Daniel Grizelj

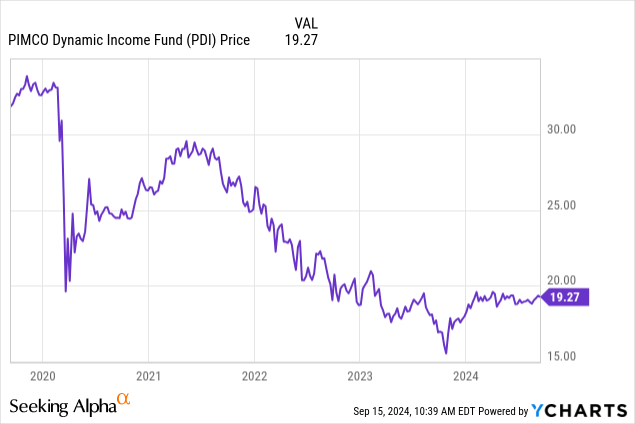

The PIMCO Dynamic Income Fund (NYSE:PDI) is a name that we had issued an income buy alert for in October 2023. The timing was fortunate as we had caught a medium-term bottom in the trading pattern. When it comes to income names, price does matter. We comfortably moved to a hold rating earlier this year, and since then, the price has barely moved, but with dividends the total return thus far is 4.4%, paltry, but decent when you consider you are buying this for income. Often, at least in the near- and medium-term, overpaying when the market is juiced can lead to a natural ebb and flow correction in price, and it can take time to get back to even from the dividends. However, as long as the fund performs well over time and the dividend payments are stable, long-term the price you pay does not matter all that much. Still, it is best to either time your big lot buys to take advantage of dips, or dollar cost average with regular buys over time. Today, we check back in on the PIMCO Dynamic Income Fund, or PDI. This is a closed-end mutual fund or CEF that seeks to provide investors a high level of income. In our opinion, the upside from here is limited right now, but that is not necessarily a bad thing since this is really an income instrument.

If you buy right now, you can collect a 13.7% yield. Looking to the recent trading channel and assuming a continued level dividend, in the near-term the shares have been a buy at a 14.1% yield, or around $18.70 per share. The fund has bounced off of this level a few times this year. It may be splitting hairs, but that entry difference is several months’ worth of dividends. Regardless, for the long term, we like this instrument for income in the $18-$19 range. What we love about income names like this, provided the dividend (and special dividend) is paid at the same level over time, with no cuts (or even raises) you can recoup your principal investment back in dividends in a little over 7 years at current rates. Now, reality will differ based on trading patterns and dividend payments, but in time you will be playing with the house’s money.

Earlier this year, we have opined that 2024 would be a strong year for income instruments because we were expecting rate cuts this year. Finally, in recent months, we have seen a good number of defensive and income type stocks start to move. While PDI has not moved, it has held firm. Right now, we expect 2 cuts, with the first one coming this week at the September fed meeting. That view may change based on data, but that is what we see right now. However, we think you get to neutral by H2 2025, so income on cash will no longer be all that attractive, and money will come back into income. That is more of a single income type stock story, but PDI’s approach is working. However during periods of market weakness, PDI also takes a hit. If you look out longer-term, PDI is still down heavily from years ago, but has traded sideways in 2024, and is up well over 20% in total returns from our October 2023 call.

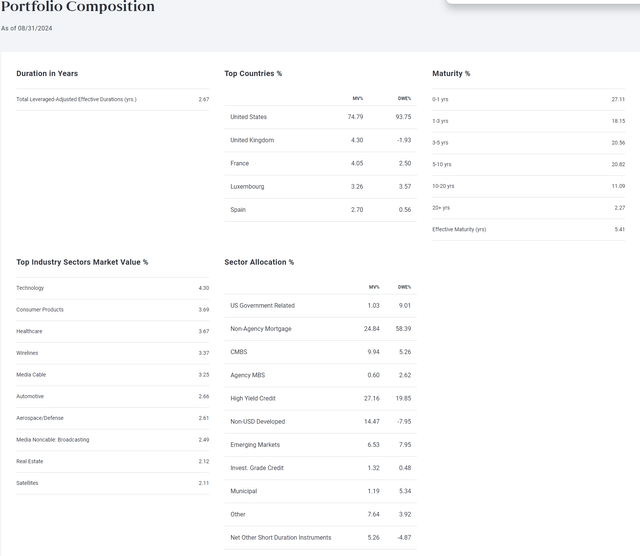

So those who have been in Pre-COVID, or bought in mid-2021 have been crushed in terms of the principal. So, we can understand if some are skeptical to wanting to own this for yield. That is, we see fear of more principal erosion. Relatively stable markets are good for this fund. Long term, this is a strong fund, with an interesting approach. It is a diversified portfolio of fixed income securities, which includes government and corporate bonds, as well as mortgage-backed securities, asset-backed securities, and other debt instruments like high-yield corporate bonds. It has instruments with a variety of maturities. As a reminder, give or take some on the margins, the fund invests at a minimum of 25% of assets under management in non-agency mortgage-related securities. Up to 40% of the fund can be invested in emerging market countries or entities tied to such exposure. The portfolio duration can range between zero and eight years, but on balance is in the middle of the range. And yes, there is also leverage in the portfolio to magnify returns and pay out that bountiful income. However, this is why when markets are volatile for an extended period, particularly the bond/mortgage markets, the significant leverage can move NAV lower. However, the structure of the fund permits management to take quick action to adjust holdings to market conditions. Still, the company does have over 1,700 holdings. Here is a snapshot of the portfolio composition (as of 8/31/24) on PIMCO’s website:

PIMCO Dynamic Income Fund Website

There are many diverse holdings, but this snapshot provides a higher-level overview of holdings and sector allocations. As you can see, as usual, there is heavy investment in debt obligations and other income-producing securities. There are approximately $8.75 billion in assets managed at the time of this writing. So why did the fund fall so hard from mid-2021? This was a result of the expectation for and reality of a rapidly changing environment for rates, which hurt returns on the MBS and other debt holdings. So this is the near-term risk right now. Rate cuts, if occurring rapidly instead of orderly, could impact MBS holdings or returns on debt in the near-term. Keep this in mind. However, the Fed does not want to risk inflation resurging. So we see a slow and orderly cut to rates over the next year, so we think it will be well managed. However, if economic data worsens rapidly in the next few months, cuts could be more rapid.

As you can now see, bonds have surged (yields are lower) on the expectation of these cuts. Investors were locking in that yield. So even though the cuts have not occurred, the bond market moved first. In short, the value of most bonds, bond funds, and fixed income securities are impacted by changes in interest rates and are often ahead of the curve. Mortgage and asset-backed securities which PDI invests in are sensitive to changes in interest rates, but are subject to early repayment risk and so if rates come down quickly. This is because prepayments will spike. As such, their value may be volatile in response to the market’s perception of issuer creditworthiness or prepayment risk. So this is a risk.

With that said, PDI has a rough midpoint portfolio maturity ranging from zero to eight years as mentioned, and in the graphic above it is shown average leveraged maturity is 2.67 years, with effective maturity in over 5 years. However, 27% of the holdings have a maturity of less than a year, while nearly 14% have a maturity of over 10 years. Because the investments provide high returns, it can pay the bountiful monthly dividend and special dividends over time and has been doing so for more than two decades.

That said, we started the piece with how price matters. Seeing a nice discount to the fund’s net asset value is rare. When it last occurred in 2023 we slapped a buy on the Fund. But today, you are paying a premium. We much prefer to do some buying when you can acquire some closer to NAV. NAV as of 9/12 was $17.30. So you are paying nearly a $2 or an 11.5% premium. Long-term this is a diversified and well-managed fund for high income, but when debt instruments are in a period of flux the fund does tend to suffer. This is something that is a risk if interest rates move too quickly, even to the downside. Still, we think cuts will be orderly. There is also credit risk, and you have to be comfortable with the leverage. However, the payout is bountiful and paychecks arrive monthly. While we think it’s best to wait for the next draw-down closer to or beneath NAV, PDI does make a good income vehicle choice.

Your thoughts on PDI?

How do you handle PDI? Do you add regularly or wait for dips? Are you in agreement that the fund can take a hit if rates move too quickly? Is there a fund you prefer to PDI? Let the community know below.

Credit: Source link

{kind=link}