dusanpetkovic/iStock via Getty Images

The Thesis

After a strong 2023 with double-digit topline expansion, Powell Industries (NASDAQ:POWL) has seen nearly 50% growth in the first three quarters of 2024 as demand remains healthy across most of the end market. I expect this to continue further in quarters ahead despite near term headwinds in the Oil and Gas end market as demand in other industrial markets like Petrochemical remains robust, which along with strong backlog levels should help the company in closing 2024 with another strong quarter. Longer-term prospects also remain favorable due to the company’s continued focus on product diversification and capacity expansion. The company also continued to look for potential M&As for longer-term growth, which should benefit the company’s sales growth in the coming years. As volume grows, the company’s margin should also benefit from volume leverage, which along with benefit from operational improvements should drive margin expansion in 2024 and beyond. Overall, while POWL’s growth prospects remain promising, its attractive valuation makes it a good buy at the current levels.

Last Quarter Performance

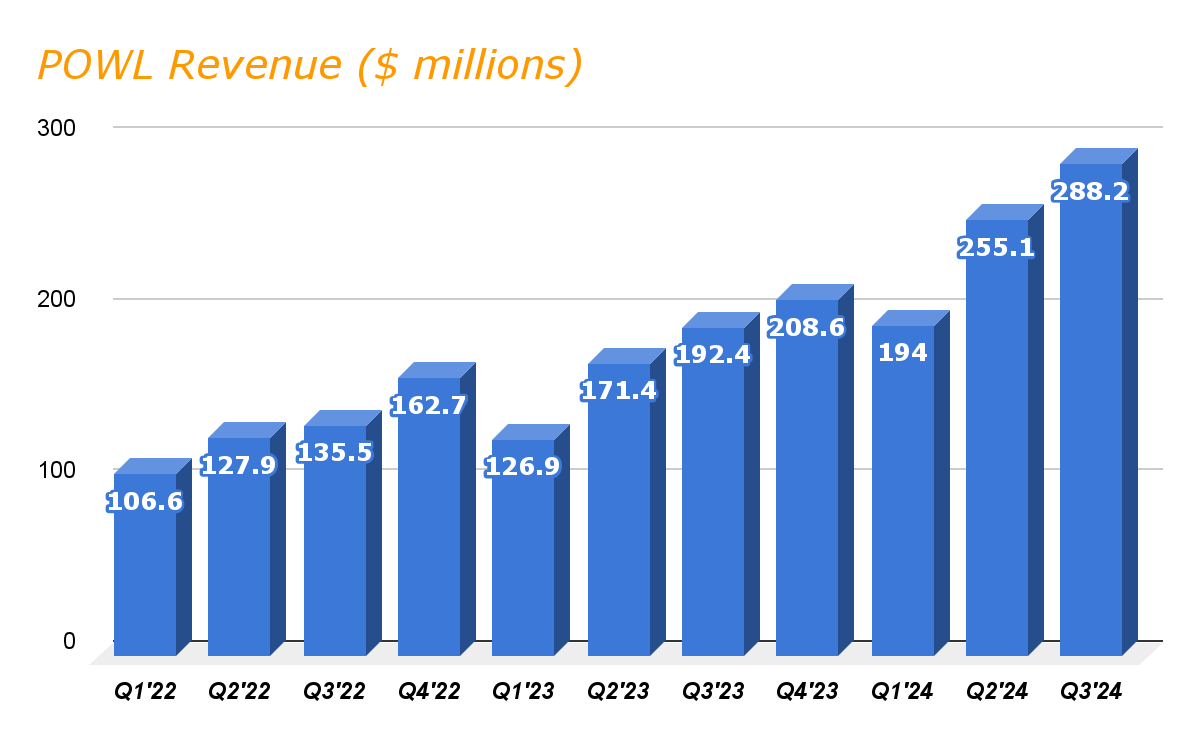

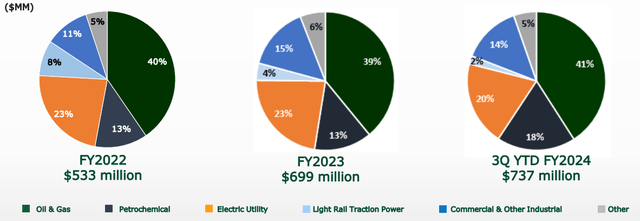

The first half was strong for POWL as its topline expanded by approximately 50%. Similarly, the company continued this strong performance into the third quarter as well, as it entered the second half of 2024 with its topline growing 49.8% year-on-year, reaching a record $288.2 million during the quarter. This growth was primarily a result of continued strength across almost all end markets the company serves, but mainly in the core industrial end markets, oil and gas, and petrochemical, which grew 56% and 158% respectively during the last quarter. New orders were, however, 30% lower year-on-year, primarily due to tougher comparison driven by two mega projects booking related to LNG in the prior year’s third quarter.

Powell Historic sales (Research Wise)

The higher volume of projects during the quarter also benefited the company’s margin, which along with benefits from strong project execution, operational leverage, and a 260 bps improvement in SG&A as a percentage of sales boosted the company’s operating margin to 19.9%, which is significantly higher than 11.2%, a year ago. A significant jump in operating profit also drove the bottom line during the quarter as the adjusted EPS more than doubled to $3.79 versus just $1.52 in Q3’23, beating the consensus estimates by a significant $1.63 during the third quarter of 2024.

Outlook

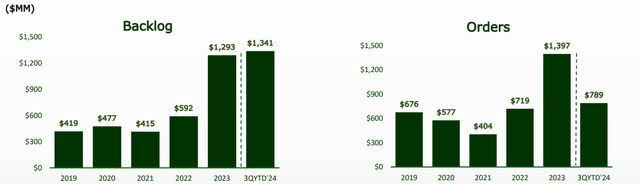

Moving into the second half, the company continued its robust performance, with its topline growing nearly 50%. I expect this growth to continue further in the coming quarter as demand for the company’s products and services remains strong across most of the geographies and end market, but primarily in the core industrial end market, leading to healthy quoting activity. In my view, this strong demand environment along with the company’s backlog levels, which remain at a record $1.3 billion as of the third quarter of 2024, should drive the company’s topline growth in 2024.

Historical Backlog and Order growth (Company presentation)

While the near term outlook remains favorable for the company, U.S. Department of Energy Policy regarding LNG export permitting is causing a slowdown in the U.S. liquified natural gas (LNG) and limiting or delaying the approval of export limits. This should lead to slowdown in activity in this market in the short term, which should also give headwinds to the company’s business in the quarters ahead. However, overall prospects remain good for the company in the near term.

End market wise revenue distribution (Company Presentation)

Going forward, the company’s capacity expansion initiative continues, which should help the company in its backlog execution and to address the anticipated volume growth in the quarters ahead. As we discussed in my last article on POWL, the company has already completed expansion of its Houston facility on the Gulf Coast, which is giving the company with fabrication and integration support for large power control rooms. In addition to this, the expansion of $11 million electrical products factory is also progressing as per plan in Houston and is expected to be completed by 2025, which should further support the company in its future growth across the customers and markets it serves. In addition to this, the company also continued to focus on its innovation initiatives to develop new technologies and diversify and enhance its product portfolio.

Furthermore, the company continues to focus on another critical area for long-term growth, strategic acquisition. Currently, the company has zero debt and improved profitability is driving decent cash flow generation, which should help the company in its potential acquisition in the future, benefiting the company’s topline in the longer term. Overall, the near term prospect continued to be favorable for the company due to healthy demand in the core end market and robust backlog levels. The company’s focus on enhancing capabilities and capacity expansion, on the other hand, should drive growth in the longer term.

Valuation

Since my last bullish article on POWL in July 2024, the stock has been highly volatile. Initially, this was due to a significant decline in Super Micro Computer’s (SMCI) stock. And then, due to concerns arose around NVIDIA (NVDA) following allegations by the DOJ of wrongful practices, creating panic among investors and causing NVIDIA’s stock to drop significantly in the last few trading sessions.

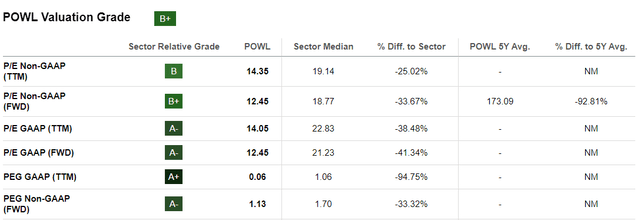

As companies like POWL also stand to benefit from the artificial intelligence boom alongside Super Micro and Nvidia, POWL’s stock also experienced a significant decline. The stock price dropped to nearly $150 after reaching a one-month high of $196.75 in the last week of August. However, despite this recent correction, the stock is still up in the high-single digits since my article and up approximately 70% YTD. Currently, the company’s stock is trading at a forward Non-GAAP price to earnings ratio of 12.45 based on FY24 EPS estimates of $12.07, representing a significant improvement from 15.46x since my last article, primarily due to the recent stock correction. While comparing with the five-year average P/E ratio of 173.09x, the stock appears to be significantly discounted.

POWL Valuation grade (Seeking Alpha)

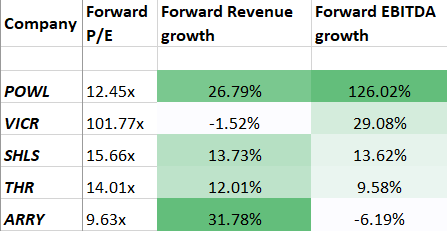

The sector median also shows the company’s stock at an attractive valuation against its close peers like Vicor Corporation (VICR), Shoals Technologies (SHLS), Thermon Group Holdings (THR) and Array Technologies (ARRY). While the company’s valuation appears to be lower than its peers’ averages, POWL also has better forward growth compared to them, as we can see in the table below.

Peer comparison (Research Wise)

Going ahead, I expect the company’s topline growth to continue further as the demand for the company’s solution remains healthy across most of the end market, but primarily in the core industrial end market, which should drive volume growth in 2024. The benefit from higher volume along with operation benefits from better execution should drive margin growth for the company in the quarters ahead, leading to bottom line expansion and further improvement in the company’s stock valuation, making this stock a decent investment opportunity.

Risk

As we have seen strong top and bottom line growth in the recent quarter, I am expecting this to continue further, which should further help the company in enhancing its valuation. However, if the company fails to meet expectations and margin growth suffers, its bottom line might be negatively impacted, potentially leading to poor stock performance in the future. Apart from the company’s performance, we’ve seen how giants in the chip industry like Nvidia and Super Micro have recently dragged down POWL’s stock. If concerns around these stocks persist, POWL’s stock performance could also be negatively impacted in the future.

Conclusion

As discussed earlier, the company’s stock valuation has improved notably since my last article, followed by correction in stock price and currently trading at a significant discount to both its historical average and sector median. In my opinion, the growth across the top line should continue further in the rest of 2024 due to healthy activity and strong backlog level. Long term also remains promising as the company remains focused on product diversification and capacity expansion to deal with anticipated growth in demand in the future. Considering the strong long-term growth prospects and an even more attractive valuation, I would strongly suggest buying this stock for the long term.

Credit: Source link

{kind=link}