P_Wei

Martin Midstream (NASDAQ:MMLP) is currently the focus of two separate non-binding offers. One of the offers is a $3.05 per unit cash offer from Martin Resource Management Corporation, and the other one is a $4.50 per unit cash offer from Nut Tree Capital Management and Caspian Capital.

Martin’s Q2 2024 results were solid, with its adjusted EBITDA slightly exceeding expectations despite a $2+ million negative impact from a couple of accidents.

This reinforces my belief that Martin’s intrinsic value is around $4.35 per unit (based on its projected year-end 2024 net debt), while it may be able to reduce its net debt by $1 per unit in 2025.

Negotiations are still ongoing, but I can envision a plausible scenario where Martin Resource Management Corporation increases its bid to $4.00 to $4.50 per unit and a deal gets done around late 2024 to early 2025.

Current Offers

Nut Tree Capital Management and Caspian Capital increased their offer for Martin Midstream’s common units to $4.50 in cash in July 2024. They previously made a cash offer of $4.00 per unit in June 2024.

Martin Resource Management Corporation (which owns Martin Midstream’s general partner through subsidiaries) made a cash offer of $3.05 per unit back in May 2024. The Q2 2024 earnings call mentioned that negotiations were ongoing between Martin Midstream Partners’ Conflicts Committee and Martin Resource Management Corporation’s advisory firm. However, there was no timeframe about when those negotiations would be completed (while the negotiations could also fall through).

Martin Resource Management Corporation indicated that it was only interested in acquiring all of Martin Midstream’s outstanding common units, and that it was not interested in selling its stake in Martin Midstream or pursuing other strategic alternatives.

Martin Resource Management Corporation effectively owns approximately 26% of Martin Midstream’s common units, including the amount owned by Ruben Martin III.

I am reminded of another example where an MLP was acquired by its general partner. Blueknight Energy Partners received an offer from its general partner Ergon in October 2021 and eventually agreed to an improved offer from its general partner in April 2022, six and a half months later.

A similar timeline would result in some news in December 2024, although each situation is different.

Accident Costs

Martin’s Q2 2024 results took a $2 million hit from a couple of accidents during the quarter. Martin’s marine transportation division had a $0.5 million casualty loss reserve due to a May 2024 bridge allision (an accident involving only one moving object) in Galveston, Texas. In the Galveston incident, a tugboat lost control of a couple of barges and one of Martin’s barges ended up hitting and damaging a bridge. The $0.5 million represents the sum of two related insurance deductibles.

In addition to the $0.5 million casualty loss reserve, Martin’s marine transportation division also saw lower fleet utilization due to the collision.

Martin’s Terminalling and Storage division saw a $1.5 million negative impact from the crude oil spill from the pipeline connecting Martin’s Sandyland Terminal to its Smackover refinery.

The spill was estimated at under 2,500 barrels of oil, and the $1.5 million represents the deductibles under the insurance policies.

Q2 2024 Results

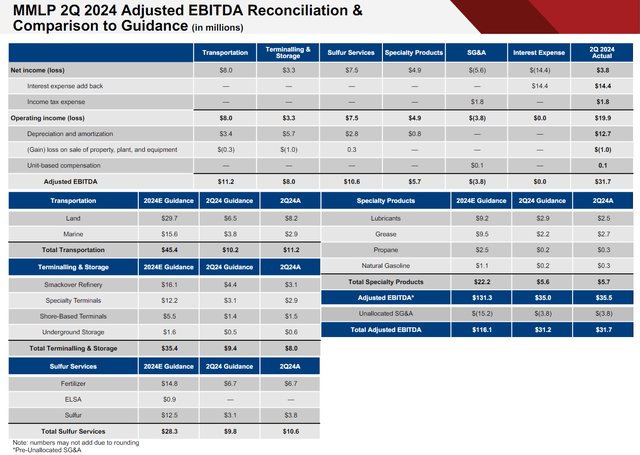

Martin Midstream’s Q2 2024 results were solid as it generated $31.7 million in adjusted EBITDA versus guidance for $31.2 million in adjusted EBITDA. This came despite the $2+ million hit from the accidents.

Martin’s sulfur services division rebounded after some challenges in Q1 2024, while Martin’s land transportation division continued to be strong.

Martin’s marine transportation division missed its EBITDA guidance by $0.9 million, attributable to the $0.5 million in insurance deductibles and business disruptions caused by the accident.

Martin’s Q2 2024 EBITDA (mmlp.com (Q2 2024 Presentation))

Martin’s Terminalling and Storage division’s results were $1.4 million less than its EBITDA guidance, and this can be attributed to the $1.5 million in insurance deductibles related to the oil spill.

Notes On Valuation

I previously estimated Martin’s value at around $4.35 per unit based on an EV to 2025 adjusted EBITDA multiple of 5.0x, along with $425 million in year-end 2024 net debt.

Martin’s business results are generally tracking according to expectations, so that estimated value remains unchanged for now. Martin’s 1H 2024 EBITDA ended up about $0.6 million below its initial guidance, but also was affected by $2.0 million in accident-related charges.

If Martin doesn’t increase its distribution, it appears potentially capable of reducing its net debt by $1 per unit (close to $40 million) in 2025. This would make its value approximately $5.35 based on a similar multiple and $385 million in year-end 2025 net debt.

Assuming that Martin’s business performs as currently expected during the rest of 2024 and 2025, it would likely get more expensive for Martin Resource Management Corporation to mount a future bid if it ends negotiations without a deal.

Given that Nut Tree Capital Management and Caspian Capital’s current $4.50 offer is 48% higher than Martin Resource Management Corporation’s original $3.05 offer, it also seems quite unlikely that the original $3.05 offer could be justifiably accepted.

Since Martin Resource Management Corporation is uninterested in selling its units, alternative offers are unlikely to be accepted unless there was a substantial overpayment involved.

Martin Midstream could potentially be able to justify accepting an offer from Martin Resource Management Corporation that at least matches the first offer from Nut Tree and Caspian Capital.

Thus, I believe there is a good chance that Martin Resource Management Corporation increases its offer and that a deal eventually gets made in the $4.00 to $4.50 per unit range by late 2024 to early 2025.

That would be relatively fair (compared to my estimated value for Martin) and would still allow Martin Resource Management Corporation to get the benefits of the projected increase in free cash flow next year.

Conclusion

Martin Midstream has attracted a competing bid that is now 48% higher than Martin Resource Management Corporation’s original bid. Martin Resource Management Corporation’s close ties to Martin Midstream mean that a competing bid is unlikely to be accepted unless there was a substantial overpayment.

The competing bid does mean that Martin Resource Management Corporation likely needs to increase its bid if it wants to get a deal done. I estimate Martin Midstream’s fair value at around $4.35 per unit based on its projected year-end 2024 net debt, and believe that a $4.00 to $4.50 per unit offer from Martin Resource Management Corporation would be enough to get a deal done.

Credit: Source link

{kind=link}