two with a steady stream of customers returns. Revenue reports generally show lessening paces of lost business to going flat. And clearly a pattern of return of the “gotta see” testers. That will accelerate until Phase three, which I believe we will see resumed BYD organic growth pre-covid.

Overall regional performance of BYD properties across its entire system has many elements of the above-mentioned bankroll fatigue, based on the economic outlook of the regions.

Financially; BYD has proven to be among the most savvy asset allocators in the business. It’s transactional management mentality has served it well. Its 2003 50% partnership with MGM for the AC Borgata was exited with $990m, much proceeds diverted to acquisition of two Vegas locals properties that were priced right.

Although the company uses debt to finance current operations from time to time, its record is spotless in repayment or refis. It has $280m in cash and $3b in long-term debt. Its rumored effort to buy PENN Entertainment (PENN) with FLUT is not idle tire kicking. They have the flexibility and resources to do such a deal. BYD owns 5% of the equity in FLUT, which it traded for Fan Duel access to its 28 casinos in ten states. It was a win-win. Just on a dollar for dollar basis percentage, the BYD equity in FLUT has dramatically increased in value since 2020. We recall the home run BYD hit from 2003 when its 50/50 partnership with MGM on the billion dollar plus Borgata in AC resulted in a sale of its halfback to its partner for $900m.

The market cap of BYD at $5.88b is way undervalued just considering what its 5% of FLUT could fetch either in a sell back to FLUT or on the open market.

Summarizing

The Morgan Stanley upgrade (Sept 4th/NASDAQ report) is very well-timed given the expected explosion of NFL wagering that is off and running. BYD’s locked in position with FD is a proven market share leader. Its brick and mortar casinos are sustaining buffeting headwinds across the regional casino geography. Its financial structure is solid, its balance sheet clean and mostly, from my POV, the quality of its management is meeting and exceeding goals.

Don’t downplay the chances for a deal on Penn. It’s a great fit all around. Of course, it’s far from happening now and may never happen. But the intention of BYD and FLUT clearly signal they are not satisfied to sit on what they have. As noted above, BYD cashed out its Borgata partnership, selling it to MGM. If you see this as an entry into the gaming sector, you could find a better stock to be in now. The balance in locations, the financial stability and the strategy which has worked for decades are for sale at a good entry point now.

Credit: Source link

{kind=link}