JHVEPhoto

8×8, Inc. (NASDAQ:EGHT), the SaaS cloud communications solution provider, has continued reporting stable revenues not showing signs of meaningful top line growth. My previous article on 8×8, titled “8×8: Waiting For A Growth Recovery”, went over 8×8’s overall financial profile and the company’s recently lacking growth. No signs of growth resuming has since been reported, as 8×8 continues to try to improve its offering’s appeal.

In the previous article, I initiated 8×8 at Hold as the valuation seemed to a resume into reasonably modest growth. Since the previous article was published, 8×8 has lost -45% of its value compared to the S&P 500’s return of 16%. The valuation now shows clearly lacking faith in any turnaround into growth, adding potential for a deep value play. Still, the deep value play is unlikely for the time being, making further stock declines very possible.

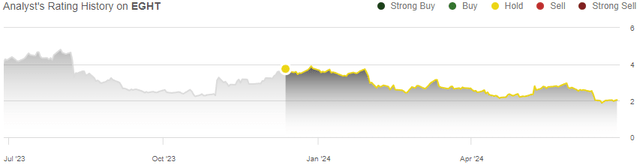

My Rating History on EGHT (Seeking Alpha)

There Isn’t a Growth Recovery in Sight Yet

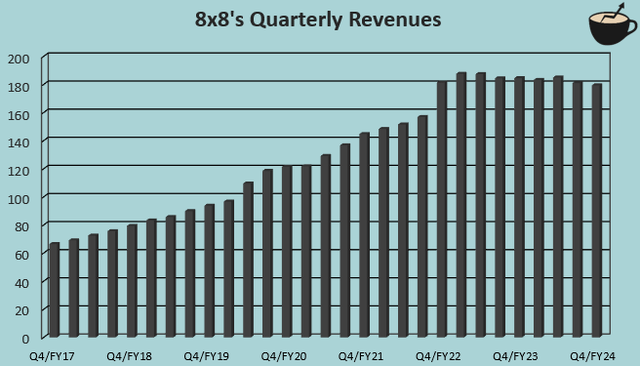

8×8 has continued to report slightly sequential declines in revenues. In Q4/FY2024, revenues reached $179.4 million, down -0.9% sequentially and by -2.8% year-over-year – the revenue stagnation has remained after the FY2022 acquisition of Fuze with no end in sight yet. The XCaaS revenues, which Fuze was integrated to including UCaas and CCaaS revenues, are still performing better with slight growth as the offering’s revenues grew from 41% in Q1 into 43% in Q4.

Author’s Calculation Using TIKR Data

The company doesn’t yet see a growth turnaround in sight. With the Q4 report, 8×8 initiated a financial outlook for FY2025 expecting total revenues of $720-738 million, with the middle point implying stable revenues from FY2024. Revenues in Q1 are expected to likely drop slightly.

Due to the lower sales, the adjusted operating margin is expected at 11.5-13.0% in FY2025, compared to the achieved 13.0% in FY2024 – sales mainly drive 8×8’s margins as the cost base is based on predominantly fixed costs.

Losing the Battle Against Competition

While the Covid pandemic clearly boosted the need for remote contact centers temporarily in prior years, the recent lacking growth isn’t due to industry weakness; competitors continue to post good top line growth even after the pandemic. RingCentral (RNG) grew total revenues by +9.7% in the same period as 8×8’s FY2024 revenue decline of -2.0%. NICE Ltd. (NICE) continued on momentum with +10.7% revenue growth in the same period, and Five9 (FIVN) grew by +15.3%.

8×8 clearly notes the company’s underperformance and is working on solutions to return to top line growth. In the FY2024 10-K filing, 8×8 communicates that the company is currently working on reducing cost of delivering services, improving sales efficiency through an intensified focus on mid-market and enterprise customers where the XCaaS platform provides the best value, and improving the offering through increasing R&D investments. Partner programs have also been extended to drive better reach in markets.

Kevin Kraus, 8×8’s CFO, expressed in the Q4 press release that the company is currently building a foundation for future growth. Yet, no signs of growth are yet seen in the FY2025 guidance; the return to growth looks to happen in FY2026 earliest. Investors should in my opinion be skeptical, as it seems that the likelihood for a return to growth is small given the recent performance.

Further cementing a bearish base scenario, multiple 8×8 insiders have continuously sold shares in the company, most recently on the 17th of June.

High Stock-Based Compensation Eats Equity

8×8 compensates employees with share incentives, and at the current valuation, continued high stock-based compensation quickly eats away shareholders’ equity in the company. The company had $61.9 million in total SBC in FY2024, now representing 24.1% of the total market cap of $257.0 million at the time of writing.

The dilution hasn’t been very rapid historically with a CAGR of 3.1% in diluted outstanding shares from FY2015 to FY2024, but the lower share price now poses a greater threat. Because of the threat of significant dilution, I believe that a short- to mid-term growth recovery is likely critical to not cause very significant dilution.

The 8×8 Stock Prices In Stagnant Revenues

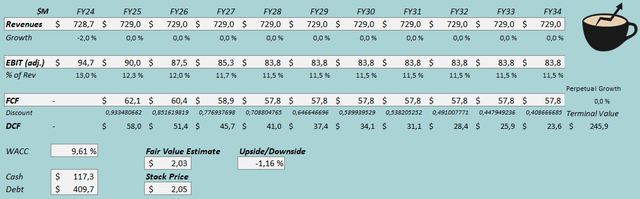

The stock currently prices in stagnant revenues – I updated my discounted cash flow [DCF] model to represent a base scenario. In the scenario, I now estimate flat 0% growth going forward, and for cost inflation to push the adjusted EBIT margin to an eventual stable level of 11.5%.

I previously accounted 8×8’s SBC as negative cash flows as they dilute shareholders, but now rather estimate a 30% total share count dilution and exclude SBC from cash flows, improving the shown cash flows into quite a good level.

Base Scenario DCF Model (Author’s Calculation)

The estimates put 8×8’s fair value estimate at $2.03, near the stock price at the time of writing. For investors, slight negative growth in real terms seems to be the base scenario, continuing the guided FY2025 performance into perpetuity. I believe that the represented DCF model scenario is very likely, but a return to growth could make the stock significantly more valuable, leveraged by the high remaining debt of $409.7 million.

8×8’s Potential Deep Value Play

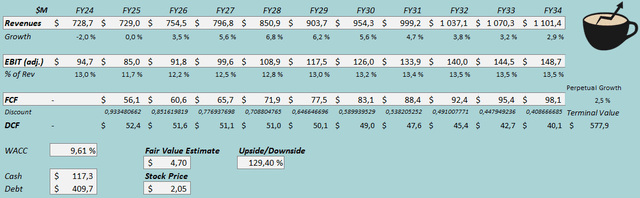

If 8×8 returns to growth, the stock’s current price could represent a deep value opportunity – at a gradual growth recovery from FY2026 forward, estimating a revenue CAGR of 4.2% from FY2024 to FY2034 and 2.5% perpetual growth afterwards, the stock would have immense upside. With the growing sales, 8×8 would likely experience operating leverage that I estimate to raise the adjusted EBIT margin into 13.5% in the more bullish scenario.

Bullish DCF Model (Author’s Calculation)

The more bullish scenario pushes 8×8’s fair value to $4.70, 129% above the stock price at the time of writing. The market seems highly skeptical of 8×8’s ability to resume growth, which I believe to be a fair base scenario especially considering continued insider sales. Investors should still note the potential deep value play – my bullish DCF model doesn’t estimate growth anywhere near 8×8’s historical rate, yet estimates very high upside.

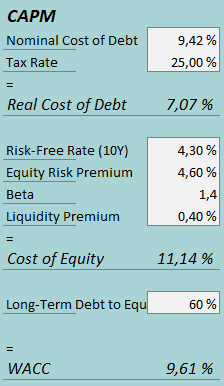

CAPM

A weighted average cost of capital of 9.61% is used in the DCF models. The used WACC is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

In Q4, 8×8 had $9.7 million in interest expenses, making the company’s interest rate 9.42% with the current amount of interest-bearing debt. I now estimate a long-term debt-to-equity of 60% instead of 40% previously as the equity valuation has declined dramatically, only partly countered by debt paydowns.

To estimate the cost of equity, I use the United States’ 10-year bond yield of 4.30% as the risk-free rate. The equity risk premium of 4.60% is Professor Aswath Damodaran’s latest estimate for the United States, updated on the 5th of January. I have kept the beta estimate at 1.40. Finally, I add a liquidity premium of 0.4%, creating a cost of equity of 11.14% and a WACC of 9.61%.

Takeaway

8×8’s stagnant revenues have continued as the company is losing against competition. The company guides for the stagnancy to continue in FY2025 while the company communicates to be building a foundation for future growth. The likelihood of a growth return now seems to be low, though, which the market seems to price in after the crash. Insiders seem to agree, as multiple 8×8 executives have continued to sell shares in the company.

A mid-term recovery could pose a great deep value play before high SBC dilutes shareholders’ equity too significantly, but such a scenario seems unlikely. The stagnant revenues are priced to continue, and unless 8×8 starts to grow again, I believe that a Hold rating is again justified. Investors should closely watch how the story evolves, though, as the stock’s potential could be huge.

Credit: Source link

{kind=link}