Torsten Asmus

Permian Resources (NYSE:PR) reported strong Q1 2024 results after making fast progress in integrating its acquisition of Earthstone Energy. It increased its full-year guidance for both total production and oil production by 2%. That doesn’t include the impact of some additional acquisitions that Permian made (totaling $270 million in consideration) that should boost its 2H 2024 production by another percent.

Permian is now expecting an extra $50 million per year in cost savings (up to $225 million per year) from its Earthstone acquisition. The additional costs savings plus Permian’s increased production helps boost its estimated value to $18 per share, up $1 from when I last looked at the company.

Q1 2024 Production

Permian Resources announced strong Q1 2024 results with 319,514 BOEPD in total production, including 151,794 barrels per day in oil production. Permian noted that its oil production increased by 11% compared to Q4 2023, although that quarter only included two months contribution from Earthstone since that acquisition closed one month into the quarter. Permian’s oil production would have been fairly similar quarter-over-quarter if the Earthstone acquisition had closed at the start of Q4 2023.

The better than expected Q1 2024 production results were attributed to excellent well results along with the fast integration of Earthstone. Permian has reduced the production downtime associated with Earthstone’s assets.

Increased Synergies

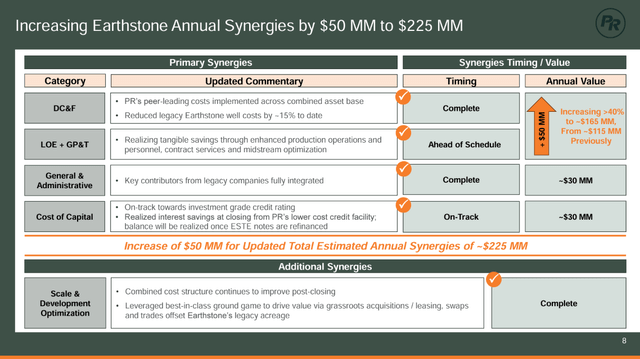

Permian announced that its integration of Earthstone was finished ahead of schedule and that it increased its annual synergy target by $50 million. Permian now is aiming for $225 million in annualized savings.

This $50 million in additional savings is expected to come from a combination of further reductions in D&C costs and operating costs. Permian has now reduced Earthstone’s D&C costs by approximately 15%, more than the roughly 12% reduction it mentioned a few months ago. By May 1st, Permian was no longer using any of Earthstone’s drilling rigs or completion crews.

Earthstone Deal Synergies (permianres.com (Q1 2024 Presentation))

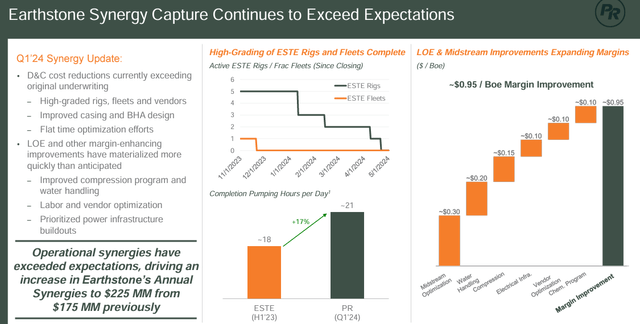

Permian also mentioned that it had significantly reduced Earthstone’s production downtime and improved margins on Earthstone’s production by nearly $1 per BOE through midstream optimization initiatives and other efforts.

Margin Improvements (permianres.com (Q1 2024 Presentation))

Administrative Liquidation

Permian announced that it liquidated Lynden Energy Corp. as an administrative move. This move simplifies Permian’s corporate structure and reduces its go forward tax obligations and doesn’t affect its guidance.

Earthstone announced its acquisition of Lynden Energy in 2015 to enter the Permian. At the time, Earthstone was mostly an Eagle Ford producer. Lynden Energy was a Canadian (British Columbia) company that was a subsidiary of Earthstone due to that 2015 acquisition. Although Lynden was Canadian, its oil and gas assets were American and nearly all in the Permian Basin.

This moves saves Permian the work of being a reporting issuer in Canada, but is otherwise more interesting for how it highlights how fast Earthstone grew through acquisitions.

In Q3 2015 (pre-Lynden acquisition), Earthstone was producing under 5,000 BOEPD. By the time of its acquisition by Permian Resources it was producing around 130,000 BOEPD and now Permian is expecting to average around 320,000 BOEPD in 2024. Centennial Resource Development (which combined with Colgate Energy to form Permian Resources) only averaged a bit over 7,300 BOEPD in 2015.

Additional Acquisitions

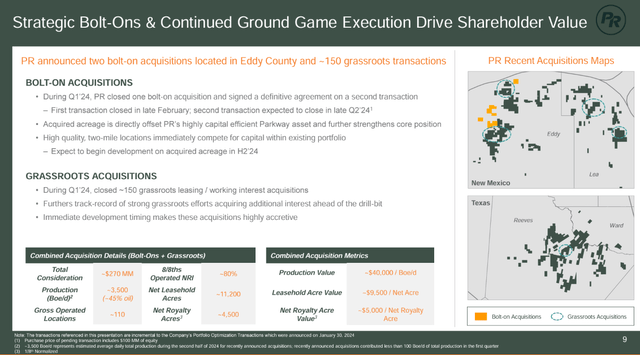

Permian also recently announced some additional transactions. For the combined transactions it added 11,200 net leasehold acres and 4,500 net royalty acres for approximately $270 million in total consideration, including $170 million in cash. The acquired royalty acreage helps the royalty burden to approximately 20% compared to the typical 25% in the area.

The acquired assets contributed less than 100 BOEPD to Permian’s Q1 2024 results but are expected to contribute 3,500 BOEPD (45% oil) to its 2H 2024 results. Permian mentioned that it expects to begin development on its bolt-on acquisitions in 2H 2024, while its grassroots acquisitions were completed just ahead of immediate development efforts on that acreage.

Permian’s Acquisitions (permianres.com (Q1 2024 Presentation))

Due to the 2H 2024 development, Permian expects approximately $50 million in incremental capex related to these acquisitions in the second half of the year.

Updated 2024 Outlook

Permian increased its full-year guidance midpoint to 320,000 BOEPD, including 150,000 barrels of oil per day (47% oil cut). This was a 2% increase in both total production and oil production guidance.

This doesn’t have the impact of the recent acquisitions that Permian expects to add 3,500 BOEPD (45% oil) to its 2H 2024 production. Thus, I am modeling Permian’s full-year 2024 results at around 322,000 BOEPD, including approximately 151,000 barrels per day of oil production.

At that level of production and at current strip prices of roughly $80 WTI oil and $2.50 Henry Hub natural gas for 2024, Permian is projected to generate $5.310 billion in revenues after hedges.

| Type | Units | $/Unit | $ Million |

| Oil (Barrels) | 55,115,000 | $79.00 | $4,354 |

| NGLs (Barrels) | 27,224,910 | $26.00 | $708 |

| Natural Gas [MCF] | 212,163,150 | $1.30 | $276 |

| Hedge Value | -$28 | ||

| Total Revenue | $5,310 |

Permian’s capital expenditure budget should be around $2.05 billion now, with the incremental $50 million in capex associated with its recent acquisitions.

| Expenses | $ Million |

| Lease Operating, Cash G&A and GP&T | $943 |

| Production Taxes | $400 |

| Cash Interest | $260 |

| Capital Expenditures | $2,050 |

| Cash Income Taxes | $45 |

| Merger Integration Costs | $20 |

| Total Expenses | $3,718 |

Permian is now projected to generate $1.592 billion in free cash flow in 2024 despite the modest increase in spending.

The additional $50 million in 2H 2024 capex will likely only be around half paid back by the end of 2024 from the net revenues generated by the 3,500 BOEPD in added 2H 2024 volumes. Thus, that investment has a slight negative effect on 2024 free cash flow but will benefit Permian’s 2025 results.

Notes On Valuation

I’ve increased my estimate of Permian’s value by $1 per share to a new estimate of $18 per share. This is based on my long-term (after 2024) commodity prices of $75 WTI oil and $3.75 Henry Hub natural gas.

The increase in Permian’s estimated value reflects the positive revision to its 2024 production guidance, as well as the additional $50 million in annual synergies it believes it can achieve from the Earthstone deal.

With Permian trading at a bit over $16 per share now, I consider it a better value than a few months ago and have moved it to a buy rating again. Permian traded at a bit over $18 in April 2024.

Conclusion

Permian Resources delivered strong Q1 2024 results that contributed to its increasing its full-year production guidance by 2%. It should be able to generate close to $1.6 billion in 2024 free cash flow at current strip prices now.

Permian now also expects to achieve $225 million in annual synergies from its Earthstone Energy deal, up from $175 million before. The combination of increased synergies and improved production expectations increases Permian’s estimated value to $18 per share at long-term $75 WTI oil and $3.75 Henry Hub natural gas now. I consider it just undervalued enough to warrant a buy rating now.

Credit: Source link

{kind=link}