tumsasedgars

NewtekOne, Inc. (NASDAQ:NEWT) has its fan base. We are not part of it. You can get that straight from our coverage of the stock. Out of the last 8 ratings we have generated for the company, 1 has been a Sell and 7 have been a Hold.

Seeking Alpha

On our last coverage, we pointed out the key risks for the company and decided to stay out.

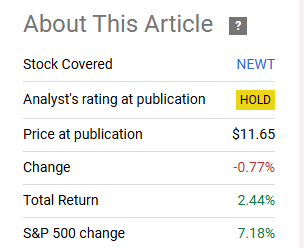

We just see the leverage in the new model as a deal breaker for now, as we have no idea how that will perform in the next downturn. For those that don’t think that is a potential problem, NEWT is certainly cheap at less than 6X estimated earnings and the price decline has also fixed the dividend yield, which is approaching 6.5%. We still rate this a hold.

Source: 6x Earnings With A 6.5% Dividend Yield.

We have not missed out.

Seeking Alpha

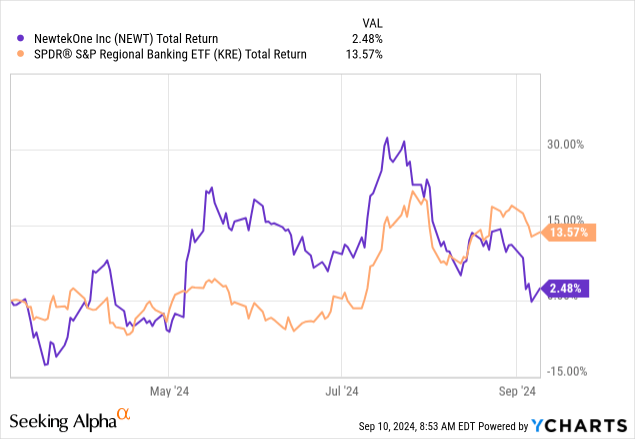

Interestingly enough, NEWT has delivered such a poor performance despite the regional banks being on fire (in a good way). SPDR S&P Regional Banking ETF (KRE) delivered almost twice the return of the S&P 500 (SP500) over this time frame and about six times as much as NEWT.

We go over the Q2 2024 numbers and tell you why we did dive into the secondary securities.

Q2 2024

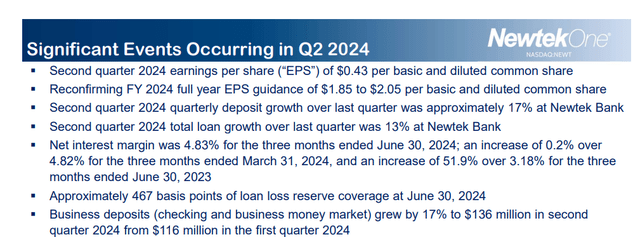

The second quarter was run-of-the-mill at most levels. The earnings came in as expected, and NEWT maintained guidance for the full year at $1.85-$2.05.

NEWTEKONE Presentation

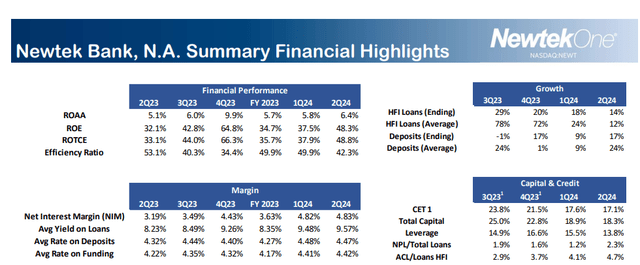

One interesting aspect of NEWT’s earnings is that the net interest margin has stayed fairly steady. Most regional banks are experiencing the opposite, as they are forced to dole out higher payments for CDs and savings account while the long end compression forces their interest payments lower. NEWT’s cost and revenue structure can be seen below, and it has done admirably.

NEWTEKONE Presentation

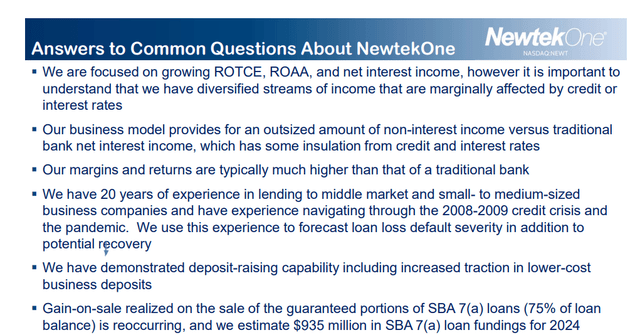

The main reason for this outsized return profile is that its “gain-on-sale” which it mentions below in the last line.

NEWTEKONE Presentation

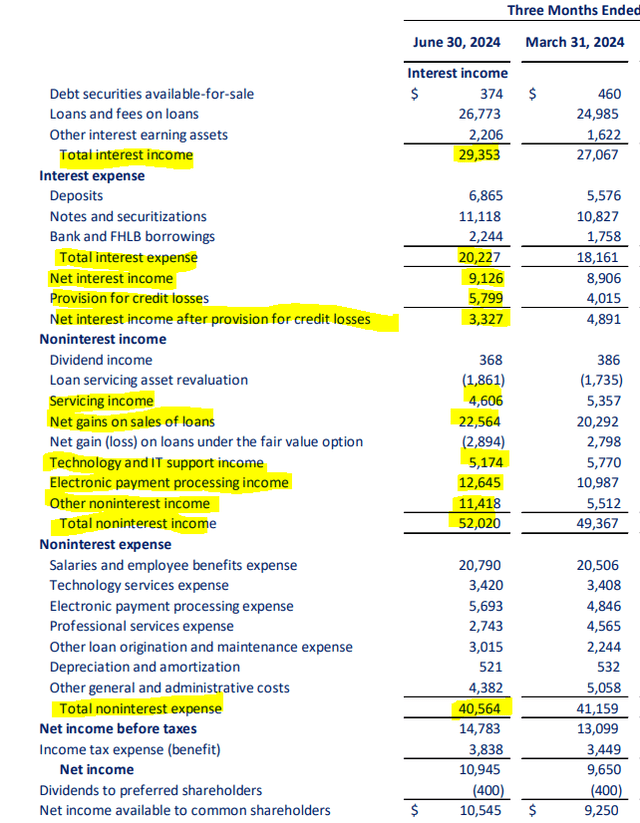

NEWT is correct about the fact that it has hit that realized gain-on-sale target consistently. Even more importantly, it has a few other sticky sources of income. Below, you can see that net interest income, which is the difference in the cost of its funds, is modest after adjusting for loan loss provisions. But there are several areas of noninterest income that should serve the bank well regardless of interest rates.

NEWTEKONE Presentation

One reason we are not too excited about that $52 million quarterly run-rate of other income is that it is not exactly free. There is a lot of noninterest expense that goes along with this. For example, you can note that electronic payment processing income was $12.64 million while the expense side of the same was $5.69 million. If you review quarter over quarter, the revenue expanded at a 15% clip while expenses moved up at 17% for this category. None of this is concerning, but our point is that a lot of work goes towards producing that net income of 43 cents a share.

Valuation & Verdict

NEWT is cheap when you look at the earnings it is generating. Among regional banks, valuations have expanded a good deal as earnings expectations have been lowered for 2025 and stocks have risen. At under 6X earnings and with a 6.5% yield, the only real question is: How big will the bank’s losses be during a recession? There is little visibility into that, as we have not seen this NEWT model perform within a recessionary setting. The bank claims to have a lot of experience from dealing with various tough environments.

NEWTEKONE Presentation

The leverage ratios are also way lower than any other bank. The credit markets seem a little unsure. We say that because despite a BBB+ rating (ok, it is from Egan Jones, the Rodney Dangerfield of rating agencies), it still has to pay a lot on its baby bonds. We remain skeptical, primarily because of the unfortunate decision to end the BDC model. The company had a blank check in place, as it was trading at more than 2.0X NAV at one point. It could expand in various ways with that privilege. Instead, it ended that and destroyed its stock price. We just cannot get over that error and will need to see some evidence of managing a downturn well, before we turn bullish on NewtekOne, Inc. stock.

Baby Bonds

NEWT has a few baby bonds trading on the exchanges. They include,

NewtekOne, Inc. CAL NEWT 28 (NASDAQ:NEWTI).

NewtekOne, Inc. NT 29 (NASDAQ:NEWTG)

NewtekOne, Inc. 5.50% NT 26 (NASDAQ:NEWTZ).

We have the NEWTZ in our bond ladder currently. This is an excellent bond with an 8.5% yield to maturity over the next 1.5 years. We also added NEWTG recently, as it offers a wider spread to risk-free rates than what it should. That one has an 8.5% yield on par and a stripped yield at the current price of close to 8.6%. We see the 10-year Treasury (US10Y) spread of near 5% as quite attractive relative to the risks of this company. In fact, fair value would be close to a 3.5% spread in our view. So this does stand out, but it also goes to show that the market remains jittery on NEWT’s prospects. As we were about to hit the “send” button on this piece, we saw this news pop up.

NEWTEKONE

NEWTH will be the new symbol when listed, and it starts with an 8.625% yield. This is likely to pressure NETWG slightly, and we might switch between these bonds if the pricing is right. All these bonds offer a far higher safety than NEWT common stock and deliver about 2% higher than the yield of the common shares. We still see these bonds as the best way to play the NEWT story through the next recession.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult a professional who knows their objectives and constraints.

Credit: Source link

{kind=link}