DarrenMower/E+ via Getty Images

Investment Thesis

Roadzen (NASDAQ:RDZN) saw its share price jump more than 50% premarket. Shareholders, who have had a torrid period, with their shares moving lower more than 70% in the past 2 months, breathed a sigh of relief that its fiscal Q4 2024 results were not worse.

However, I declare that this business has too many hairs on it. That its path to profitability is straddled by its heavily indentured balance sheet.

In brief, investors would do well to skip this opportunity to buy RDZN.

Why Roadzen? Why Now?

Roadzen is a technology company that aims to revolutionize the auto insurance industry using AI. They partner with insurers, car manufacturers, and fleet operators to provide more transparent, efficient, and seamless insurance products and services. By integrating computer vision, telematics, and AI, Roadzen helps create better insurance products, assess damages accurately, process claims faster, and improve driver safety.

Roadzen’s value proposition lies in its ability to transform the auto insurance landscape by leveraging cutting-edge technology. They offer a comprehensive platform that enhances every aspect of the insurance value chain, from underwriting and claims processing to road safety. Their AI-driven solutions allow for real-time data analysis and dynamic policy adjustments, making insurance more personalized.

Their contention is that Roadzen not only improves customer satisfaction by speeding up processes like claims handling but also helps insurers manage risks better and reduce costs.

Essentially, Roadzen’s approach enables real-time data collection and analysis, leading to quicker and more accurate decision-making. In sum, Roadzen seeks to be more agile and innovative in adapting to the evolving needs of the modern auto insurance market, than say, an insurer like AXA (OTCQX:AXAHY).

Given this background, let’s now discuss its fundamentals.

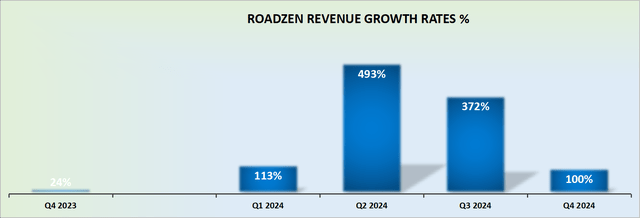

Revenue Growth Rates Are Too Volatile

RDZN revenue growth rates

Roadzen’s fiscal Q4 2024 saw its revenues increase by 100% y/y. On the surface, that’s a strong performance. But when we consider that the comparables with last year were up 24% y/y, this poses a problem.

The problem is that fiscal Q4 2023 was the last easy comparable period. Starting fiscal Q1, 2025 (this current quarter), its comparables will rapidly become more challenging. And by fiscal Q2 2025, which starts in less than 90 days, it’s reasonable to expect that Roadzen’s revenue growth rates could turn negative.

And when investors recognize that this is not the growth business they suspected it could be, they will no longer be willing to pay a premium for a colorful growth story. Instead, investors will be eyeing up its bottom line, before deciding to pass up on this investment opportunity. But there’s more, so let’s turn to it.

RDZN Stock Valuation — 4x Trailing Sales

Including the premarket jump, RDZN is priced at 4x trailing sales. But there’s no need to overcomplicate matters.

RDZN SEC 10-K

Above we see that Roadzen has about $18 million of debt, interest not included, due in less than 1 year.

What’s more, consider this excerpt from Roadzen’s SEC filings published yesterday, with reference to Mizuho’s senior secured notes, worth $7.5 million:

The Mizuho Notes bear interest at a rate of 15.0% per annum, which will automatically increase by 5% if we fail to prepay the Mizuho Notes upon the occurrence of certain mandatory prepayment events as set forth in the Note Purchase Agreement. The Mizuho Notes mature on June 30, 2024 […]

On June 30, 2024, Mizuho granted to the Company a waiver until July 31, 2024 thereby waiving the obligation to repay the Loan while the parties continue negotiations to extend the Loan and to possibly advance additional funds. There can be no assurance that the Loan will ultimately be extended beyond July 31, 2024 or that additional funds will be made available. (emphasis added)

Simply put, Roadzen, with its $11 million of cash and cash equivalents has a lot of negotiation to do in the coming few weeks, if it seeks to repay these financial notes.

On top of that, its meaningfully adjusted EBITDA reported this quarter at negative $2.2 million. In short, investors would do well to avoid this name.

The Bottom Line

In conclusion, despite Roadzen’s strong premarket surge of more than 50%, plus its compelling AI-driven value proposition in the auto insurance industry, the company’s heavily leveraged balance sheet and volatile revenue growth rates pose significant risks.

The looming debt obligations and uncertain near-term outlook overshadow the potential benefits of their technology in the long term.

Investors are advised to steer clear of this opportunity as Roadzen navigates through this financial turbulence, otherwise, Roadzen could turn them into roadkill.

Credit: Source link

{kind=link}