Kirkikis/iStock Editorial via Getty Images

One more deal to acquire Paramount (NASDAQ:PARA) has reportedly fallen through and details about potential new offers are rather murky. We have been holding the stock assuming that fairly low-risk profits could be pocketed given the significant discount to the sum-of-the-parts value that the company is trading at. This has proven to be a lot more difficult than we anticipated.

We have covered PARA previously in our articles:

- Paramount: The Market Does Not Buy Byron Allen: we explored scenario analysis of future potential deals, Skydance deal was discussed as a worst-case scenario.

- Paramount: One Big Content Factory: we discussed the scale advantages of PARA and the value of sharing content between linear and streaming.

- Paramount: Potential Merger Arbitrage With Downside Protection: we estimated the value of the PARA equity to be about ~$19 billion, based on SOTP.

We have been wrong, not about the value of the assets, but rather about the willingness of Shari Redstone as well as many potential suitors to strike a deal. Financing in the current environment also has not been easy. It’s time to start considering alternative scenarios.

We believe it is likely that Paramount will attempt to slug it out as an independent entity, and it would not necessarily be the worst outcome for the common shareholders. Skydance, for example, was proposing to dilute common shareholders at depressed prices. Other financial suitors are also likely to try to take advantage of the National Amusement voting control at the expense of common Paramount stockholders.

The going-it-alone scenario might not be as profitable as an acquisition at a fair value, but it has become quite clear that nobody will acquire PARA at a fair value to common holders. Staying independent is likely to be more beneficial to common folk of PARA, than riding with Skydance or other private equity-backed groups at the helm.

We are not happy about how this acquisition saga has panned out, – probably nobody is. On the other hand, we are at least encouraged that Ms Redstone did not sell common PARA holders down the river.

We still believe PARA is cheap, and therefore we continue to hold our position.

The financial leverage is the key sticking point to the idea of Paramount staying independent, – it should not be

Leverage has been broadly discussed as a key issue of Paramount. We believe that these concerns have been overblown as the business is rich in content franchise assets as well as real estate. The values of these assets far outweigh the debt that the company carries.

Paramount, though, does have free cash flow generation issues that stem from excessive content and marketing spending on the streaming business. The business essentially pours every dollar of profits it generates back into the business. Excessive investment is a self-inflicted issue that can easily be repaired.

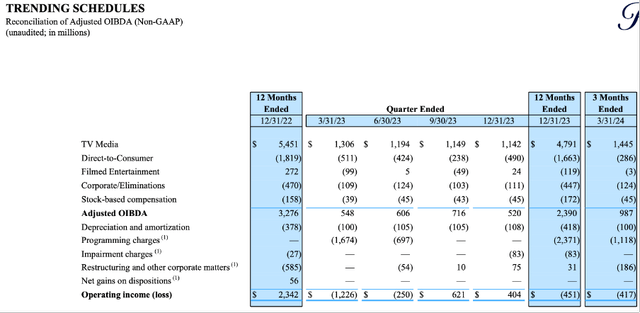

The Linear TV business is a key cash flow-generating engine of the group, delivering ~$4.8 billion of OIBDA during FY2023. Streaming, on the other hand, was the key OIBDA detractor.

Paramount Q1 FY2024

Paramount just has to scale down spending on streaming, even if it means losing customers. This loss would not be an issue either as currently, the market ascribes practically no value to the 71 million customer base of Paramount+ anyway. Higher free cash flows would boost the equity value of PARA and de-risk the balance sheet while the loss of DTC customers would not have any negative counterbalancing effect. Slashing DTC spending would be a win-win!

If the DTC business starts being run on a breakeven OIBDA level, the group-adjusted leverage would improve considerably. Assuming the same level of TV Media profitability and breakeven Streaming as well as Filmed Entertainment performance, an OIBDA of the group could easily reach ~$4.2 billion. Providing a leverage level of 3.5X EBITDA, – a rather high but manageable level for a cash-generative business. By comparison, Warner Bros. (WBD) operates with a leverage level of 4.5X.

WBD can withstand these higher leverage levels as it generates a lot of free cash flow and can progressively deleverage even as its linear media profits decline. The reason why the lower level of leverage at Paramount is seen as an issue is the lack of free cash generation.

Strategic Streaming realignment could allow Paramount to save $2.7 billion free cash per annum

We do not believe that it would be wise to discontinue Paramount+, even given its losses. Significant value can be extracted from this asset, but a larger scale is needed and PARA does not have the resources to continue growing the platform by itself. A deep partnership with another operator, such as Comcast’s (CMCSA) Peacock, would be the best option.

A JV or other type of deep partnership would allow DTC business to leverage the fixed marketing, technology and content costs over a lot larger revenue base. We believe that a streaming platform of a considerably larger scale would be able to operate at least on a free-cash-flow-neutral basis.

During FY2023, the DTC business of Paramount delivered a negative $1.7 billion OIBDA. On top of this, the original and licensed content spending was increasing, pushing overall cash spending up. Group-wide, cash content spending exceeded content amortisation expense by ~$1 billion, most of this excess must have been allocated to Streaming. It is therefore likely that Paramount has had to infuse the accounts of its DTC operation by ~$2.7 billion during FY2023. This cash could instead have been spent on dividends, buybacks or debt pay-down.

Paramount has disclosed its intention to explore strategic investment options in its latest annual shareholders meeting. On top of this, the company has outlined plans to cut costs and divest assets. Specifics were not discussed, but it was hinted that a previously interested party could still have an offer on the table. It was speculated by the media that Paramount+ could combine with Peacock.

Plans from streaming JV were previously shelved as merger talks have intensified, and several interested parties submitted their bids for Paramount Group. If the bidding contest would come to an end, the streaming JV could again be in the works.

Deconsolidation of the Streaming business could enable Paramount to report about $2 billion in earnings, which would equate to a PE ratio of 3.6X at today’s market cap. This does look cheap, but the Linear TV business is in decline and could potentially experience an annual low double-digit earnings decline trend. Any meaningful upside to the current share price would have to come from the value of the streaming JV and the Paramount Pictures Studios.

Paramount Studios is the hidden balance sheet asset, not contributing much to earnings

The 3.6X PE estimate is based on the previously made assumption of the Filmed Entertainment division achieving a break-even OIBDA. Essentially, up till now we assumed that Paramount Studios, with its IP treasure trove and Hollywood real estate, is worthless. This is obviously not the case.

In our previous articles, discussing the sum of the parts value of Paramount, one of the main obstacles we faced was the uncertain valuation of Paramount Pictures. The business is somewhat subscale and generates low OIBDA margins. On the other hand, it sits on incredibly valuable real estate and owns some iconic intellectual property that many in the industry would want to acquire.

As of late, the market value of the Filmed Entertainment division has become apparent. Apollo Global Management has reportedly offered $11 billion to acquire Paramount Studios. We are not surprised by the size of this bid, considering that in the case of MGM, the content catalogue alone was acquired for $8.5 billion. Paramount Pictures has a catalogue of similar size, and it also owns the prime Hollywood lot.

Considering that the overall Net Debt of Paramount is ~$14 billion, an $11 billion disposal of Studios would enable the company to deleverage considerably. The Studios do not contribute significant OIBDA. Therefore, disposal would reduce Net Debt but not the profits. Thus, leverage ratios could improve considerably to below 0.8X OIBDA if the DTC business was also de-consolidated.

Why would Ms Redstone refuse to sell Paramount Pictures, but agree to let go of Paramount Group?

We must note here that we believe Ms Redstone is unwilling to sell this trophy asset. Many industry observers point out the lack of synergy between TV Media and Filmed Entertainment, and we tend to agree. Ms Redstone, on the other hand, claims that a movie studio is essential for any content distribution business. To our knowledge, she has never explained why this studio has to be located on Melrose Avenue.

Why would Ms Redstone consider selling her controlling stake in the company instead of selling off Paramount Pictures and repairing the group, we do not know. Maybe Ms Redstone had no intention to sell her control of PARA in the first place and just wanted to see what strategic options and values the market is offering and who is interested.

Even if the whole division is not for sale, the company has the strategic option to sell some of its content rights. As it became apparent from the MGM transaction, these assets could be of significant value and some nonstrategic franchises could be sold off to reduce the leverage of the group.

Even if the Studios are not divested, content rights disposals paired with deep strategic partnership for the Streaming business would enable Paramount to improve its financials and continue operating independently.

The Bottom Line

Paramount Global is probably one of the most hated stocks on the street right now. The company has been troubled for many years by a lack of strong strategic leadership and internal in-fighting. Most recently, they have failed to capitalise on its valuable asset base to secure an attractive acquisition proposal.

The guiding vision of Ms Shari Redstone was to scale up the content production and distribution business by merging broadcast networks, cable and film studios to get ready for the direct distribution world. It seems that she was taken by surprise when nobody showed interest in keeping this portfolio of businesses together.

We hope that the most recent dealmaking rollercoaster was a sobering experience for the controlling shareholders of PARA. It seems apparent that the current business portfolio is not suitable for the markets and a fair value for the group of assets will not be secured. If Ms Redstone wants to avoid giving up control at depressed price levels, hard strategic decisions have to be made.

First, Paramount Plus has to be merged with another streaming operator. Second, significant asset sales must be considered. We believe that PARA has a lot of valuable assets, and therefore they do have options. We hope that Ms Redstone chooses this option, instead of selling control to private equity.

We continue holding our PARA stock, but at the moment we do not intend to increase our position.

Credit: Source link

{kind=link}