FilippoBacci

The Swiss pharmaceutical stock Roche Holding AG (OTCQX:RHHBY) might have seen underwhelming performance year-to-date [YTD], but a turnaround is becoming visible with a 13% price rise in the past month. While the stock had already started inching up after touching five-year lows in early May, it got another boost following positive results for its weight management treatment.

Here, I look at why this latest result could be a big deal for Roche and what’s next for the stock in the near future.

Price Chart (Source: Seeking Alpha)

Notable impact from treatment

The significance of obesity treatments can’t be emphasized enough. As Roche points out, by 2035, around half the world’s population would be impacted by either obesity or from being overweight. This in turn significantly increases the risk of lifestyle diseases like Type 2 diabetes, with Public Health England noting, “90% of adults with type 2 diabetes are overweight or obese.”

To this extent, the results from the Phase I clinical trial of the company’s C-388 injection administered over 24 weeks are highly encouraging, resulting, on average, in a ~19% weight loss. Further, 45% of the patients receiving the injection reported over 20% weight loss in eight months.

Why the new treatment can be big for Roche

This is excellent news for Roche for multiple reasons:

- Peers see big growth in weight and diabetes management: If the progress of companies like the Danish Novo Nordisk (NVO) and Eli Lilly (LLY) that focus on weight management and diabetes treatments is any indication, Roche could significantly stand to gain if all goes well with its own treatment. For example, almost 93% of Novo Nordisk’s revenues were generated from the segment in 2023, which grew by a robust 38% too. The segment had a significant share of almost 58% in revenues in 2023 for Eli Lilly too, along with a 36% revenue growth.

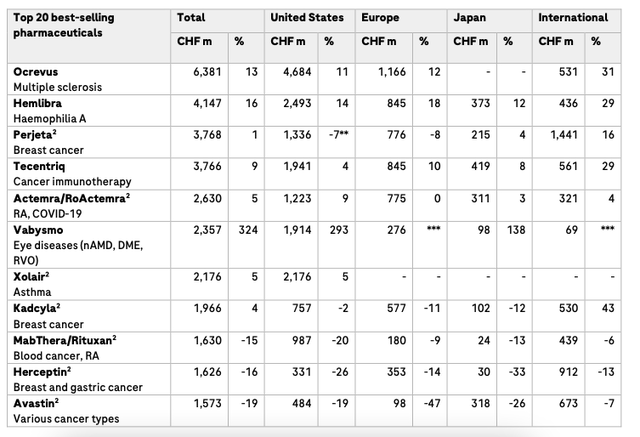

- Roche’s minimal presence in diabetes care: By comparison, Roche’s three biggest treatments, accounting for 24% of the revenues in 2023, are in diverse areas like multiple sclerosis (Ocrevus), hemophilia (Hemlibra) and breast cancer (Perjeta). Its presence in the weight management and diabetes segment is only through its diagnostics division, with the diabetes care segment contributing only 2.3% to total revenues in 2023.

Revenues, 2023 (Source: Roche Holdings)

- Potential to improve sales growth: The potential of the segment along with the encouraging results from Roche’s treatment are particularly encouraging considering the company’s sagging sales. In 2023, its sales contracted by 7% at market exchange rates due to a strong Swiss franc. Most notably, its home currency’s ~8% appreciation against the USD was a downer, considering that the US is its biggest market, bringing half the company’s pharmaceuticals’ revenues in 2023. It did better in constant currency terms, with a 1% growth and an even better 8% increase ex-Covid-19 sales. However, even this isn’t comparable with the 36% increase in total revenues for Novo Nordisk in 2023 and 20% for Eli Lilly.

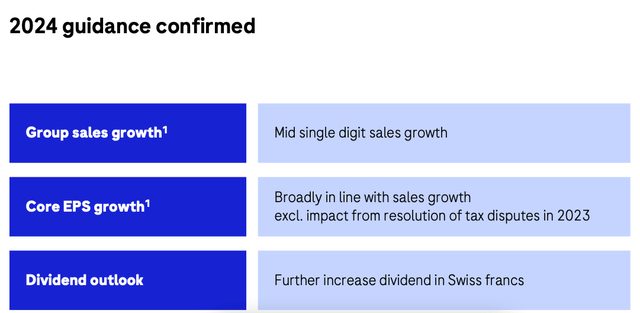

- Sales growth in Q1 2024 and outlook are muted too: Further, even going into 2024, Roche’s sales growth aren’t expected to accelerate meaningfully. In Q1 2024, for example, sales ex-Covid-19 have risen by 7%, similar to that last year. Further, even for the full year 2024, no significant pickup is expected in sales (see graphic below).

Source: Roche Holdings

Essentially, the successful development of the treatment may well significantly improve the company’s muted prospects, as demonstrated by other pharmaceutical companies’ performance.

Forward P/E shows little further upside

However, for now, the stock’s future will be determined by the expected financial results for 2024. And that’s not terribly exciting. A similar growth expectation for core earnings per share [EPS] as for revenues this year, doesn’t indicate much upside. Not after the stock’s recent uptick.

Assuming that earnings grow by 5%, as per the guidance, the forward non-GAAP price-to-earnings [P/E] ratio is at 13.7x. This is only a bit lower than Roche’s 5-year average of 14.2x, indicating less than 4% price upside for now.

There could still be a case for the Roche stock, considering that its forward P/E is trading discounted to the healthcare sector at 19.1x. But then again, its growth metrics don’t quite match up, either. In other words, the stock is seeing a relatively muted market valuation for good fundamental reasons.

Dividend aren’t bad

Investors could still stand to make some gains based solely on its dividends, though. The company does expect to see a dividend increase, which is encouraging, after it has already grown them for the past five years. Its trailing twelve months’ [TTM] dividend payout ratio of 66% doesn’t put them at risk in the foreseeable future, either. It’s not the ideal payout ratio, but it’s not the worst around either.

Further, the TTM dividend yield of 3.78% isn’t bad either. In fact, it is notably higher than the average yield of 1.47% for the healthcare sector. It’s also worth pointing out that even though Roche’s stock price hasn’t gone anywhere in the past five years, the total returns have been positive (see chart below).

Price and Total Returns, 5y (Source: Seeking Alpha)

What next?

The total returns, however, don’t make a convincing enough case for Roche. Not when its financials aren’t expected to see significant improvement anytime soon. The company’s sales growth was in single digits in 2023 at constant exchange rates and is expected to be relatively muted this year too. Moreover, continued strength in the Swiss franc can continue to shrink sales in market exchange rates. With the uptick in its price recently, there’s also limited upside based on the market valuations.

At a time when Roche can really do with a growth fillip, the latest results from its weight management treatment are certainly encouraging. This is especially true, as the challenge is enormous and other pharmaceutical companies have made significant gains from their treatments in the segment. However, this potential is yet to be realized. It’s worth looking out for, though. Meanwhile, I’m going with a Hold on Roche Holding.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Credit: Source link

{kind=link}