denisik11/iStock via Getty Images

Zscaler (NASDAQ:ZS) leads the Security Service Edge market, expected to grow 20-30% over the next five years. I expect billings to bottom in F4Q24/F1Q25, as changes in the sales motion take effect. Investors price the shares for 15-20% Gross Profit growth. Street estimates 23% Revenue growth in the next two years. Yet, billings and current RPO sit above 25%. I expect 25-30% GP growth over the next two years, which should earn Zscaler a higher multiple, resulting in 32% upside from here.

The Download

In 2007, Jay Chaudhry and K. Kailash founded Zscaler to offer network security solutions adapted to cloud computing. Already a successful entrepreneur by then, Jay bootstrapped the company, only accepting VC money in 2012. The company IPOed in Mar-18. Jay Chaudhry remains at the helm.

Zscaler thesis is that the pervasive use of SaaS, alongside an increasingly hybrid workforce, shifts the traditional model of securing a network based on perimeter vs. core, to connecting the right users to the right applications, securely, regardless of the network. That translated into two solutions: Zscaler Internet Access (ZIA) and Zscaler Private Access (ZPA).

ZIA securely connects users to external applications, regardless of device, location or network. ZPA securely connects authorized users to internal applications, replacing Virtual Private Networks (VPNs) and other solutions. Zscaler Zero Trust Exchange platform supports both services. It consists of a datacentres network sitting between users and the internet. It ensures malware does not reach the user, nor corporate data leaks out.

ZIA and ZPA represented 82% of FY23 Net New ACV. Zscaler complements these core offerings with:

- ZDX, a service optimising user experience

- Zscaler Data Protection, securing data-in-motion and data-at-rest

- Zscaler for Workloads identifies and remediates cloud service, application, and identity misconfigurations for assets deployed in public cloud infrastructure such as AWS, Azure or GCP

- Zscaler for Branch/Factory

- Risk360

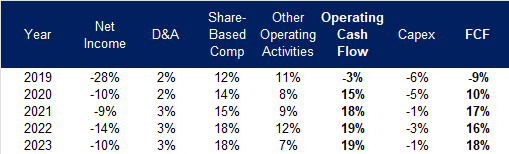

In the last three years, the company has grown Sales at a 49% CAGR, delivered gross margins of 77-79%, reduced Opex/Sales from 109% to 85%, mostly through S&M – 2900bps of reduction -, and G&A (700bps of reduction). FCF/Sales increased to 21% from 6% in 2020, with a 2024 target in the low to mid-20% range. There is a lot of dilution at Zscaler; the company guides 161m weighted diluted shares in FY24, compared to 145m in FY23.

Figure 1: FCF Generation at Zscaler

Zscaler 10Ks

Focused on Deepening Within Accounts

At the 2021 Analyst Day, management laid out a $49bn Serviceable market (SAM) for ZIA/ZIA Add-ons/ZPA/ZDX, based on 335m users in the 20k organizations with 2k+ employees that Zscaler targets in the Enterprise segment, times $145 ARPU. Zscaler highlighted $23bn in SAM for Zscaler for Workloads, based on 150m serviceable workloads at top public clouds and $155 per workload, including $40 for Cloud Security Posture Management (CSPM), $60 for Workload Segmentation and $55 for Workload Communication. Earlier this month at Zenith Live 2024, management increased the TAM adding DLP ($10bn), Zero Trust for Branch/Factory ($12bn) and Risk360 ($2bn), to a total of $96bn.

To fulfil these ambitions, Zscaler adopted new pricing mechanisms adapted to how customers consume the new products. Subscription pricing remains primarily calculated on a per-user basis, with an increasing portion of sales linked to workloads. Besides, with a much wider portfolio of solutions, they focus on going deep with customers. There are positive signs. The company has 41m users and $2bn+ in ARR, implying $48 per user; compared to $1.5bn in ARR at the end of FY23, and 40m users, implying a $38 ARPU.

Zscaler hired new Go-to-market leaders on Nov-23, fit for a $5bn ARR target. Sales motion is changing from opportunity-centric to account-centric, focusing on enterprise cross-sell under the new CRO, Mike Rich, who spent 12y at ServiceNow, lastly as President for Americas.

Investing in an enterprise software amid changes elevating execution risks is tricky and investors are unforgiving. The following print did not reassure. When Zscaler reported F2Q24 on Feb 29th, investors grew concerned about billings growth deceleration – 37% in FY23 to 26% in FY24 -, lower than usual beat, and the large sequential increase in 4Q necessary to achieve FY24 billings guidance. After peaking at $253 in Mid-Feb, shares declined to $170 over the course of two months.

Since then, Zscaler reported excellent F3Q24 earnings on May 30th; billings accelerated to 30% YoY (vs 27% in prior quarter), in a context of weak software results, and with shares down 35% in the prior 3m. Management tampered FY25 billings expectations, citing a few points of headwind due to higher-than-expected attrition in F3Q and the timing of new hires over the next 6 months. Zscaler expects attrition to stabilize in 4Q and sales capacity to be fully ramped by 2H25.

Following this set of results, all analysts are revising FY1 upwards, so Zscaler ranks well on Seeking Alpha Revisions score at A+. Importantly, analysts have not revised FY25 and FY26 Revenue expectations aggressively; these barely changed in the last six months. Zscaler will provide FY25 billings guidance in early September when they release F4Q24 results.

Consensus currently sees 23% YoY Rev growth in FY25 and the same in FY26. Yet, calculated billings and current RPO growth have remained above 25% for the last four quarters. Besides, if FY25 experiences headwinds due to lower productivity, then FY26 will benefit from an easier compare and could accelerate from the previous year.

The Set-Up

Investors are not underwriting potential acceleration from increased sales productivity and wider product set. Valuation is low relative to history and relative to fundamentals. The company is priced at the low-end of its historical range. And revisions have yet to pick up. Zscaler fits my goal of seeking companies able to deliver better than expected results, which stocks are not yet discounting that possibility.

Figure 2: EV/Sales low relative to history

Koyfin

I have explained before that ARPU went from $38 to $48 during FY24. Since Dollar-based Net Retention has decreased during that timeframe, from 117% to 116%, I believe the increase in ARU to comes from landing more products at new customers, rather than an increase among existing customers. That benefit has yet to come.

In our conversations with resellers and global system integrators, they agree Zscaler remains the leader in SASE, the most innovative due to its focus on Zero-trust. This is also regularly highlighted by industry experts like Gartner. Earlier this year, Dell’Oro predicted the SASE market would reach $16bn by 2028, a 12% CAGR, with Single vendor SASE growing 17%. That is the market Zscaler operates in. Gartner predicted a 30% CAGR for SASE to 2027. Zscaler is doing well in its core market, which will grow 20-30% in the next few years. Changes to the sales motion are building momentum yet to be reflected in fundamentals.

By layering on top of the core products DLP, Zero Trust Branch and Risk 360, Zscaler will gain a few additional percentage points of growth. Channel feedback on DLP is that it will be on par with leaders in the space in the next year. Zero Trust Branch seems a natural extension for the company, used to sell to network teams within the CISO organisation.

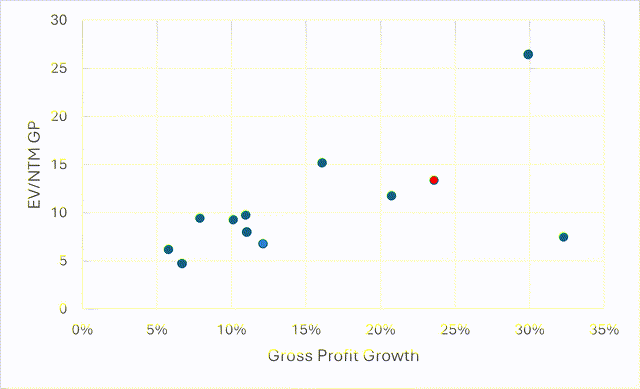

From a relative valuation standpoint, investors bake 15-20% Gross Profit growth. I see low risks to FY25 expectations. Given trends in billings, current RPOs, competitive position, larger lands, and increased productivity throughout FY25, I expect sales to accelerate from F4Q24 or F1Q25, bottoming out around 22% YoY. I expect 24% Gross Profit growth in the next 12m and 28% in the following 12m. This should warrant a 16x EV/GP, on $2.4bn of GP (F4Q25-F3Q26), or $39bn in EV, with $500-$600m more in the bank coming from FCF, and 7% dilution; I end up with a price target of $244, a 32% increase.

Figure 3: Investors baking in 15-20% GP growth (red dot)

Author calculations based on current price and estimates

Risks

Consolidation Risk

Larger competitors Palo Alto Networks (PANW) and CrowdStrike (CRWD) seek to consolidate customers’ spending on their platform. They have developed their offering to capture adjacent markets. This could cause in the long-run market share loss, and in the short-term longer sales cycles as customers pause to rethink their technological roadmap.

New Comers Aggression

Netskope and Cato Networks are private competitors. They are well-regarded by buyers and industry analysts. Thy have received significant funding in the last 18m. Netskope raised $401m in convertible debt last year, and recently crossed $500m in revenue. Cato raised $238m last September.

Execution Risk from Changes in Sales Motion

The early signs are encouraging, but the changes to the Zscaler sales model to account-centric will reduces sales productivity in the short term. Such reduction will impact FY25 billings guidance, a key number scrutinized by investors in the upcoming earnings results. There is a chance they disappoint.

Conclusion

Zscaler represents an attractive opportunity among high-quality large cybersecurity vendors. It has more potential to surprise positively than CrowdStrike or Palo Alto Networks and carries less competitive risk over the next six months. I see the potential to benefit from multiple expansion and earnings growth. Revisions are positive and accelerating. I think it will continue in 1H25. Near-term disappointment risk exists, but I see decent upside on a 12m view.

Credit: Source link

{kind=link}