Gabriel Trujillo/iStock via Getty Images

Executive Summary

Spotify (NYSE:SPOT) is continuing to grow its premium subscriber base even after a price increase was implemented, leading to strong earnings growth. Spotify is also continuing to invest in its own content portfolio, with the hope that an increasing share of the revenue pool will be allocated to its podcasts and audiobooks. Growing revenue share from high-margin content investments would help Spotify to continue increasing margins, even if record labels adopt a more aggressive position in negotiations.

The market seems to anticipate a considerable opportunity for Spotify to increase its owned content portfolio and continue growing its profit margins over the long term. However, the business of podcasts has proven to be more challenging than initially anticipated, and it remains to be seen if other content categories such as audiobooks can be more successful. So far, Spotify has not proven its ability to diversify away from music revenues and therefore its earnings growth can be capped by higher rates demanded by the major record labels.

Strong earnings growth due to price increases and improved podcast monetisation

During the second quarter of 2024, Spotify managed to generate EUR 266 million in operating profits, compared to losses over the same period last year. This was made possible by a 21% premium revenue growth on the back of growing subscriber numbers and higher pricing, as well as improving gross profit margin.

Gross profit has increased by 45% from a year prior. The most significant drivers of this uplift were the improvement in music and podcast profitability. Music’s gross margin improved as the higher margin premium revenue growth exceeded ad-supported revenue growth due to subscription price increases.

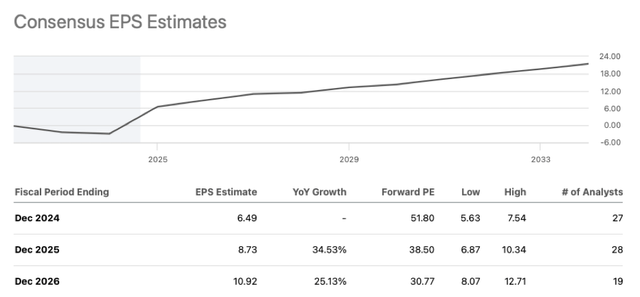

Podcast profitability is also improving as the company is shifting the focus of owned content investments from subscriber acquisition to monetisation. Spotify is now expected to be able to generate ~$11 of per-share earnings in three years, as strong growth continues.

Seeking Alpha

The market seems to expect the business to continue growing subscriber revenues in the mid-teens, while also increasing its net profit margin to about 10% by the end of 2026. We see these expectations as rather rosy. For one, they ignore the bargaining power that the record labels have, as Spotify might need to start paying a higher revenue share once its profitability improves.

However, the business is trading at a rather rich valuation of ~31X three-year forward earnings. We believe there is considerable uncertainty as to their ability to maintain higher profit margins, as record labels might push for higher licensing fees in upcoming negotiations.

Friends or foes? Spotify and the record labels

Spotify and the major record companies such as Universal Music (OTCPK:UMGNF) or Warner Music (WMG) have a symbiotic relationship. As Spotify subscriber numbers grow and the revenue pool increases, labels benefit as they are allocated a pre-determined share of these revenues.

It is in the interest of the labels to see Spotify or Apple Music (AAPL) and the like grow their subscriber numbers. To grow subscribers, the streamers need to invest in sales and marketing as well as technology. To be able to make these investments, the streamers need to generate sufficient gross profits to cover the expenses.

Record labels do want Spotify to generate a certain level of Gross Margin, but once the platform starts doing “too well” they might be tempted to tighten the leash. For most of its history, Spotify was barely breaking even, and therefore the record labels had to be accommodative to make sure that the business did not collapse. But now that profits are starting to roll in, the relationship might change.

Owned content is the key to protecting profit margins

Spotify is aware of this risk and is therefore actively trying to develop an owned audio content portfolio. Exclusive podcasts and audiobooks are the keys to that strategy. Even if record labels eventually demand a higher share of the music streaming revenues, the music will likely represent a lower share of overall playback time on the platform.

The music profit margin might contract going forward; however, the owned content revenue share will increase, mitigating the overall negative effect of higher music licencing fees.

Sirius XM (SIRI), for example, generates 50% gross margins as a significant portion of their listening time stems from owned content such as The Howard Stern Show or exclusive sports broadcasting rights. Joe Rogan, for example, is Spotify’s version of Howard Stern. The company has recently renewed its deal with Rogan for a reported $250 million, hoping to monetise this content across all platforms. Owned content should generate higher margins, as Spotify would have more bargaining power against a fragmented roster of individual rights owners.

Podcasting has not been as profitable as initially anticipated

It has not worked as anticipated, though. Podcasting is a rapidly growing market and has attracted interest from both traditional media and tech companies. A lot of money was spent in the industry to acquire attractive content and develop a leading position in this market with growth potential.

Overall, Spotify spent more than $1 billion to build its owned podcast portfolio, with big-name hosts such as the Obamas, Joe Rogan, Kim Kardashian and Prince Harry. The company, however, has been losing money on most of these high-priced content deals.

Spotify is now moving its owned content strategy from subscriber acquisition to ad monetisation. Exclusive content encourages listeners to sign up, however a wider distribution increases ad revenue potential as content reach is broadened. The Joe Rogan Experience will not be exclusive to Spotify; however, the company will be entitled to revenues from all the platforms where it is distributed. Spotify will monetise the show across all podcast networks as well as YouTube.

Essentially, Spotify’s podcasting business is evolving from a Sirius-like subscription talk show model to a free-to-air ad-supported model. The ad-supported business models tend to be less profitable but require less upfront investing. It will help podcasting to break even but caps the future profit potential.

Spotify is said to have 100 million podcast listeners on its platform and is on track to make the podcast business profitable in 2024.

Is podcasting the first step towards an audio empire?

CEO Daniel Ek has the vision for Spotify to become the largest audio company, spanning audiobooks, education, sports, and news. Podcasts are only the first step toward this goal.

Spotify has the ambition to reach $100 billion in revenue in 10 years, up from $13 billion last year. If the business could indeed achieve this ambition, and diversify away from music revenues, the profit margins of the business would grow, and earnings would soar higher.

However, we do not believe it is sensible to talk about an audio media empire when the company is only starting to break even with podcasts. It has also chosen to move to an ad-supported revenue model for podcasts, which is a lower gross margin endeavour.

As it stands today, Spotify is still generating an overwhelming majority of its profits from streaming music, and it is unlikely to evolve in the near term. Spotify would not be able to generate profits without content from the leading record labels.

Some new initiatives, like audiobooks, have proven to be successful in the U.S. and hold some future potential, but it is too early to tell with any certainty.

The Bottom Line

Spotify has finally been able to become profitable after years of losses. This profit growth propelled the stock price 4X over the last year and a half. We believe that the market is overly optimistic about the future prospects of the business and is ignoring the potential of the major record labels to renegotiate higher revenue share.

Spotify has been investing heavily to build its own content portfolio to be less reliant on external content suppliers, much like Netflix (NFLX), however, this strategy has not yielded tangible results as of yet. We therefore believe that Spotify might struggle to hold on to the higher profit margins and might fail to live up to EPS projections.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Credit: Source link

{kind=link}