code6d/iStock Unreleased via Getty Images

The best thing that happens to us is when a great company gets into temporary trouble… We want to buy them when they’re on the operating table. – Warren Buffett

Some of Warren Buffett’s best investments were made when companies with strong competitive moats got into temporary trouble. Perhaps the best-known example is American Express (AXP) which lost significant money in the “salad oil” swindle. Still, Buffett realized that American Express would probably recover, and that its franchise remained strong as he saw customers continued to use their cards.

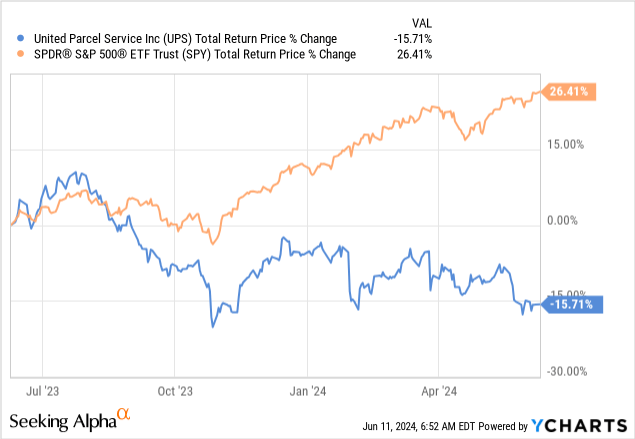

In some ways UPS (NYSE:UPS) is also on “the operating table” right now, as the company has been impacted by lower volumes and higher costs. In particular, it is having to absorb significant wage inflation as it negotiated a contract with the Teamsters union that resulted in significant wage increases, particularly in the first year which they will anniversary on August 1st, 2024. To compensate for the cost increase, the company is implementing measures to significantly improve productivity and efficiency. However, these measures will take time to implement and for the results to show. This has generated uncertainty that has driven shares considerably lower, underperforming the S&P index (SPY) over the past twelve months by a significant margin.

Current Headwinds

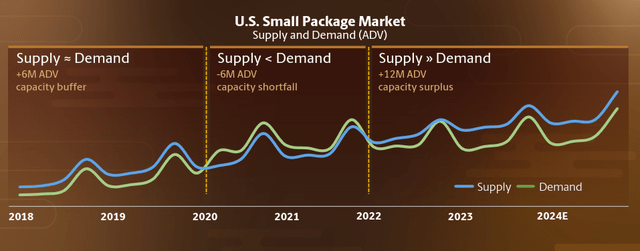

In addition to the cost increases resulting from the Teamsters negotiation, UPS is also facing excess market capacity. This happened because logistics companies rapidly expanded after the post Covid e-commerce boom. While e-commerce has retained most of the share it gained, e-commerce companies including the likes of Amazon (AMZN) extrapolated too far the growth they were seeing. Still, logistics companies have now adjusted their capital expenditures accordingly, and the excess capacity is expected to return to more normalized levels soon.

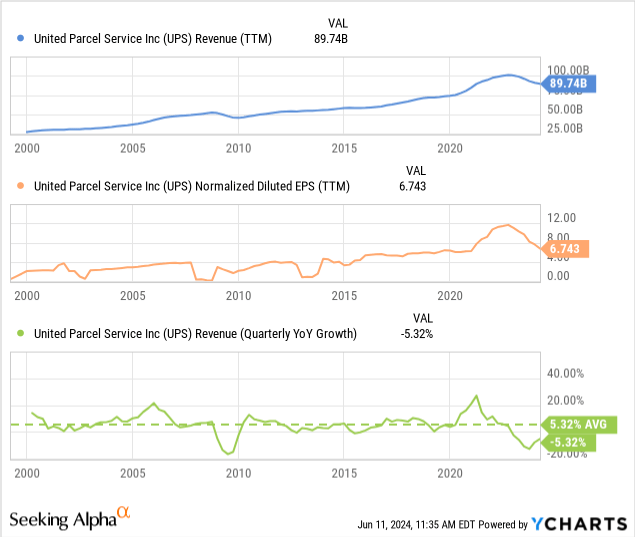

What all this results in is lower earnings in the short term. For the first quarter, UPS reported revenue of $21.7 billion, which was down 5.3% year-over-year. Diluted earnings per share of $1.43 reflected a decline of 35% compared to the first quarter of 2023.

Average daily volume was down 3.2% year-over-year, and B2B average daily volume was down 5.5%, mostly driven by declines in the retail and manufacturing sectors. International total average daily volume was down even more significantly, with a 5.8% year-over-year decline.

UPS Investor Presentation

Secular Tailwinds

While current challenges should be taken seriously, it is also important to look at the bigger picture. It is clear that e-commerce continues to take retail market share, and this should benefit companies like UPS. While logistics companies overshot in their capacity additions, it is a matter of time for this excess capacity to be absorbed.

During its last earnings call the company reported that its productivity was increasing, and that it is expanding its addressable market share. One example is its expansion in big and bulky deliveries through Roadie, which offers delivery of items such as grills and furniture. The company estimates the TAM for this type of delivery at ~$60 billion. Another promising growth segment is healthcare, where the company wants to become the number one player in healthcare logistics worldwide. In the first quarter the company generated about $2.6 billion from its healthcare operations, and it has a goal to reach $20 billion in revenue annually by 2026.

Financials

The combination of higher costs and lower revenue has had a significant impact on profitability, with normalized diluted earnings per share falling almost by half. On the positive side, we can already see the revenue growth rate starting to rebound, and management sounding more positive about the second half of the year.

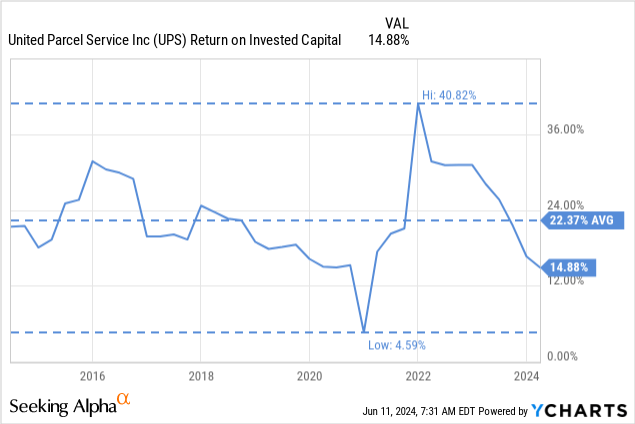

Strong Competitive Moat

Even during these trying times, the company continues to deliver attractive returns on invested capital [ROIC]. We believe this elevated ROIC reflects the company’s strong competitive moat, which it derives from its scale advantages and difficult-to-replicate logistics network. The massive logistics networks the company has built gives it a cost advantage in many cases, while allowing the company to also offer a superior customer experience. Sometimes with reduced delivery times, or increased convenience thanks to its massive UPS Stores footprint.

U.S. Postal Service Contract

Another example of UPS’s strong competitive moat can be found with the U.S. Postal Service contract it won from its competitor FedEx (FDX). Analysts believe this was a close to zero margin business for FedEx, but that UPS assured investors that it will be a profitable contract for the company. This will make UPS the primary air cargo provider for the United States Postal Service, and CEO Carol Tome commented that it should be margin accretive.

Well, thanks very much for your question, Amit. And we’re delighted to have won the air cargo business from USPS our team put together an innovative solution using our integrated network. And as in contrast to traditional hub-and-spoke models, we don’t have to run all of the air volume through our main air hub at Westport. Of course, we will use Worldport, but we will also use our regional gateways. That allows for splits to occur outside of the network, so they’ll be built in origin and then we will bypass the main hub and go point to point. This is an integrated solution that’s very different than I think the former provider offered.

We also will use all of the assets of our integrated network, and that will allow us to actually optimize block hours.

Now in terms of the investments that we need to make to services volume, we have plenty of space on our existing aircraft. So we won’t be purchasing any aircraft. We will be hiring some pilots but less than 200 pilots, and we factored all of that into the cost model that we built. So this will be margin accretive. It will be EPS great at beginning in year one and through the life of the contract.

Returns Business

Another business that has proven challenging for many logistics companies is the “returns business”. However UPS sees an attractive opportunity to leverage its massive store footprint and network to expand its addressable market. It has even launched a specific initiative that it calls Happy Returns, which offers no-box and no-label returns at more than 5,200 UPS store locations.

The company explained during the earnings call why this is an attractive business, including the fact that these are typically business-to-business (B2B) transactions that drive pickup and delivery density. It also helps create customer loyalty and repeat business, as Carol Tome explained:

So we like to return business a lot. You’re right, the consumer typically walks into a UPS store to start the return and we consolidate the returns at the UBS store, and they returned to the shipper. And that would be a B2B return.

So if you think about — I’ll use our largest customer for an example, we have returns through our UPS stores with our largest customer. We take in thousands of returns for that customer and package it into one consolidated return that goes back to them. So that’s a good business for us.

And with Happy Returns, now we were able to offer the same service, which is no box in the label. Same idea, consumer walks in, they make the return, we consolidate it and return it back that’s how we think about it being a B2B business, and the margins are very attractive to us. It’s density. That’s one reason why the margins are so good because you get that.

Peers

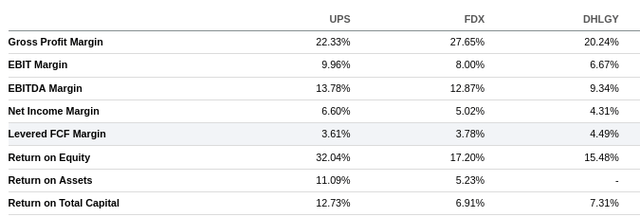

There are very few companies that can afford to spend the enormous resources needed to build a logistics network to rival UPS’s. In the U.S., the only pure-play companies are UPS and FedEx, with DHL dominating in Europe (OTCPK:DHLGY).

A good example of how difficult it is to compete with an entrenched logistics network is the fact that despite its domain expertise and significant resources, DHL Express decided in 2009 to exit the U.S. market. There is some fear that Amazon (AMZN) will eventually try to compete more directly with UPS and FedEx. While this is a real risk, so far it seems that Amazon is mostly focused on delivering its own packages. In any case, based on the EBITDA and net income margins, we believe UPS has a stronger competitive moat than FedEx and DHL Express.

Seeking Alpha

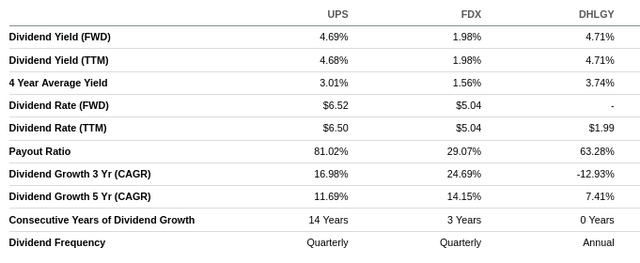

UPS has a long history of increasing its dividend, and currently has a very high dividend yield of ~4.7%. While the reduced earnings have resulted in an elevated payout ratio, the company believes it will be able to maintain the dividend. CEO Carol Tome reassured analysts and investors during the last earnings call saying they have no intention of cutting the dividend, and that they expect to restore earnings so that the payout ratio normalizes again:

We have a disciplined approach when it comes to capital allocation. The first use of our cash, as you know, is to invest back into our business and the second is to pay our dividend. We have a targeted dividend payout ratio of 50%. We are higher than that. It’s our intent to earn back into a 50% payout ratio over time. We have no intent to cut the dividend to make that math work. We’re going to earn back into it and the dividend is an important part of the value proposition. So we just raised the dividend and we look to, of course, subject to board approval, we look to raise the dividend every year.

Seeking Alpha

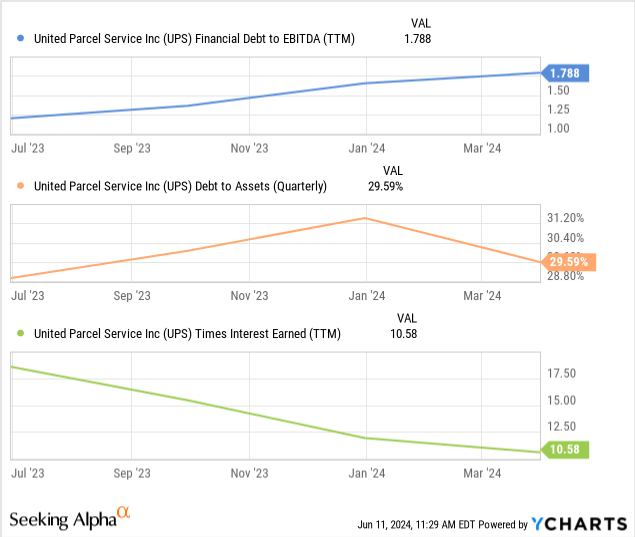

Balance Sheet

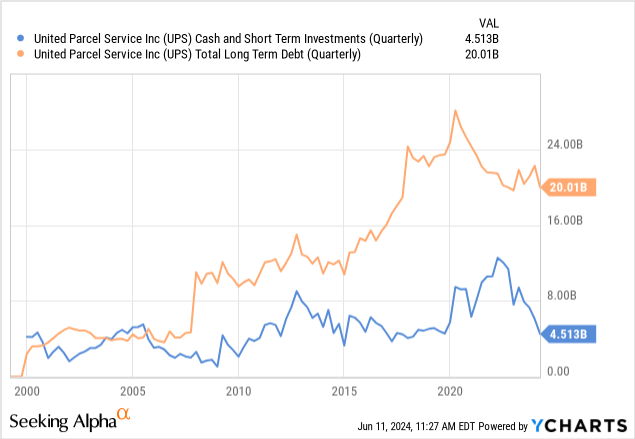

UPS has a strong balance sheet with significant liquidity, and strong investment grade credit ratings. Still, the amount of debt it carries is not insignificant, and is considerably higher than it was ten years ago.

Its financial debt to EBITDA ratio has been increasing, but remains at a relatively healthy level below 2x. Similarly, its debt to assets is below 30%, and its interest coverage is more than 10x, even if this indicator has also experienced some deterioration.

Outlook

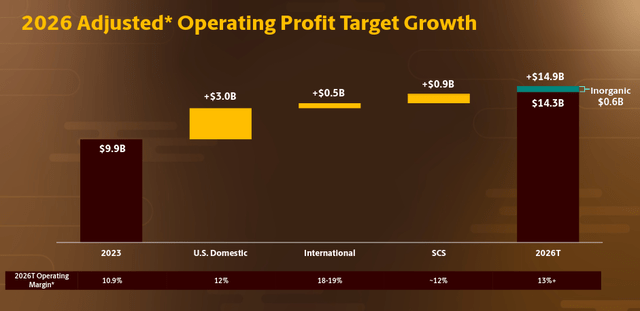

UPS is guiding for revenue in fiscal year 2024 to be in the range of $92 billion to $94.5 billion, and its consolidated operating margin between 10% and 10.6%.

Importantly, the company reaffirmed the targets it had shared during its investor day that call for revenue to be between $108 billion and $114 billion and its operating margin to exceed 13% by 2026. One of the keys to achieve these targets will be for the company to grow its U.S. revenue per piece at a compounded annual growth rate (CAGR) of at least 2.5% between 2024 and 2026, while the cost per piece should grow with a CAGR of 1% or less during this period.

UPS Investor Presentation

Valuation

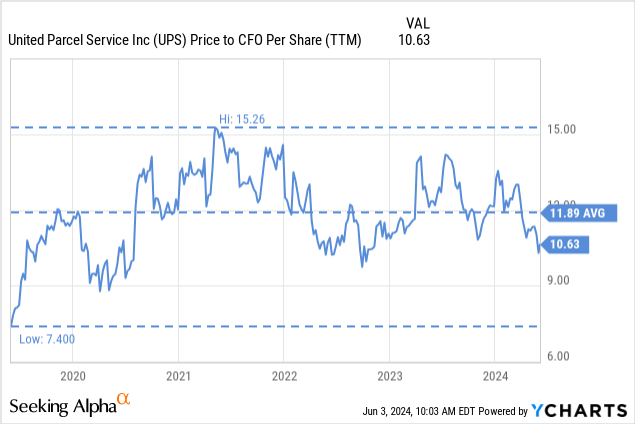

Compared to its own valuation history, UPS is trading below its ten-year average price to cash flow from operations. Most other valuation metrics also point to an undemanding valuation. This is in large part the result of the disappointing earnings the company has delivered in the past couple of quarters.

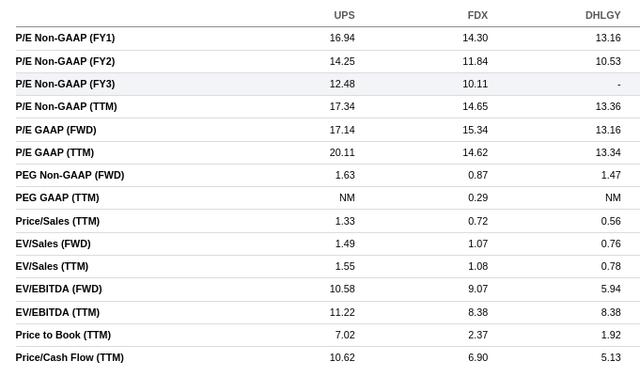

However, we do believe management is right that the excess capacity will soon be absorbed and growth will resume. Analysts seem to also believe earnings will recover, as their forward estimates call for earnings growth in the coming years. In fact the forward FY26 P/E is less than 12.5x, while the trailing twelve months GAAP Price/Earnings ratio is about 20x. UPS competitors look even cheaper, but we believe UPS does deserve a premium given the strength and scale of its logistics network.

Seeking Alpha

Risks

An investment in UPS is not without some important risks. As previously mentioned, Amazon is building its own logistics network, and could one day try to compete more directly with UPS and FedEx. We believe many retailers would be hesitant to let a competitor handle their packages, which somewhat mitigates this risk. There is also risk that the excess capacity might take longer than expected to be absorbed, which could be the case, especially if the U.S. economy goes into a recession.

There is also execution risk that the automation and consolidation strategies the company is using to counter wage inflation might not provide the expected benefits. Finally, the company is committing very significant sums to improve and modernize its network, around $18 billion over the coming three years, and it remains to be seen if these investments pay off.

Conclusion

In some ways we believe UPS is currently on the “operating table”, and investors are understandably nervous. However, we believe this has created a good buying opportunity for investors that believe that the company will be able to counter wage inflation through automation, consolidation, and modernization of its network.

If the company delivers on its promise of creating capacity through higher productivity, reducing the cost and labor intensity per package, and improving customer service, then there is a good chance that profit margin targets can be reached. In other words, we believe that if management delivers on its 2026 targets, investors buying at current prices should be handsomely rewarded.

Credit: Source link

{kind=link}