Jim Still-Pepper/iStock Unreleased via Getty Images

With the academic school year set to begin in a few days, I thought it would be a good time to check up on Scholastic Corporation (NASDAQ:SCHL), the world’s largest publisher and distributor of children’s books and media.

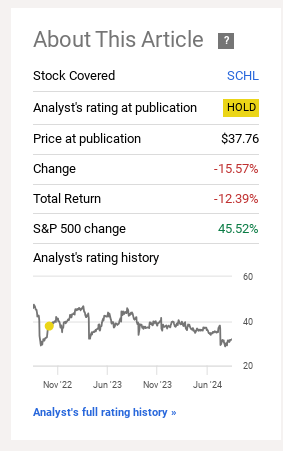

I last wrote about Scholastic in late 2022, when I deemed the company fairly valued with downside risks to revenues. So far, my caution appears warranted, as Scholastic’s stock price has declined by 12%, dramatically underperforming the 45%+ return on the S&P 500 Index (Figure 1).

Figure 1 – SCHL has underperformed S&P 500 (Seeking Alpha)

Scholastic has seen declining revenues and margins as consumers and educators balk at the high price tags of the company’s products. To spur growth, Scholastic recently paid $250 million to buy 100% economic interest of a digital media and publishing business. While management should be commended for proactively trying to improve its growth trajectory, it is simply too soon to pass verdict on the 9 Story investment. With only $112 million in LTM revenues, 9 Story may be too small to move the needle for Scholastic.

For now, I recommend investors stay on the sidelines and await more signs of stabilization in SCHL’s core children’s book business.

Brief Company Overview

Scholastic Corporation is a leading publisher and distributor of children’s books and media. In North America, Scholastic is best known for operating school-based book clubs and book fairs where school children can directly purchase books from Scholastic. The company also sells books to schools and libraries as well as through physical and online stores.

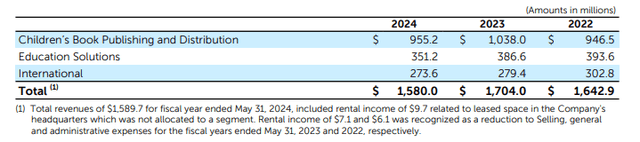

On a segmented basis, Scholastic derives approximately 60% of its revenues from publishing and distributing children’s books in the U.S., 22% from selling directly to American schools, and the rest from similar business models in other countries like Canada, the U.K., and Australia (Figure 2).

Figure 2 – SCHL revenues by segment (SCHL F2024 10K report)

The Bad…

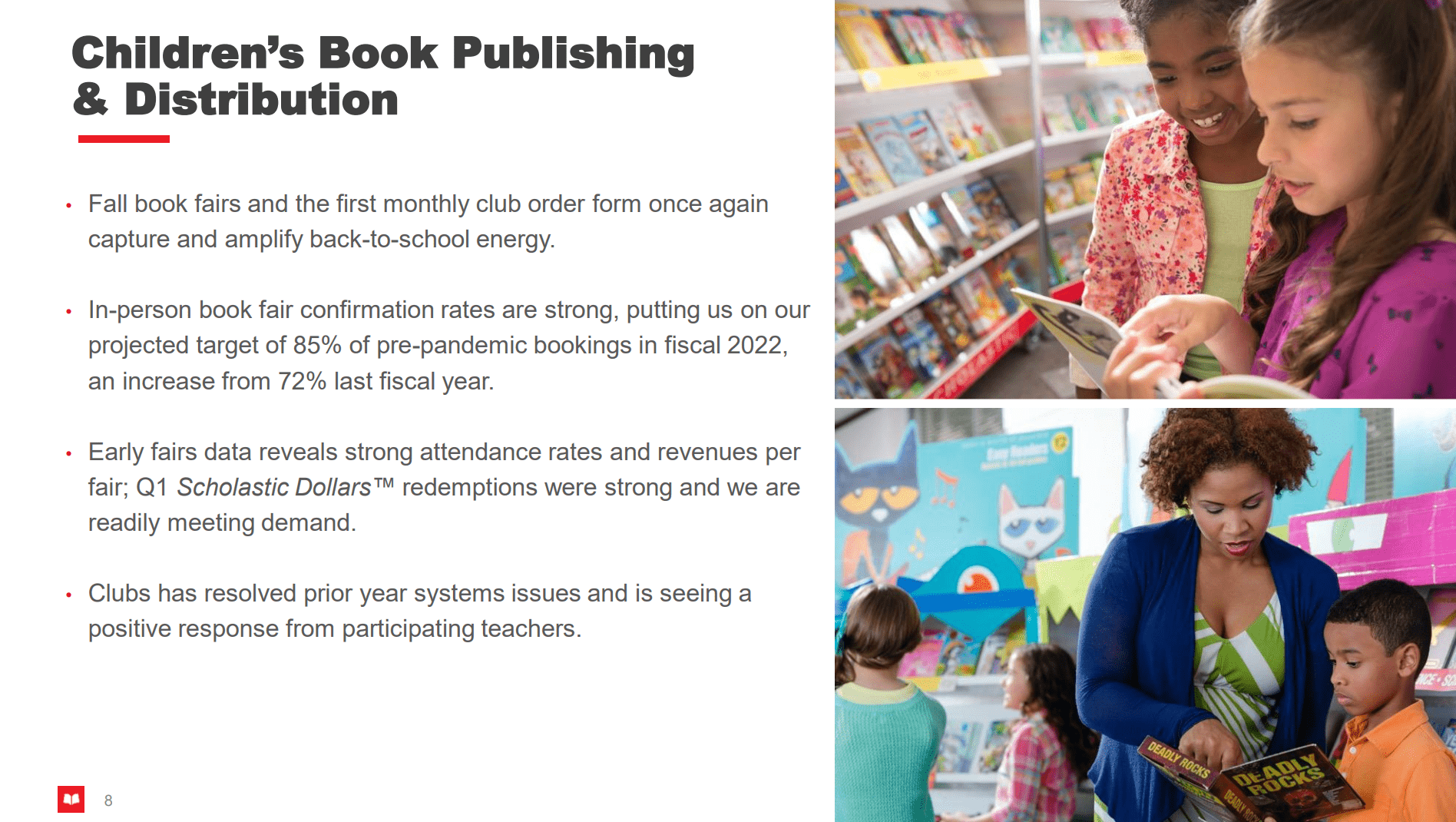

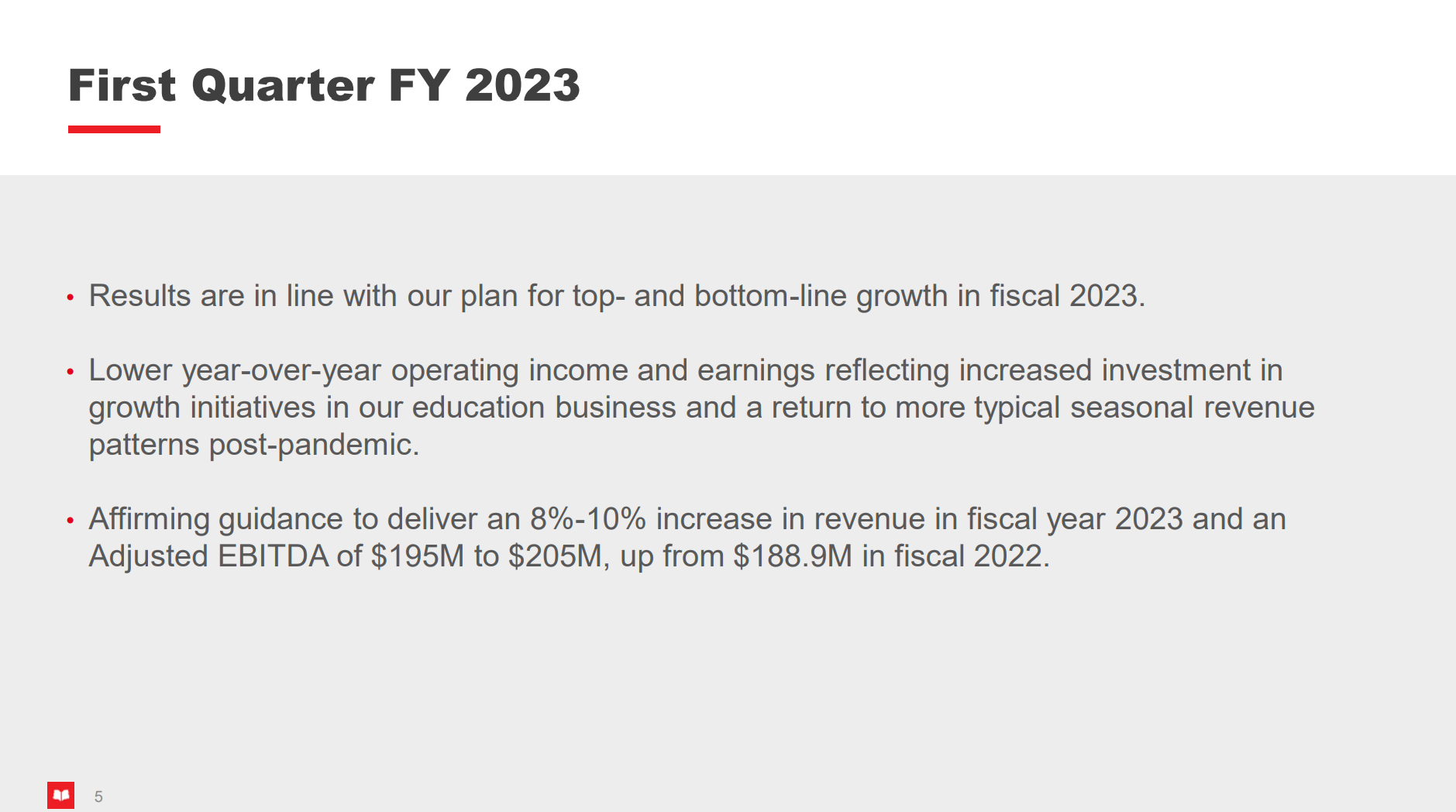

Going back to my 2022 article, one of my main worries was Scholastic’s revenue guidance. Recall, at the time, Scholastic was quite optimistic about the 2022 academic year (which is covered in SCHL’s fiscal 2023), as in-person book fairs have only recovered to 85% of pre-COVID-19 pandemic levels (Figure 3).

Figure 3 – SCHL Q1/F23 Children’s Book Publishing & Distribution Commentary ((SCHL Q1/F23 Investor Presentation)

Management believed revenues could return to pre-pandemic levels and beyond, and guided to FY2023 revenues and adj. EBITDA increasing 9% and 6% respectively compared to FY2022 (Figure 4).

Figure 4 – SCHL F2023 guidance (SCHL Q1/F23 Investor Presentation)

However, as I noted in my article, with the price of children’s books increasing by 60% or more and a cost-of-living crisis across the United States, Scholastic was at risk of consumers cutting back on their discretionary purchases of children’s books.

In my personal experience, instead of purchasing multiple $8-10 books at my child’s school book fairs, I opted to acquire a family subscription to Epic!, a digital reading platform, giving my children access to thousands of books appropriate for their reading levels (Figure 5).

Figure 5 – Digital platforms offer subscription-based reading (getepic.com)

For my family, this made financial sense since my children were avid readers and rarely re-read the same book twice, so the cost-per-book was less than $1.

Unfortunately for Scholastic, my worries were proved correct as the trend towards digitization and the dramatic price increase in children’s books have negatively affected their revenues, leading to Scholastic missing on its revenues compared to initial guidance.

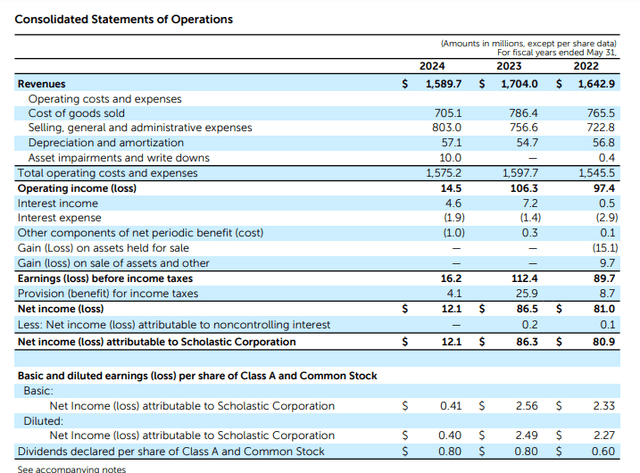

Instead of revenues increasing 8-10% in fiscal 2023, revenues only rose 3.7% in 2023 to $1.70 billion. To make matters worse, the negative trend appears to have accelerated in fiscal 2024, as the cost-of-living crisis worsened and consumers looked for ways to cut back spending. Fiscal 2024 revenues declined by 6.7% YoY to $1.59 billion, and were even lower than in fiscal 2022 (Figure 6).

Figure 6 – SCHL financial summary (SCHL F2024 10K report)

…And The Ugly

Although revenues declined in fiscal 2024 compared to 2022, operating costs did not. SG&A in fiscal 2024 was 11.0% higher than in 2022, as salaries and wages kept going higher YoY due to inflation.

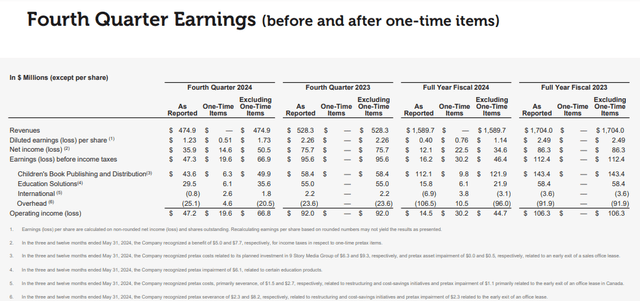

This led to a collapse in Scholastic’s operating income to just $14.5 million in F2024 compared to $97.4 million in F2022 and dil. EPS of $0.40 vs. $2.27. However, after excluding ‘one-time items’, SCHL’s adj. dil. EPS was not as bad, coming in at $1.14 (Figure 7).

Figure 7 – SCHL adj. financial earnings (SCHL Q4/F24 Investor Presentation)

Pivot To Digital Media?

To management’s credit, they appear to recognize the change in the market landscape and recently (subsequent to the 2024 fiscal year-end) made a bold $250 million bet to acquire 100% economic interest in 9 Story Media Group (but only 25% voting control).

9 Story is an award-winning creator, publisher, and distributor of children’s media with an in-house animation studio creating children’s shows like “Doc McStuffins,” “Daniel Tiger’s Neighborhood,” “Octonauts,” and “Wild Kratts”.

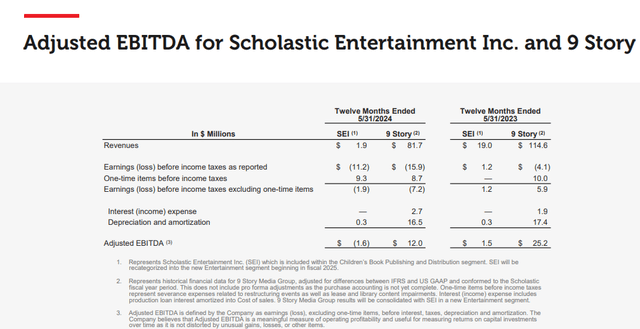

The price Scholastic paid appears fair, with 9 Story generating $25.2 million in LTM adj. EBITDA, or ~10x EV/EBITDA (Figure 8).

Figure 8 – Abbreviated 9 Story financials (SCHL Q4/F24 Investor Presentation)

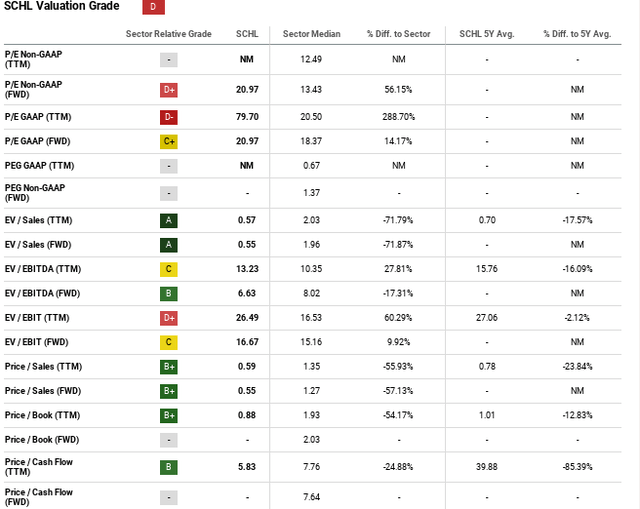

This price-tag is similar to the sector median at 10.3x, but is a premium to SCHL’s Fwd EV/EBITDA multiple at 6.6x (Figure 9).

Figure 9 – SCHL valuation (Seeking Alpha)

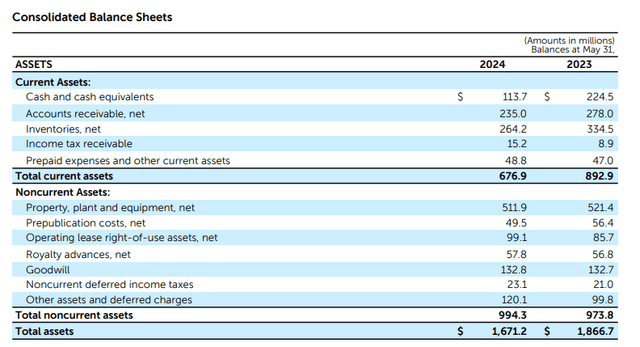

Scholastic is funding this transaction from available cash and its revolving credit facility. With only $114 million in cash as of May 31, 2024, this suggests Scholastic may have to take on ~$150 million in revolving debt to complete the 9 Story transaction (Figure 10).

Figure 10 – SCHL only has $114 million in cash (SCHL F2024 10K report)

Disappointing 2025 Guidance

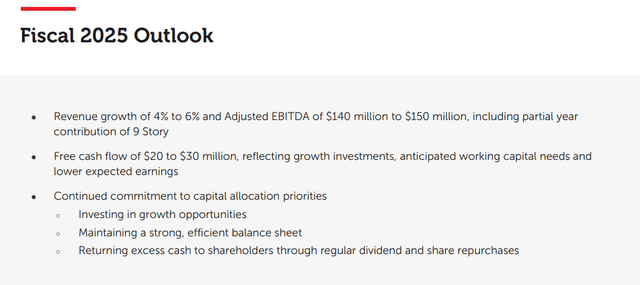

Even accounting for the addition of 9 Story, Scholastic’s initial F2025 guidance looks disappointing. The company is looking for 4-6% revenue growth and adj. EBITDA of $140-150 million. Free cash flow is expected to decline to $20-30 million, reflecting growth investments, increases in working capital, and lower ‘expected’ earnings (Figure 11).

Figure 11 – SCHL F2025 outlook (SCHL Q4/F24 Investor Presentation)

A 4-6% revenue growth rate suggests management is looking for $1.65 -1.69 billion in revenues or a $64 to 95 million increase in revenues. However, from Figure 8 above, we know that 9 Story generated $115 million in revenues in the last twelve months. Assuming 9 Story revenue stays flat, this implies management expects a further decline in ‘core’ revenues.

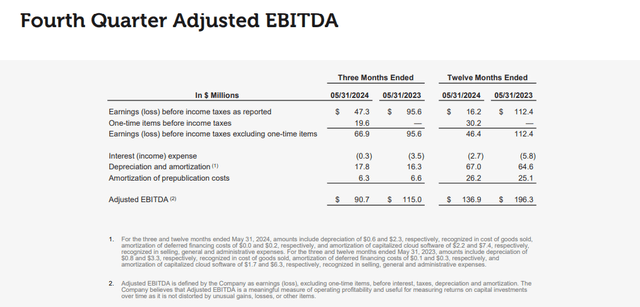

Furthermore, SCHL’s ‘core’ business generated $137 million in adj. EBITDA in F2024, and 9 Story generated $25 million in the last twelve months (Figure 12). Compared to the midpoint of management’s $140-150 million adj. EBITDA guidance, management is implying the ‘core’ business will see adj. EBITDA further shrink in the coming year.

Figure 12 – SCHL Q4/F24 EBITDA (SCHL Q4/F24 Investor Presentation)

Risks To Scholastic

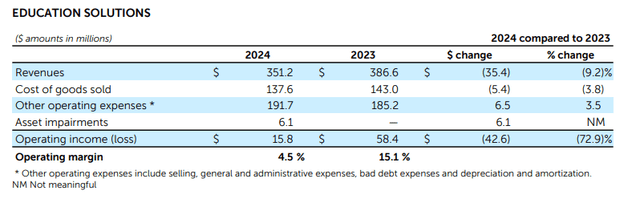

In my opinion, there is a high risk that Scholastic’s ‘core’ business will deteriorate faster than management expects. In particular, I am concerned about the collapse in Scholastic’s Education Solutions segment, where revenues declined 9.2% YoY and operating income shrank 73% (Figure 13).

Figure 13 – SCHL Education Solutions segmented performance (SCHL F2024 10K report)

The Education Solutions segment sells books and teaching resources directly to classrooms and libraries. According to commentary in the 10-K, Scholastic suffered declines in segment revenues as there was declining spending on “supplemental curriculum materials, especially those not explicitly aligned with science-based approaches to literacy,” as well as increased competition.

In my opinion, Scholastic’s troubles could be related to tightening school budgets, as Federal pandemic-related aid came to an end. Looking forward, $122 billion in Federal aid is set to expire this coming September, which could further dampen demand for supplemental teaching materials from suppliers like Scholastic.

On the upside, if the 9 Story pans out, that could change the trajectory of Scholastic’s outlook. However, children’s animation is a fickle business, and it is hard to create hit shows. In my opinion, 9 Story’s current IP is middling/mediocre (I asked my children whether they watched any of 9 Story’s shows and they said the shows were for babies), and may not generate enough growth to excite investors.

Conclusion

With Scholastic’s core children’s books business mired in a slump and the company betting big on a pivot to digital media, I believe execution risks have grown for the company. For now, I recommend taking a cautious stance until we see signs of stabilization in SCHL’s core business or more details on 9 Story’s growth trajectory. I am maintaining my hold recommendation.

Credit: Source link

{kind=link}