z1b

Earnings season is a great time to pick up stocks that one has been eyeing for some time, as results or guidance that disappoint Wall Street can create opportunities to buy quality companies at discounted prices. This is because market reactions to earnings can often be exaggerated, causing stocks to drop more than they should.

In addition, earnings season can also provide insights into the overall health of specific industries and sectors. By analyzing the performance of multiple companies within a particular industry, investors can gain a better understanding of any potential trends or challenges that may be affecting the sector as a whole. This can help the long-term investor to make an informed decision on whether the market reaction is justified.

This brings me to the following two picks, both of which have fallen materially as of late, creating attractive entry points for investors who have a long-term investment horizon. Both carry moat-worthy attributes in their own right, and above average dividend yields. In this article, I highlight why each is an appealing ‘Buy’ at their present discounted valuations, so let’s get started!

#1: Prologis – 4% Yield

Prologis (PLD) is a global logistics leader with a focus on high-growth and high barrier-to-entry Tier 1 markets. At present, it has 1.2 billion square feet in owned real estate and development projects combined. It has a presence in 19 countries and serves 6,700 customers in its B2B and Retail/Online fulfillment categories.

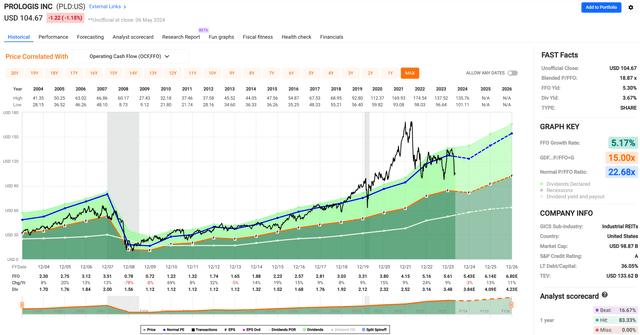

Prologis has seen a sizable pullback in its share price in recent weeks, from $135 in May to $104.67 at present. As shown below, PLD’s price is down by 16% over the past 12 months.

PLD Stock 1-Yr Trend (Seeking Alpha)

Despite the share price underperformance, PLD continues to churn out reliable returns. This includes Same Store Cash NOI growth of 5.7% YoY during Q1 2024, results of which were released on April 17th. Notably, SSNOI would have been higher by 175 basis points at 7.45% when one-time items are excluded. This was driven by continued high demand for its properties, with rent growth of 70% new leases signed during Q1.

Occupancy also remains strong at 96.8%, and while this is lower than what PLD saw a couple years ago, its decline of 80 basis points since 2022 is far more muted than the 310 bps decline for the overall U.S. industrial property market over the same time frame.

Risks to PLD include slowing growth, driven in part by inflationary pressures on the consumers. This is reflected in management’s guidance for occupancy to land at 96.25% at the midpoint of the range by the end of 2024, implying a 55 bps drop in occupancy from the present level. In addition, management adjusted down full-year 2024 SSNOI growth by 150 bps to 6.0% at the midpoint.

While the operating environment looks to be challenging for 2024, management expects the supply-demand imbalance to continue to benefit the sector as demand is expected to stabilize by the end of this year and early next year. Moreover, PLD has catalysts from its burgeoning energy business, as it recently signed 405 MW of long-term storage contracts with investment grade-rated utilities. It also delivered the largest EV fleet charging project in the US that’s within 15 miles from the ports of Los Angeles and Long Beach.

Importantly, Prologis carries a strong balance sheet with an ‘A’ credit rating from S&P. This enabled it to raise $4.1 billion of debt so far this quarter with a weighted average interest rate of just 4.7% over a 10-year term, which is impressive for this high interest rate environment. This brings its liquidity to over $5.8 billion to fund its development pipeline, which is estimated to carry a stabilized yield of 5.7%, sitting above PLD’s cost of debt.

Importantly for income investors, PLD’s share price downturn has raised its dividend yield to 3.7%. The dividend is well-protected by a 70% payout ratio and comes with a 5-year CAGR of 12.6% and 10 consecutive years of growth.

Lastly, I find PLD to be good value at the current price of $104.67 with a forward P/FFO of 19.5, sitting below the 21.5 P/FFO mark from when I last visited the stock in August of last year, and below its normal P/FFO of 22.7. While PLD is more expensive than peer Rexford Industrial’s (REXR) 18.8 P/FFO, another favored Industrial REIT of mine, I believe PLD warrants a higher valuation due to more geographic diversification than just Southern California.

FAST Graphs

The recent slowdown in PLD’s operating fundamentals has made me slightly more cautious, but I maintain a ‘Buy’ rating on the stock. This is based on my belief that the current headwinds are transient in nature, with low new supply coupled with strong demand being growth drivers for the company over at least the medium term. Analysts estimate 10-12% annual FFO/share growth, thereby supporting my belief that PLD deserves to trade at least at its historical P/FFO as mentioned earlier.

#2: Crown Castle – 6% Yield

Crown Castle Inc. (CCI) is one of the three major players in the cell tower industry, alongside peers American Tower (AMT) and SBA Communications (SBAC). Its sizable presence includes 40K cell towers and 90K route miles of fiber supporting small cells and fiber solutions across every major U.S. market.

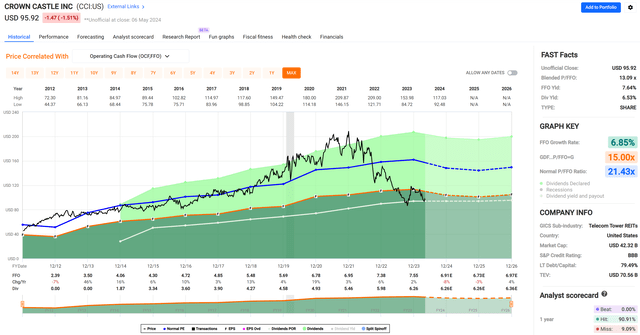

Like Prologis, CCI’s share price has also fallen materially in recent months, from $113 in March to $95.92 at present. As shown below, CCI stock sits 18% below where it was just 12 months ago.

CCI Stock 1-Yr Trend (Seeking Alpha)

One of the reasons for why CCI stock is down may be due to market misperceptions around a 2% YoY decline in site revenue during Q1 of 2024, results of which were released on April 17th. It’s worth noting that this decline was due to $50 million worth of Sprint cancellations after its merger with T-Mobile (TMUS). On an organic basis, CCI actually saw 5% YoY revenue growth, driven by 4.6% growth from towers, 16% growth from small cells, including $5 million of higher than expected non-recurring revenue, and 2% growth from fiber solutions.

Management is guiding for 5% organic revenue growth for the full-year 2024. This includes 4.5% growth for towers (compare to 5% growth in 2023), 13% growth from small cells, as CCI plans to add 16K new billable nodes this year, and 3% growth from fiber solutions, which compares favorably to flat growth in 2023.

CCI has also taken steps to strengthen its balance sheet in this higher interest rate environment. This includes having $6 billion in liquidity on its revolving credit facility, which more than covers just 8% of its debt maturing between now and the end of 2025. Management has also extended weighted average maturity on debt from 5 to 7 years, and since 2015, it’s reduced secured debt from 47% to 6% and increased the percentage of fixed rate debt from 68% to 90%, thereby supporting its BBB credit rating from S&P.

Risks to CCI include uncertainties around its fiber solutions, which may be viewed as being a distraction away from its core business of cell towers. Fiber is a tougher business to be in, as CCI competes with the likes of AT&T (T) and Verizon (VZ), which have their own fiber networks in major metropolitan areas. Moreover, CCI faces uncertainties from capital spending plans by the Big 3 telecoms, as the timing of incremental spend around their 5G networks may change based on their capital plans.

Importantly for income investors, CCI currently yields an appealing 6.5%. It’s worth noting that CCI’s dividend payout ratio is elevated at 91% based on management’s AFFO/share guidance of $6.91. I would expect for the payout ratio to improve with time, however, as CCI moves on past the Sprint churn and as organic growth continues to kick in.

Lastly, I continue to see good value in CCI at the current price of $95.92 with a forward P/FFO of 14.0, sitting below the P/FFO of 15.3 from when I last visited the stock in January of this year, and below that of peers AMT’s 17.2x P/FFO and SBAC’s 15.3x P/FFO. As shown below, CCI’s current valuation is also well under its historical P/FFO of 21.4.

FAST Graphs

My ‘Buy’ thesis around CCI remains largely unchanged from last time, considering that near-term headwinds around the Sprint cancellations are largely overblown considering the market price reaction. CCI is expected to produce healthy organic growth with the backing of its moat-worthy asset base. As such, I would expect for CCI to be able to produce at least mid-single digit FFO/share growth, which combined with the current dividend yield could produce market-beating returns in the low-teens.

Investor Takeaway

Both Prologis and Crown Castle continue to be high-quality REITs that I believe offer good value at current prices. Though they face near-term headwinds, their long-term prospects remain strong due to favorable industry dynamics and solid fundamentals. In the meantime, investors get to collect well-above market average dividend yields ranging from 4-6% with expected growth in the future. As such, I believe both PLD and CCI present excellent Buy-and-Hold opportunities at their current prices.

Credit: Source link

{kind=link}