kzenon

Introduction

United Rentals (NYSE:URI) is one of the compounding superstars I have followed and covered for many years. Not only has the company figured out how to effectively penetrate a highly competitive construction equipment market. It also has become a dividend growth stock, with the potential to deliver both outperforming capital gains and high dividend growth for many years to come.

Unfortunately, due to its cyclical behavior, its shares are selling off. This is what I wrote in February (emphasis added):

The company is capable of strong long-term growth. It has a healthy balance sheet, high free cash flow, and the ability to reward investors with long-term dividend growth on top of buybacks.

While the valuation is fair, I believe that economic headwinds will provide us with new buying opportunities down the road.

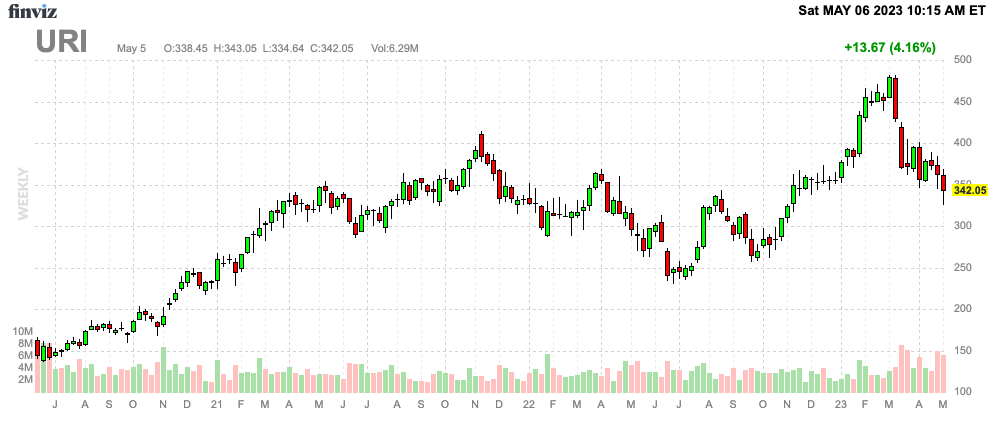

Since my February article, URI shares have lost a quarter of their value, which makes it one of the steepest sell-offs since the 2020 pandemic.

FINVIZ

Based on that context and the just-released earnings, we have a lot to discuss, as finding a suitable entry might result in tremendous long-term value for URI investors.

So, let’s get to it!

Growing The URI Way

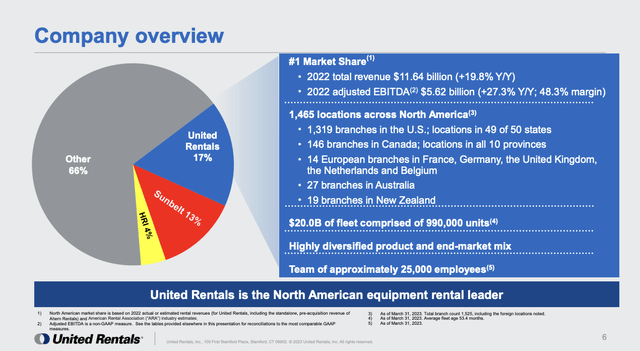

With a market cap of roughly $24 billion, Stamford, Connecticut-based United Rentals is the largest company in the Rental & Leasing Services industry. This industry is a part of the industrial sector.

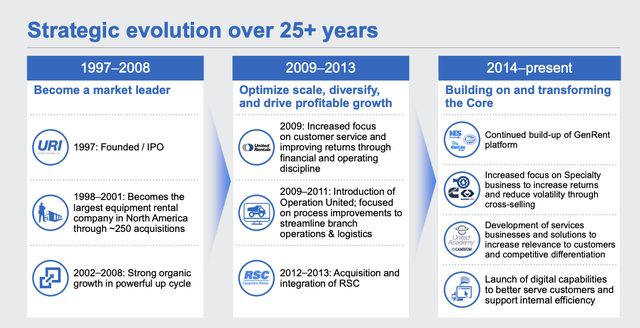

The company was incorporated in 1997 and founded by Mr. Brad Jacobs, who also founded LTL giant XPO, Inc. (XPO), which has spun off a number of leading companies in other transportation industries.

With that said, I’m not interested in buying rental companies. Entry barriers are low, and construction (and related) equipment is extremely cyclical. During economic downturns, there’s a big chance you own a company with a yard full of money-losing machinery – if you allow me to paint with a broad brush.

While this is a risk that applies to United Rentals, the company is different. It has exploited the fact that entry barriers are low and created a business model that achieves rapid growth through organic growth and acquisitions.

The company ended 2022 with a 17% market share, which included almost 1,500 locations in North America, 13 branches in Europe, 27 branches in Australia, and 19 branches in New Zealand.

United Rentals

- 48% of its customers are industrial customers, which includes power and utility companies, manufacturing, oil downstream, metals and mining, oil and gas, and everything related to these industries.

- 47% of its customers are non-residential construction customers.

- Only 5% of its customers use equipment for multi-family construction.

When I think of URI, I think of the Monopoly game. There are other stocks where this applies to as well. Basically, players that get ahead early in the game tend to win. I don’t have scientific data to back it up, but I think it’s a reasonable thesis. The moment players get ahead, they can build houses and hotels, increasing the odds of making even more money. At some point, it’s game over as companies benefit from an increasing advantage over competitors.

United Rentals is similar. The company has built a terrific framework over the past few decades. It now has a massive network of stores supported by relationships and capabilities that allow the company to offer services that smaller players cannot compete with.

United Rentals

Below are some of the benefits that I listed in February:

- Size – The company is large enough to service large customers that require substantial quantities of equipment. Smaller companies cannot compete with that.

- Variety – Its size also comes with variety, meaning it has equipment for special purposes. Again, smaller operators cannot compete with that.

- Purchasing power – When URI buys new equipment, it has a much better position when it comes to negotiating better prices. Again, it’s related to the “size” benefit.

- The National Account Program – This program establishes long-term relationships with large companies with a national or multi-regional presence. This combines all the benefits above and ties them to long-standing customers.

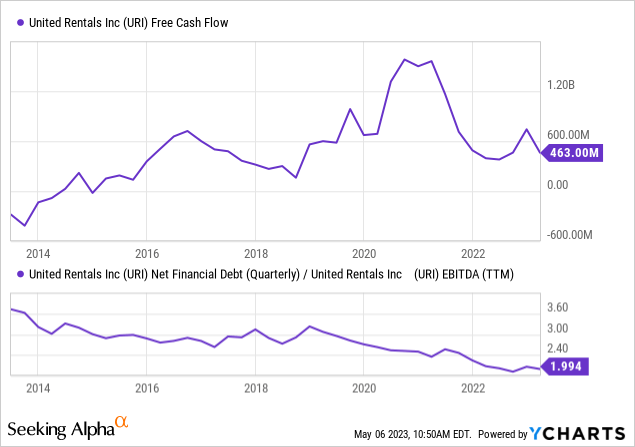

Looking at the chart below, we see that URI has become increasingly powerful. Since 2015, the company is consistently reporting positive free cash flow, which has resulted in a steep decline in the company’s net leverage ratio. The company currently enjoys a BBB- credit rating.

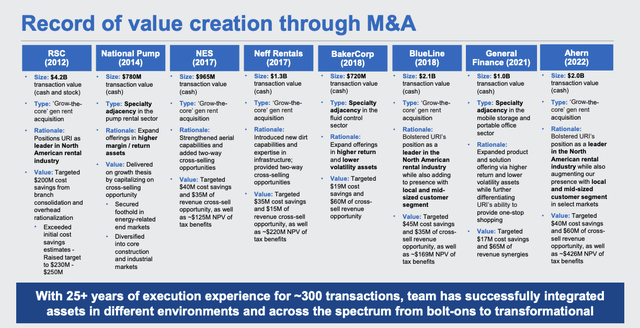

Also, note that this financial performance is based on aggressive M&A. The company has spent billions on acquisitions in the past decade, buying strong players to enhance its own operating performance. Not only that, but the company has done this without causing its balance sheet to become risky. The decline in net debt above speaks for itself.

United Rentals

On top of that, URI is now a dividend (growth) stock.

Dividends, Buybacks & Outperformance

On January 25, URI announced its first dividend. The company initiated a $1.48 per share per quarter dividend, which translates to a yield of 1.7%.

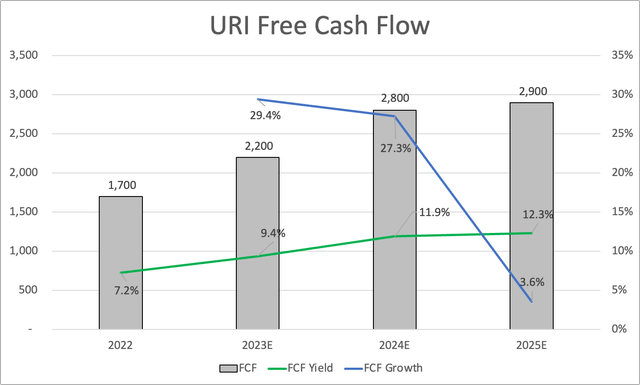

This dividend is protected by its healthy balance sheet and a load of free cash flow. Looking at estimates, the company is not only expected to maintain high free cash flow but it is also expected to end up with a double-digit free cash flow yield after 2023 – based on its current market cap.

Leo Nelissen

While the company did not say anything specific with regard to its dividend in its 1Q23 earnings call last month, it did comment on its dividend in January.

We plan to buy back $1 billion of stock this year. And we’ll also be instituting quarterly dividends for our shareholders, totaling $5.92 per share this year. These two decisions underscore our confidence in the durability of our cash generation and the strength of our balance sheet. And together, they’ll return $1.4 billion of capital to our shareholders in 2023.

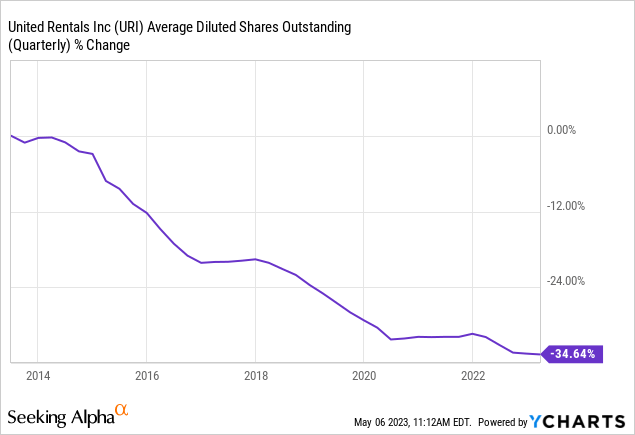

Furthermore, URI has bought back more than a third of its shares since early 2013. This is despite aggressive M&A during this period.

So, just to reiterate because it’s so impressive:

- URI operates in a highly cyclical industry.

- It has grown through organic growth and aggressive acquisitions.

- It has a very healthy balance sheet and a long-term decline in its leverage ratio.

- It has engaged in aggressive buybacks for more than a decade.

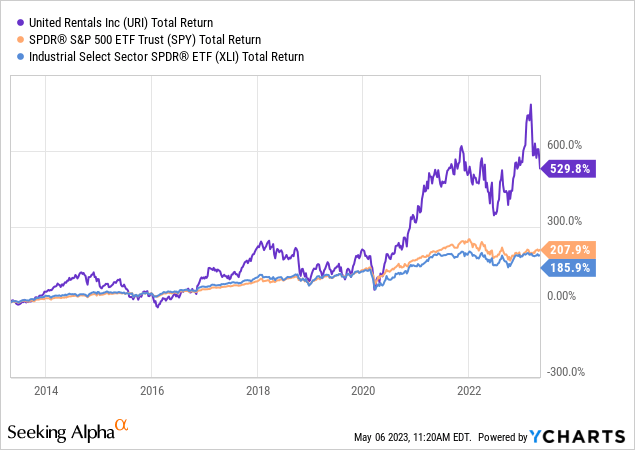

Hence, it’s no surprise that the stock has outperformed the market and industrial sector peers by a wide margin.

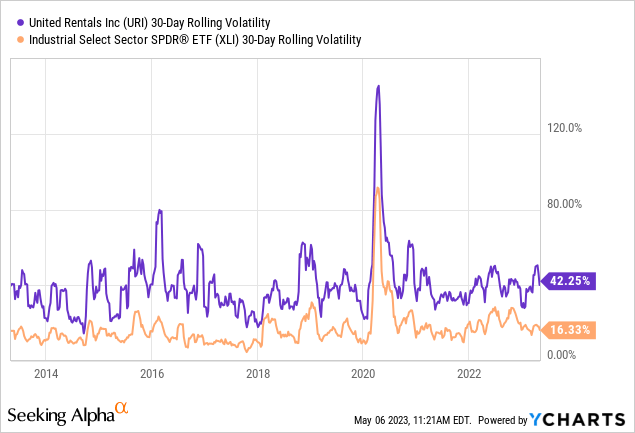

However, URI comes with high volatility. The company’s 30-day rolling volatility is consistently close to 40%, which is high for an individual stock.

High volatility is accompanied by regular and steep downturns. However, these drawdowns are not random.

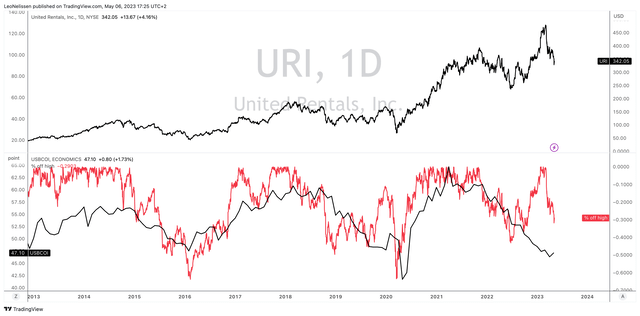

The chart below compares the URI stock price performance (% off its all-time high) to the ISM Manufacturing Index. URI perfectly follows economic expectations, which makes sense, as its business is cyclical.

TradingView (URI, ISM Index)

The fact that economic growth is in a steep downtrend is also the reason why I told readers to wait for weakness in February.

More often than not, URI shares fall 40% to 60% during manufacturing downturns. The current downturn is 30%.

This brings me to the just-released earnings.

Recession? What Management Has To Say

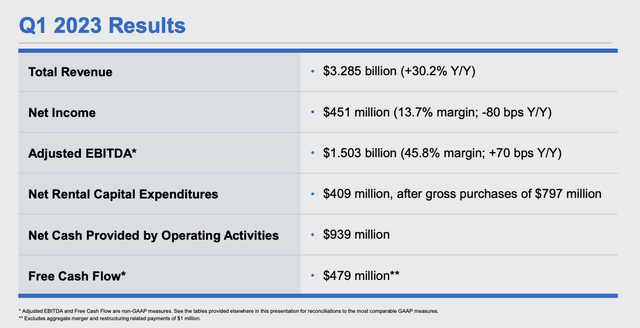

In 1Q23, URI reported a 30.6% revenue increase to $3.29 billion, beating analyst estimates by $120 million. Adjusted EPS came in at $7.95, which missed estimates by $0.04.

United Rentals

What’s interesting is that URI saw growth across all of its regions, including double-digit growth. Non-residential construction, industrial manufacturing, and power all saw positive growth. The company’s specialty business delivered great results, with rental revenue up 24% year-on-year and high growth across all lines of business, especially the mobile storage team. URI opened six new locations and is on track for around 40 cold starts this year.

URI is optimistic about its business and the positive industry indicators for the balance of 2023 and beyond. The company remains confident in its ability to capitalize on significant multi-year tailwinds for the rental equipment industry, which they believe are resilient in any economic environment. URI is well-positioned to support its customers as they undertake projects across clean energy and advanced manufacturing funded by the Inflation Reduction Act. The tailwinds hold the potential for over $2 trillion of project spending in the US over the next decade.

It remains early, but we continue to see a ramp in spending from the federal infrastructure bill across a variety of project types, including airports, bridges and road and highway. We’re also well positioned to support our customers as they undertake projects across clean energy and advanced manufacturing funded by the Inflation Reduction Act.

Within private construction, we continue to see strong investments across manufacturing, led by autos, semiconductors and energy and power. Combined reports indicate that these tailwinds hold the potential for over $2 trillion of project spend in the U.S. over the next decade.

The company is right when it mentions secular tailwinds like economic re-shoring. I have been bullish on this for a while. As a matter of fact, URI is one of my top picks in that area.

However, investors don’t care about that. Economic indicators are poor, which causes investors to be more fearful of short-term pain than long-term gains.

That’s normal for cyclical stocks and great for investors looking to buy on weakness.

Valuation

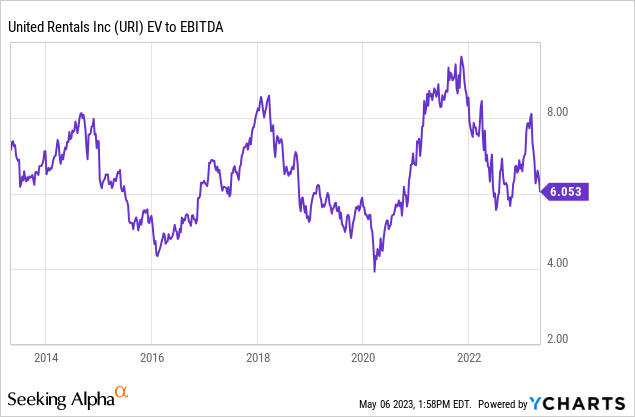

URI is trading at 6.1x LTM EBITDA. The stock trades at 5.0x 2023E EBITDA, which is the result of analysts pricing in growth this year. Add to this that the stock is trading below 9x next year’s free cash flow.

Just looking at the raw numbers, URI is a total steal right now.

However, it’s not that simple – not that anyone expected it.

- EBITDA estimates will come down if economic growth expectations do not recover soon.

- Markets tend to be irrational during both bear and bull markets. Even if EBITDA estimates were to remain unchanged, the stock could get cheaper. After all, URI has a history of dropping more than 40% during manufacturing recessions. This is something to keep in mind, even if URI is now a more mature business than it was during prior cycles.

When dealing with a fast-growing stock like URI, I believe the best thing to do is to buy gradually. While I’m still considering if I need URI (I have close to 50% industrial exposure already), I would start small and add gradually over time. If the stock continues to drop, investors can average down, which is great for a long-term investment. If the stock takes off, investors have a foot in the door.

Takeaway

In this article, we discussed United Rentals, a fascinating stock operating in the industrial sector. This company is quickly taking over the equipment rental industry thanks to aggressive M&A and a business model that allows for superior customer service.

Not only that, but the company is now at a point where it is significantly growing its free cash flow, allowing it to maintain a very healthy balance sheet, buy back shares, and grow its just-initiated dividend at a rapid pace.

Despite all of this and a good growth outlook, URI shares are selling off. The problem is that economic growth is slowing down, causing investors to dump cyclical stocks like URI.

As much as I like the valuation, I would not invest large sums in URI. I believe that gradual buying is the way to go.

My buy rating reflects its longer-term potential.

Credit: Source link

{kind=link}