Written by Nick Ackerman, co-produced by Stanford Chemist.

The timing of my last update on NXG NextGen Infrastructure Income Fund (NYSE:NXG) turned out to be incredibly poor. The ‘Buy’ rating ultimately turned out to be a good call, but there ended up being a much better buying opportunity only about a month later. The broader market entered into correction territory, but for a fund invested in several renewable-focused companies, that led to some further downside.

Today, the discount has narrowed but the distribution remains incredibly attractive—which could continue to bring interest in the fund where it could move to a premium. That said, I’d be more patient with wanting to invest in this fund, given the current narrow discount. One could even consider taking some profits on this name if they have them, waiting for a more opportune time to invest.

NXG Basics

1-Year Z-score: 1.30

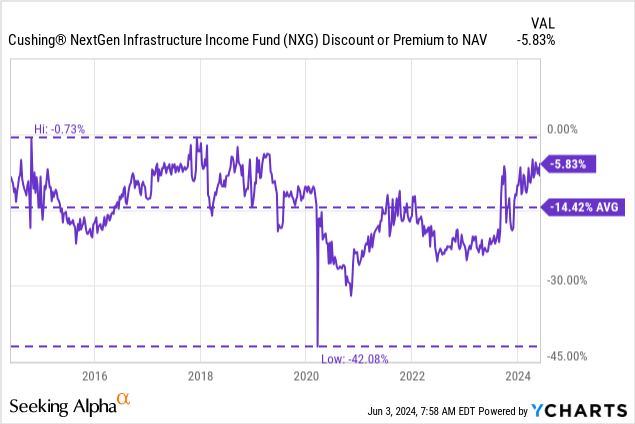

Discount: -5.83%

Distribution Yield: 15.49%

Expense Ratio: 1.94%

Leverage: 29.06%

Managed Assets: $152 million

Structure: Perpetual

NXG will seeks “to invest in a portfolio of equity and debt securities of infrastructure companies, including energy infrastructure companies, industrial infrastructure companies, sustainable infrastructure companies and technology and communication companies.”

This provides quite a flexible portfolio that embraces all things “infrastructure,” whether digital infrastructure, renewables or old-fashioned pipes.

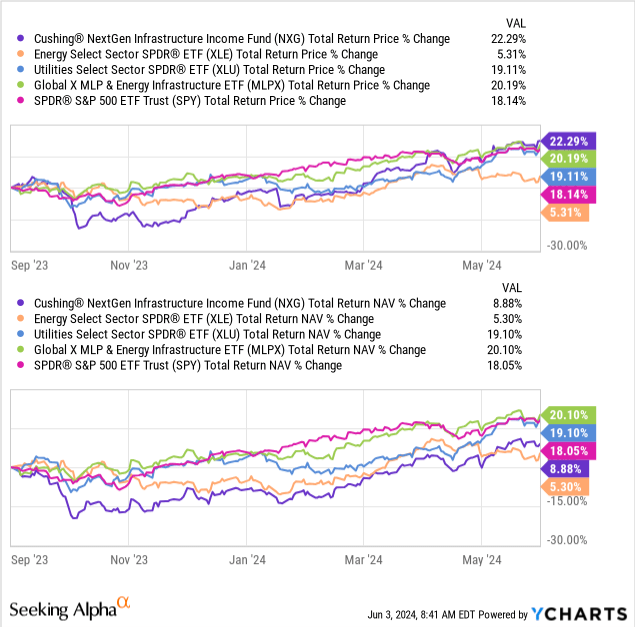

At this point, the total share price return since our prior update was 22.3%, but the timing wasn’t great. Not only did the entire market hit correction territory in October 2023, a month or so after my last update, but renewables took a significant hit during that time, too.

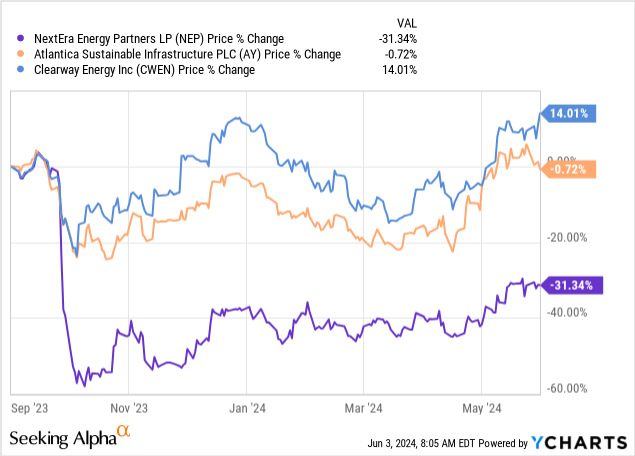

That was thanks to NextEra Energy (NEE) announcing its subsidiary, NextEra Energy Partners (NEP), was expecting about half the growth in its distribution and reducing its earnings expectations. That was merely after two months prior reiterating the expectation that things were on track. That sent shares of NEP south, but it took other renewable names with it.

At the time, NXG’s largest position was NEP, followed by Atlantica Sustainable Infrastructure plc (AY) and the fifth largest name, Clearway Energy (CWEN).

CWEN has clawed its way back higher during this time, and AY isn’t far behind. On a side note, AY is looking to be bought out, but the offer announced was actually for less than what the share price was trading at. That saw the shares dip upon that announcement more recently.

NEP is still down materially from that initial decline, but it has been grinding higher.

Ycharts

The main risk for NEP continues to be that its parent, NEE, could do a takeunder. NEP’s sole reason for existing is to benefit NEE primarily through deal drop downs and financing new renewable growth projects. If it doesn’t become a source of growth and currency for NEE, then it doesn’t need to exist.

The management team is clearly giving it some time before throwing in the towel, but that’s the general idea. NEE could suspend NEP’s distributions entirely, see the unit price absolutely collapse, and then fold it back into their business for a fraction of the current unit price. Hence, the “takeunder” risk that NEP carries.

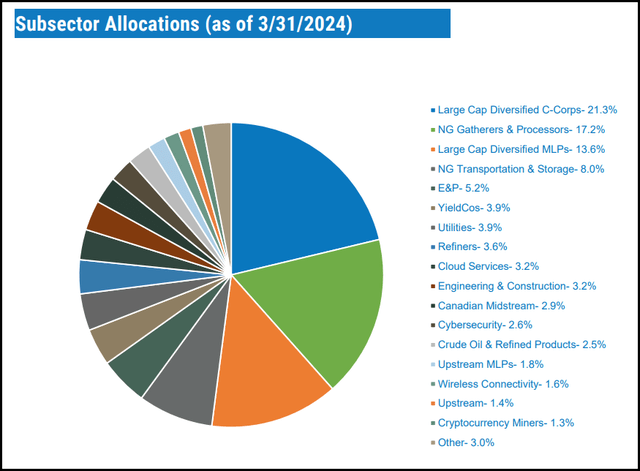

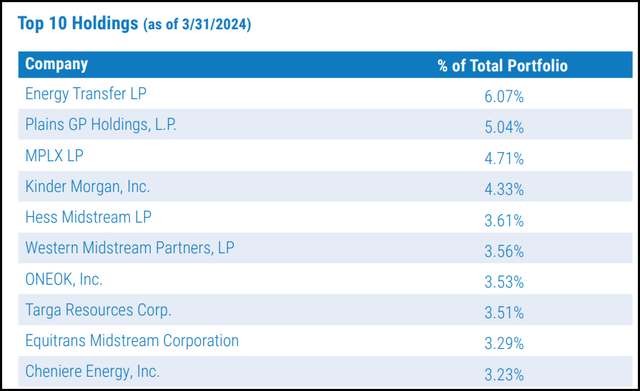

For what it’s worth, NXG no longer holds any of those three positions in its top ten. Instead, they are holding traditional pipeline C-corps and MLPs in their top ten list.

NXG Top Ten Holdings (NXG Investment Management)

For NXG, more specifically during this time, the actual underlying performance wasn’t overly strong. At least on a relative basis. The large climb for the shares came from discount contraction primarily.

For some context of performance in this time frame, we’ve also included several other securities for some sort of benchmarking. That includes the Energy Select Sector SPDR ETF (XLE), the Utilities Select Sector SPDR ETF (XLU) and Global X MLP & Infrastructure ETF (MLPX). For good measure, I’ve also thrown in the SPDR S&P 500 ETF (SPY).

Ycharts

The fund’s discount is considerably narrower than its longer-term average at the current moment. However, it may be interesting to note that prior to the Covid crash and the ultimate change in the fund to a more hybrid renewable infrastructure fund, this sort of discount wasn’t completely out of the ordinary. It is more the timeframe since Covid to now that really brought the fund’s average discount down.

Ycharts

Distribution Drives Discount Narrowing

The clear catalyst for the fund’s narrowing discount in this time frame was the doubling of the fund’s distribution. That happened right when we covered the fund initially. The fund went from covering its distribution through distributable cash flow to about 50% coverage.

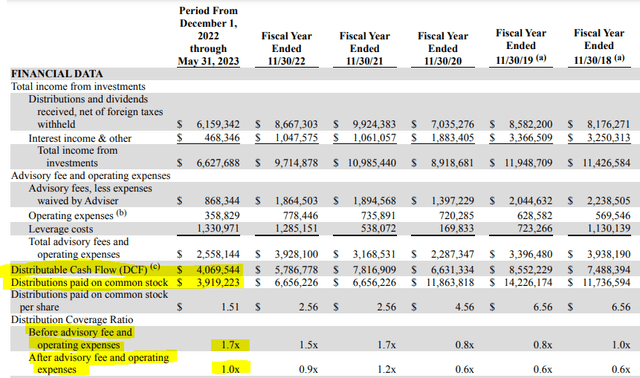

Lucky us, NXG provides the [DCF] figure for us (though it is a rather easy calculation to come up with if we had to on our own as it’s simply NII plus the ROC distributions added back in.) NXG provides a breakdown of distributable cash flow, or DCF, coverage on two different metrics, without and with the expenses of the fund. As we can see, DCF, with the expenses factored in, provides coverage at 1x. Given that the fund is an equity fund, seeing DCF coverage at 1x or greater is really all we are looking for. This coverage has also increased since the last fiscal year-end.

NXG DCF From Semi-Annual Report (NXG Investment Management (highlights from author))

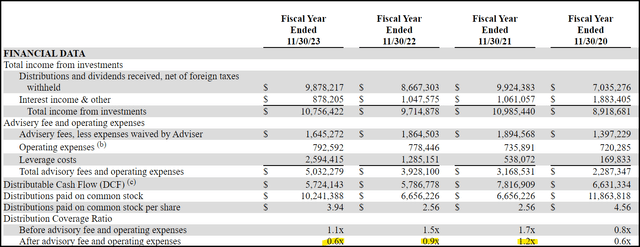

With the fund’s latest annual report, we can see that coverage already started to sink.

NXG Financial Metrics (NXG Investment Management (highlights from author))

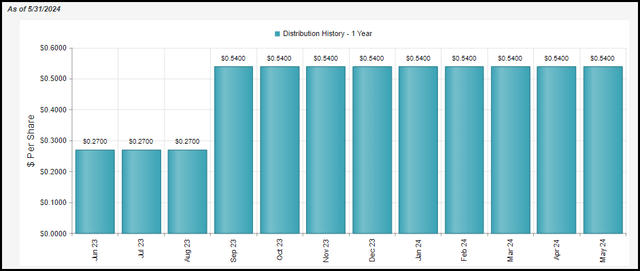

However, the higher distribution actually wasn’t in place until the September 2023 monthly distribution. So, we should see the coverage figures weaken further.

NXG 1 Year Distribution History (CEFConnect)

That said, the idea was to narrow the fund’s discount with such a move, and that certainly happened. It took it from a relatively stable infrastructure fund with a renewable hybrid lean that traded at a massive discount to more of a trader fund. Which there is nothing wrong with that at all; it just takes a bit more monitoring.

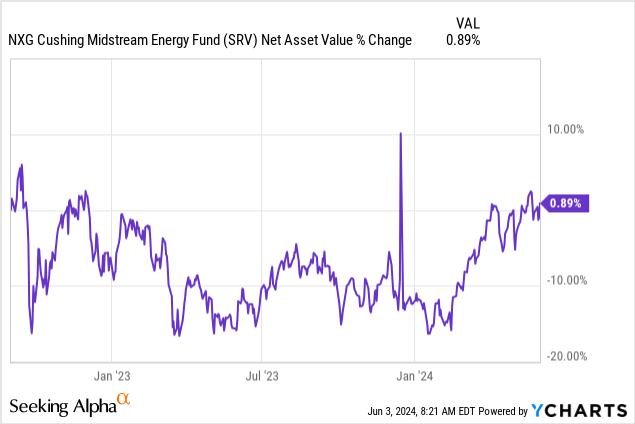

As we saw with its sister fund, NXG Cushing Midstream Energy Fund (SRV), that put this strategy in place earlier, they conducted a rights offering once the fund touched a premium. With an N-2 filing in place for NXG, that could be the next move for that fund should it hit a premium. The fund conducted rights offerings in 2018 and 2019, so there is a history there as well.

Worth noting is that thanks to a strong energy market, SRV hasn’t really seen any erosion of the fund at all at this point in time. With a nearly 13% NAV rate plus the fund’s expenses, one would expect to see a bit of erosion as that’s a rather lofty rate to be able to achieve over the long term. This also includes the fund’s dilutive rights offering that saw a small hit for the NAV as well.

Ycharts

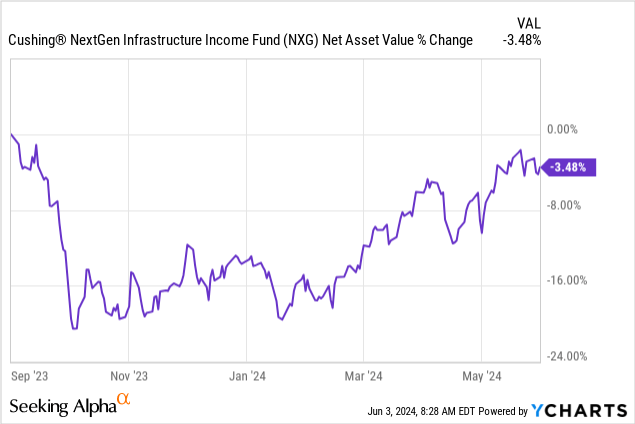

For what it’s worth, NXG has also seen its NAV perform incredibly well through 2024, bringing it back close to where it was when they initially announced the higher distribution. The NAV rate for NXG is higher, though, at 14.59%, which could make it more difficult to maintain NAV.

Ycharts

Conclusion

NXG has seen its discount narrow materially, and that is to be expected when the fund doubles its distribution. While investors could push the fund to a premium, as we saw with SRV, I think it could be time to potentially take some profits off the table. At least, I would be more hesitant to increase my position further to this name at the current levels.

{kind=link}