Feverpitched

Historically, investors have had three main options to invest in real estate:

- Buy a rental property

- Invest in a private real estate fund

- Buy shares of a REIT.

But lately, a fourth option has become increasingly popular, and that is that of real estate crowdfunding. They are online platforms that pool capital together from many investors to make real estate investments.

They are quite similar to traditional private real estate funds, but the main difference is that they are often open to unaccredited investors, allowing anyone with as little as $10 to participate in their deals.

Many of these platforms really took off following the pandemic, when interest rates were ultra-low and amassed $100s of millions or even billions of assets under management (“AUM”). Today, some of the biggest ones are:

- Fundrise

- RealtyMogul

- Crowdstreet

- YieldStreet

- Arrived

- Cardone Capital

- Etc.

Fundrise

But I think that they are poor investments in most cases.

I believe that most of these platforms exist mainly to milk fees off unsuspecting individual investors. They use slick marketing to raise capital, but they have no competitive advantage and offer disappointing risk-adjusted returns when compared to other alternatives.

REITs (VNQ), in particular, are a far better option for the vast majority of investors.

They are not only safer, but also more rewarding, and here are 8 reasons why:

Reason #1: Significant Conflicts of Interest

It all starts with this. The main problem with real estate crowdfunding platforms is that they are asset management businesses that exist for one purpose: to earn fees from investors.

They use the classic “external management” structure in most cases with a fee structure that typically includes:

- An asset management fee

- An acquisition fee

- A loan origination fee

- A disposition fee

- A potential incentive fee.

And for that reason, they are incentivized to raise as much capital as possible to maximize fee income and profits for themselves. Therefore, their incentives aren’t aligned with those of the investors.

Today, most REITs use an “internal management” structure that eliminates fees and better aligns the interests of the management and shareholders. What this means is that the management is hired as employees of the REIT, and they earn salaries for their dedication to the REIT. These salaries are then tied to some key performance indicators such as the returns of the REIT, rather than just the volume of assets under management.

There is only a minority of REITs that are externally managed, and they are typically priced at a large discount relative to the internally managed ones, and have earned much lower returns over the long run due to this one difference.

Yet, most crowdfunding platforms are externally managed and investors don’t seem to care.

Reason #2: High Fees Masked as Low Fees

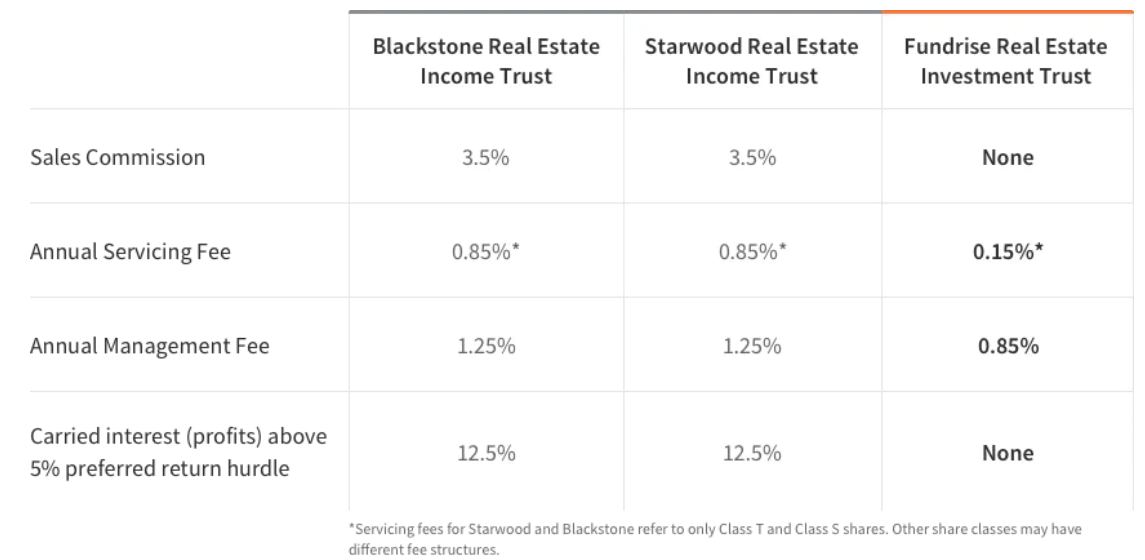

Crowdfunding platforms will often promote themselves as a “low fee” option for investing in real estate. They will use aggressive marketing strategies and often compare themselves to a cherry-picked real estate fund or REIT that suffers high fees and show that: “look, we are a lot cheaper.”

Fundrise does a lot of that. Just look at the below table which they display on their website:

Fundrise website

But the reality is very different.

Fundrise charges a 0.85% asset management fee. Then they charge a 0.15% advisor fee. Finally, they have other fees depending on the vehicle.

In comparison, the average management cost of public REITs is only around 0.5% annually, or about 2x lower than Fundrise:

Public REIT fees

REITs are so much more cost-efficient because their internal management structure affords much greater economies of scale.

The management earns salaries that are based on the actual performance of the REIT and not just the volume of assets under management. Therefore, as the REIT grows larger, the management cost as a percentage of assets goes down.

But crowdfunding platforms typically charge a fixed fee, and this fee does not change as they grow larger. That is a big issue because real estate is a highly competitive, low-margin business in which scale matters.

Reason #3: Too Much Leverage

Again, because of these same conflicts of interest, crowdfunding platforms will often take on too much leverage.

They are in the business of earning fees, and they maximize those fees by managing more assets.

They are then incentivized to take on a lot of leverage to grow the volume of assets under management.

They will not hesitate to use 60-70% LTVs on their properties, and this has already pushed many of these deals into bankruptcy. Some of the biggest crowdfunding platforms have even gone under because of this reason.

REITs, on the other hand, learned their lesson from the great financial crisis and have been using much lower leverage ever since. Today, most REITs have an LTV in the 30-50% range.

It boosts returns during the good years and allows them to play offense during times of crisis, picking up properties from distressed sellers like overleveraged crowdfunding platforms.

Simply avoiding catastrophic scenarios helps them achieve better risk-adjusted returns over the long run.

Reason #4: No Competitive Advantages

As we mentioned earlier, real estate is highly competitive. It has low barriers to entry and it is a low-margin business.

Therefore, it is key to have a competitive advantage if you want to earn above-average returns.

REITs typically achieve this by focusing on one specific property type, becoming absolute experts in it, developing superior relationships within their niche, and then using their superior scale to their advantage to attract the best talent to work for them. They will then often develop their own properties to earn superior returns and use their relationships to attract the best tenants and draft their own lease agreements.

Crowdfunding platforms typically do none of that.

Most platforms like Fundrise don’t have any specialization. They invest in all sorts of properties, becoming jacks of all trades in a sense. Their knowledge and relationships then aren’t at par with specialists, and their smaller scale makes them less competitive.

The best talent in real estate will typically want to work for REITs or major private equity companies like Blackstone (BX), and not crowdfunding platforms.

Reason #5: Poorer Access to Capital

Another issue is access to capital.

REITs have a major advantage because their public listing allows them to efficiently raise capital with a low cost. They can sell shares to raise common equity or even preferred equity. They can use mortgages, bonds, convertibles, etc. Furthermore, they have plenty of options and it is a quick and efficient process.

In comparison, crowdfunding platforms have to deal with a much slower and less efficient capital-raising process. They will use their own website to privately raise capital.

Put yourself now in the shoes of a property seller. Would you rather sell your property to a crowdfunding platform that may need a few weeks to raise the capital? Or would you prefer to sell it to a REIT that has a big line of credit to buy your property and can then later sell shares later to pay off the line of credit?

The capital raising process of the REIT is far more efficient, and it affords them access to better deals. It also lowers their cost of capital, resulting in larger spreads.

Reason #6: No Liquidity… No Control… No Problem

Typically, one major advantage of REITs is their liquidity, but some investors dislike the lack of control.

On the flip side, investors like the feeling of controlling a private real estate investment, but they are then lacking liquidity.

Well… Crowdfunding platforms combine the worst of both worlds.

No liquidity and no control.

This is a major issue because it will make it very hard for you to exit your investment if the thesis changes and/or you need the capital for something else.

Liquidity and control are greatly underappreciated, until you need it.

Reason #7: REITs Are Much More Dynamic

Most crowdfunding platforms make an investment, collect rental income, and then wait for the property to gain value, hoping to sell it 10 years later at a profit. At most, they may make some slight improvements to the property in hopes of creating additional value.

REITs are much more dynamic than that. They will commonly develop their own properties from scratch to earn higher returns. To give you an example, the likes of Cardone Capital were buying apartment communities at very low cap rates in the years preceding the surge in interest rates, but Camden Property Trust (CPT) was able to develop its own properties at much higher cap rates.

Beyond that, REITs will also often earn additional profits from other real estate-related businesses, and shareholders then participate in these profits as well. As an example, some REITs offer brokerage and property management services to other investors. Others also offer construction services and/or asset management services.

Crowdfunding platforms don’t let their investors participate in these additional profits. They keep them for themselves.

Reason #8: REITs are Far Cheaper Today

This is perhaps the most important reason today.

REITs have crashed and are today priced at their lowest valuations since the great financial crisis, with many REITs trading at a ~30-40% discount relative to the fair value of their properties.

To give you an example, BSR REIT owns apartment communities in Texas. It has a great balance sheet, its rents are growing, and the management is the biggest shareholder of the REIT. Yet, it is today priced at a near 40% discount to its net asset value:

Costar

This means that by investing on a crowdfunding platform, you are making the decisions to overpay for an asset with no liquidity, no control, higher leverage, lower economies of scale, and much greater conflicts of interest.

If I offered you to buy equity in a real estate deal at 60 cents on the dollar, you would probably jump on the opportunity, but somehow, because REITs are publicly listed, they are getting no love today.

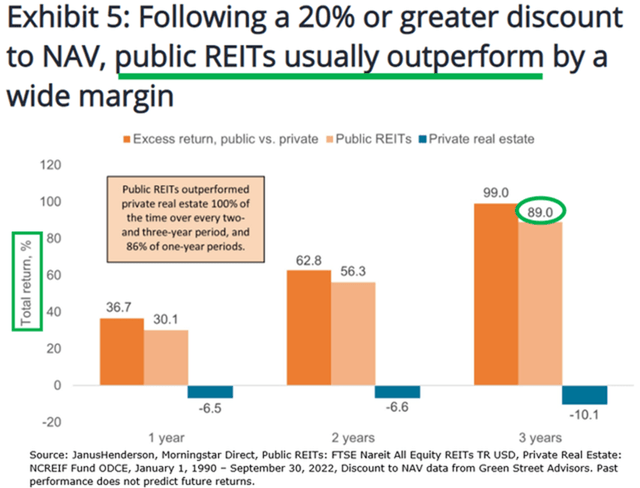

Historically, whenever REITs have been so cheap, they have strongly recovered in the following years and significantly outperformed private real estate investments:

Janus & Henderson

Will this time be different?

I don’t see why it would be, and that is why I am putting most of my real estate allocation into REITs today.

Credit: Source link

{kind=link}