urbazon

To say that demand for weight loss drugs and demand for the stocks of companies that produce them is robust would be an understatement. Over the past year, stocks like Novo Nordisk A/S (NVO) and Eli Lilly and Company (LLY) have had returns and ballooned to valuation levels unheard of for mature large-cap drug companies. Demand for NVO’s drugs Ozempic and Wegovy is so great after the weight loss benefits were discovered that the company struggles to produce enough of each. But this article isn’t about NVO as there are plenty of excellent reads on Seeking Alpha and elsewhere about the company. I focus on writing about and analyzing small-cap stocks. The type of stocks that one can see extremely impressive returns if they get in at or near the ground floor. Rather than chasing NVO at current valuations, investors who feel they are late to the party might consider a speculative investment in Omega Therapeutics, Inc. (NASDAQ:OMGA) instead.

There was an article recently written about OMGA by fellow Seeking Alpha author Galzus Research that describes the science behind the company’s OMEGA platform. OMGA seeks to develop a new class of programmable epigenomic mRNA medicines for unprecedented control of gene regulation and cellular function in hopes of treating or curing a broad range of diseases. Galzus put a neutral rating on the stock as OMGA’s mostly pre-clinical pipeline was too early for their risk level, but they also recognized the hype potential due to the recently announced partnership with NVO and the potential for more partnerships like this. As someone with a higher risk tolerance, I will attempt to make the case that OMGA is a uniquely positioned stock to benefit from the sudden change in sentiment in junior biotech, accelerated by the specific hype surrounding the surging demand for weight loss drugs.

Details of the Novo Nordisk deal with Omega

On January 4th, Novo announced collaborations with Omega and Cellarity on novel treatment approaches for cardiometabolic diseases. This represented the first deal struck between itself and Flagship Pioneering, the incubator of more than two dozen biotech companies, some of which are publicly listed. That includes both the public company Omega and the private company Cellarity. Immediately after its announcement, OMGA shot up to as high as $6.30 on January 4th, and closed the day at $5.32, up 95% on the day. NVO also rose 4% that day to $107.63 from $103.62, adding about $18 billion in market cap.

OMGA has since pulled back to the $4 to $5 mark with high volatility after more details about the collaboration were outlined in OMGA’s SEC filing. In exchange for the right to use OMGA’s IP in exploring potential treatments for obesity management, NVO agreed to make an upfront cash payment of $10 million, up to $522 million in future development and sales milestone payments, and mid and high-single digit to low double-digit percentage royalties on net sales of the licensed product. These payments will be shared approximately equally between OMGA and Pioneering Medicines. The nature of the split between OMGA and Pioneering Medicines wasn’t made clear in NVO’s press release, and some traders may have sold the stock thinking the deal was more lucrative to OMGA than it was. The upfront payment of only $5 million does little to extend OMGA’s cash runway, which is around four quarters based on existing cash reserves and burn rate.

While the deal is not as lucrative as one would first think when reading NVO’s press release, any collaboration that could result in the next generation of Wegovy or Ozempic is going to have tremendous and long-lasting hype potential. OMGA sitting at less than a $300 million market cap is a steal for speculative investors. As mentioned previously, NVO gained $4 per share or $18 billion in market cap on the day it announced the collaboration and has since kept most of those gains. If OMGA was to be valued at just 5% of this perceived valuation boost on NVO, it would be worth $900 million. Other market forces have been at play, but it appears to me that OMGA’s contribution and entitlement to the collaboration has been thus far underappreciated by the market relative to NVO’s.

Flagship Pioneering shows bullishness on OMGA

As an incubator of numerous publicly listed healthcare and technology listings over the past two decades, Flagship has built itself an impressive portfolio of holdings that it’s legally required to disclose. The largest of which is Moderna, Inc. (MRNA), the company that brought mRNA technology to the forefront of popular culture and political debate during the COVID-19 pandemic.

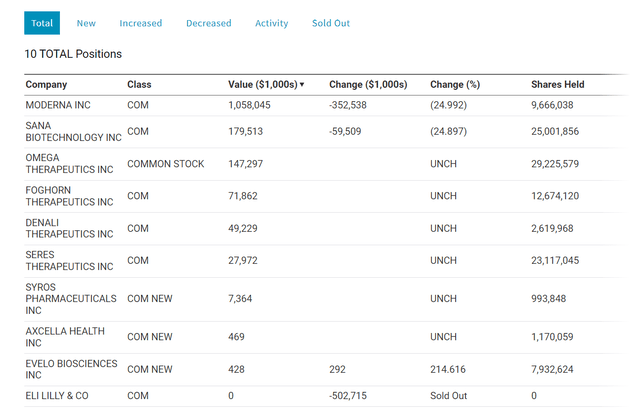

A review of Flagship’s holdings gives us a clue on how it feels about OMGA:

www.nasdaq.com/market-activity/institutional-portfolio/flagship-pioneering-inc-745144

OMGA is currently Flagship’s third-largest holding. However, the company sold a significant amount of shares in the two positions larger than it – MRNA and Sana Biotechnology, Inc. (SANA) – approximately 25% of its stake in each. Leaving OMGA as the largest holding for which it has not sold any shares. In addition to that, it sold out its entire $500 million stake in LLY. Presumably to facilitate the NVO deal with OMGA so as to not appear to have any conflict of interest in the eyes of NVO. Conversely, Flagship could feel so strongly about the collaboration resulting in a such superior weight loss drug that it’s no longer bullish on LLY. Either way, selling a $500 million position in a portfolio that is less than $2 billion in order to facilitate a transaction on a holding that is $150 million in size screams bullish. Imagine selling your second-largest holding that comprises 25% of your portfolio in order to facilitate success on a holding that comprises less than 10% of your portfolio (at that time). You would have to be excessively bullish on that 10% holding in order to bear the potential opportunity cost of watching the stock you sold run.

Conclusion: No price target, but I feel there is massive upside potential, especially in this environment

Reading through the Galzus Research article, I can understand and respect the thought process behind the neutral rating. The company is too early stage to come up with definitive revenue estimates for which to derive a price target. Analysts currently have price targets between $10 to $15 on the stock, but targets like these tend to be notoriously bullish.

I derive my bullishness from the behavior of larger players involved in OMGA. NVO already has the Holy Grail of problems as it can barely keep up with the demand for its drugs. Yet it still is willing to investigate the next generation of weight loss drugs laced with mRNA magic to stay ahead of the competition. Flagship is making a significant bet on this success as well, dumping its LLY position and keeping all of its OMGA.

While an argument that OMGA is too early stage and speculative has merit, the mirror to that would be that given its early stage, it will take a long time to play out for better or for worse. Therefore, OMGA can remain in a bullish cycle purely on hype for the foreseeable future. One of the largest healthcare companies at the center of the weight loss drug boom is willing to fund research using OMGA’s platform and pay the company handsomely upon any success. That should be worth a sustained uptrend in speculative value assuming we see similar market conditions on small caps and speculative biotech going forward as we have had over the past several weeks.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Credit: Source link

{kind=link}