Joe Raedle

Summary

Readers may find my previous coverage from August via this link. My previous rating was a buy, as I expect LKQ Corporation (NASDAQ:LKQ) to stay resilient throughout this tough macrocycle, supported by a more productive business model relative to the past. I am reiterating my buy rating as I believe the fundamentals of LKQ were not impacted as the 3Q23 headline results suggest.

Financials / Valuation

In the previous week, LKQ released its financial results for the third quarter of 2023, revealing a notable increase in sales by 15% to reach a total of $3.57 billion. The growth observed can be attributed to several factors. Firstly, there was a 300 basis point increase in organic parts and service revenue, accompanied by a 360 basis point favorable foreign exchange tailwind. Additionally, there was a significant contribution of 1,050 basis points from inorganic drivers. Despite experiencing strong revenue growth, the stock price has been significantly affected by the disappointing headline GAAP EBIT margin, which declined by 190 basis points to 8.6%, and the decrease in gross margin by 210 basis points to 39%. The EBITDA margin for the segments experienced a decline, with a decrease of 190 basis points to 11.8%. This decline can be attributed to specific decreases in each segment: a decrease of 240 basis points in the Wholesale – North America segment, a decrease of 200 basis points in the Europe segment, a decrease of 220 basis points in the Specialty segment, and a decrease of 320 basis points in the Self Service segment.

As a result, the management made downward revisions to its guidance, thereby exacerbating the prevailing negative sentiments surrounding the stock. The company revised its projected EPS for fiscal year 2023, adjusting the guidance range to $3.68-$3.82, which is lower than the previously stated range of $3.90-$4.10. Additionally, the diluted EPS attributable to LKQ shareholders was revised to $3.41-$3.55, down from the prior range of $3.65-$3.85. The projected growth in revenue for organic parts and service has also been adjusted to a range of 4.75% to 5.75%, which is lower than the previous estimate of 6% to 7.5%.

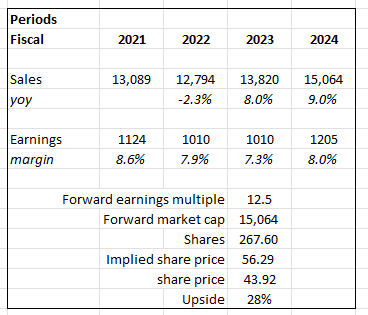

Based on author’s own math

Switching gears to a relative model (previously, I used a DCF model) in order to illustrate the near-term upside, my model suggests a price target of $56. In this revised model, I annualized LKQ 9M23 results to derive my FY23e revenue, followed by a 9% growth in FY24 as I expect business growth to normalize (this is in line with consensus estimates). For earnings, I used management guidance for FY23, which takes into account all the one-off issues that happened in 3Q23 (as I discussed below). That said, margins should revert back to historical levels, as these one-offs should not repeat themselves. It is apparent that the market is focused on the near term, as the 3Q23 results have sent the stock down by more than 15%. Hence, while I am bullish that the fundamentals are sound, I expect valuation to gradually revert back to mean instead of an instant jump. LKQ is currently trading at 10x forward PE, the low end of its historical 10Y trading range, and I modeled it to trade at 12.5x (the mid-point of where it is trading today vs. its historical average of 15x).

Comments

Contrary to what the stock price reflects, I believe the headline results were not indicative of the fundamentals of the LKQ business. Based on my read, the “weak” 3Q23 results and guidance were mainly impacted by one-offs that should not repeat in FY24. Beginning with the fundamentals, it is evident that the North American parts and service sectors experienced a 5.8% organic growth. This growth can be attributed to the attainment of fill rates that approached optimal levels, surpassing 90%. Furthermore, LKQ has observed a rising adoption of its offerings by State Farm. Bears may contend that there is a likelihood of enduring volume headwinds in the foreseeable future. These headwinds can be attributed to various factors, including the decline in used vehicle values and the presence of older fleets, which contribute to an increase in non-repairable cases. Nevertheless, my argument is that the progressively intricate automobile PARC will necessitate a greater number of components per repair. According to the most recent results, it indicates that there exists a record-breaking figure of 15.7 repair components per unit, signifying the highest recorded value to date. Furthermore, the ongoing increase in repair inflation is expected to contribute to the continued acceptance and utilization of recycled parts that are more cost-effective. This trend is advantageous for the LKQ business.

And APU is going North in part because the average number of parts required to repair a vehicle hit an all-time high of 15.7 parts in the third quarter. Source: 3Q23 earnings

Across the Atlantic Ocean, LKQ Europe’s performance was healthy, in my opinion, but the one-time tax impact and strikes have overshadowed this. The occurrence of periodic strikes on distribution centers in Germany, along with a single tax remediation payment received from the Italian subsidiary Rhiag, collectively posed a headwind of 160 basis points on organic growth and 110 basis points on EBITDA. If the aforementioned impacts were disregarded, the European segment would have experienced a 9% increase in organic growth and an 11.3% margin for EBITDA. This would represent an improvement in both metrics compared to the second quarter of 2023. Although it is very likely that the strikes will continue throughout the majority of the fourth quarter of 2023, it is important to acknowledge that they are sporadic in nature and do not result in a complete cessation of operations. I encourage readers to direct their attention towards the notable observation that the growth outlook in the EU aftermarket parts market, which is characterized by significant fragmentation, continues to exhibit strength. Post this one-off, I expect LKQ to return to its historical organic growth of high single-digit percentages and EBITDA margins to remain above 10%.

We knew from a European perspective, we had a fantastic set of platforms, multi-leading businesses, but each of them were running as desperate fragmented platforms than themselves.

However, the majority of the industry is highly fragmented regionally. We’ve provided a few of the larger players on this slide. LKQ investor day

Risk & conclusion

LKQ strategic approach to expanding its presence in the alternative parts market through a rollup strategy presents a moderate level of acquisition risk. This risk stems from the potential challenges associated with identifying and integrating acquired businesses successfully. Failure to execute these acquisitions effectively could result in financial and operational setbacks.

In summary, despite the recent setback in LKQ stock price following the 3Q23 results and guidance, it is important to recognize that these results were influenced by certain one-off factors that are not expected to persist into FY24. Fundamentally, the company’s North American parts and service sectors showed strong organic growth, driven by improved fill rates and increased adoption by key partners. The evolving automobile PARC is likely to demand more components per repair, creating a favorable trend for LKQ’s business. While LKQ Europe faced temporary challenges, primarily due to strikes and a one-time tax impact, the segment exhibited a healthy underlying performance, with significant potential in the EU aftermarket parts market. Once these one-off issues are resolved, the European segment is expected to return to historical growth rates and robust EBITDA margins.

Credit: Source link

{kind=link}