RHJ

Overview

Yellow Cake (OTCQX:YLLXF) is a passive uranium investment vehicle that has its primary listing in the UK. I have covered the company frequently and it has been core part of my portfolio for most of the last five years. My prior articles on Yellow Cake can be found here.

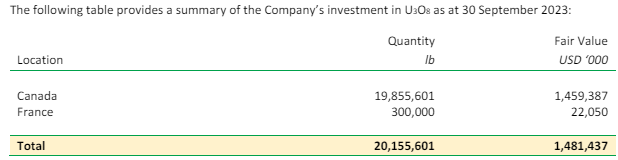

Figure 1 – Source: Yellow Cake Interim Financial Report

The company owns uranium that is stored in Canada and France and on the 4th of June announced that it has taken delivery of the last 1.5Mlbs of uranium purchased from Kazatomprom. Yellow Cake now holds 21.7Mlbs of uranium stored in the two locations, with most of it in Canada.

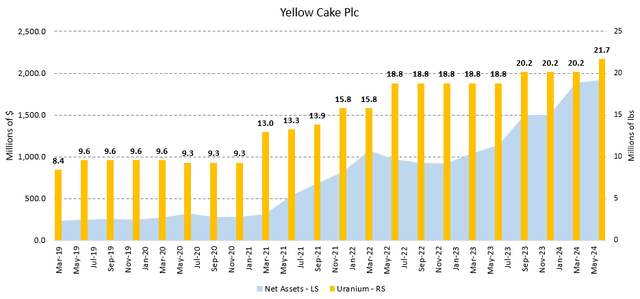

This is up from 8.4Mlbs of uranium a little over five years ago, which equates to an increase of close to 160%. However, Yellow Cake’s net asset growth has been substantially higher during this period, with an increase of just over 750% due to the strong commodity price trend for uranium.

Figure 2 – Source: Quarterly Reports

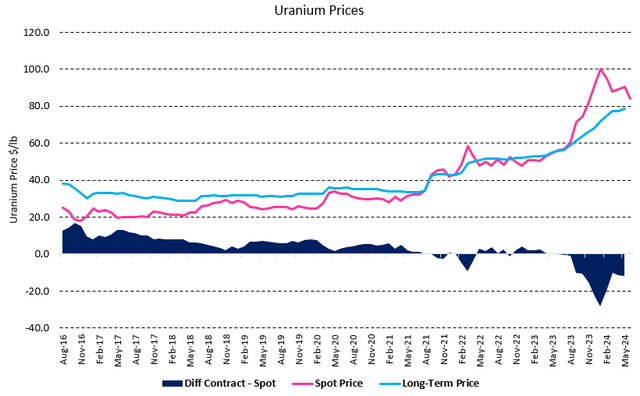

The spot price of uranium was most recently reported at $84.25/lb by Numerco, which isn’t that far off the long-term contract price of $78.5/lb at the end of last month. So the divergence between the spot and contract prices that we have seen over the last year has now started to close.

One might consider the contract price the more accurate reflection of the uranium market, because most uranium transactions are done in the contract market. However, there are some issues with how contract prices are reported, which I discussed in more details in this recent article on Yellow Cake. I prefer to look at both the spot price and the reported contract price, together with additional information on price levels occasionally shared by uranium-producing companies.

Figure 3 – Source: Cameco & Numerco

Recent Developments

One very interesting uranium industry development is the U.S. ban on uranium imports from Russia, which will take effect in mid-August. The ban also unlocks $2.7B in federal funding to the uranium industry in the U.S. This is likely to lead to higher uranium prices in the west, at least on the margin, even if we haven’t see much of short-term reaction in the market. This news has been expected for a while, so it is fair to assume that market participants have had a few months to prepare.

Not too long ago, nuclear energy was far from popular, but we have lately seen a reversal in that regard in many countries. The latest wording from the U.S. Secretary of Energy of tripling the nuclear capacity in the U.S. is a good illustration of the increase in popularity, even if more concrete plans are still needed.

To reach our goal of net-zero by 2050, we have to at least triple our current nuclear capacity in this country. That means we’ve got to add 200 more gigawatts by 2050.

So, it begs the question why the spot price of uranium has declined year-to-date, and equities have been weak over the last month? 2023 was a strong year for uranium and the related equities, so some level of consolidation was always due to happen. I suspect the weak oil price and poor sentiment among many mining stocks over the last few weeks have played a part as well.

I prefer to zoom out over a multi-year perspective, where uranium prices and Yellow Cake looks to be in a very constructive long-term bull market, and I view the recent weakness as a minor cyclical correction in a long-term secular uptrend which is fueled by strong and growing demand from the nuclear industry and a delayed supply response by miners.

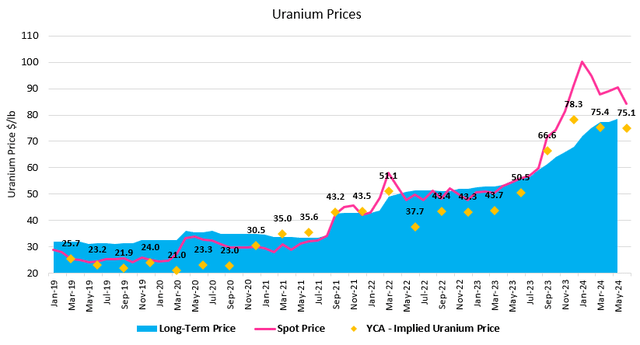

Figure 4 – Source: Yellow Cake Quarterly Reports, Cameco & Numerco

Valuation & Conclusion

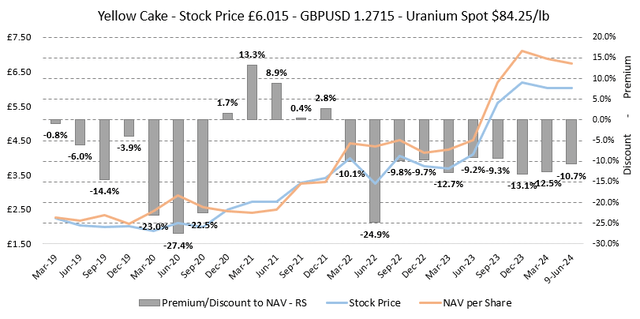

Yellow Cake has over the last couple of years traded with a persistent discount to net asset value (“NAV”) of around 10%. The discount to NAV is presently at 10.7%, which equates to an implied uranium price of $75.1/lb.

Figure 5 – Source: Multiple Sources

Even if we have seen the discount to NAV persist for some time, I do think the current poor sentiment plays a part as well. One possible argument for the discount has been the possibility that Kazatomprom would fail to deliver on the uranium purchases. With the recently announced delivery, that risk should no longer be a consideration.

Yellow Cake has no financial leverage and minimal operational risk. Uranium and uranium equities have been somewhat correlated to the overall market and energy prices in general. So, the largest risk with an investment in Yellow Cake is likely a correction of the overall market, which would in the short-term impact the stock price of Yellow Cake as well.

However, with an implied uranium price of $75.1/lb and very few large uranium mines coming online in the next few years, I still view the upside risk larger than the downside risk for uranium and consequently Yellow Cake.

I view Yellow Cake as a “buy” here and I am long the stock. I expect we will see a higher uranium price over the next few years, and I also think the discount to NAV will decrease ones the sentiment improves, even if I wouldn’t expect the discount to remain at zero, at least unless Yellow Cake more actively try to enforce it via buybacks.

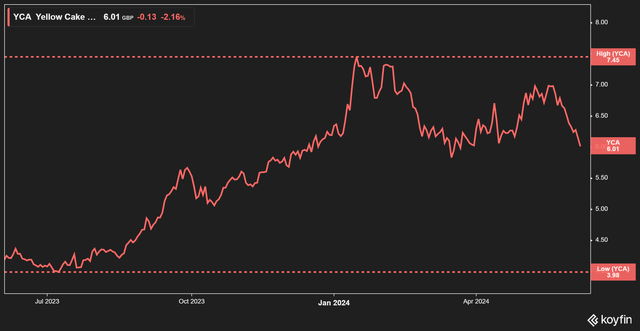

Figure 6 – Source: Koyfin

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Credit: Source link

{kind=link}