Felix Geringswald/iStock Editorial via Getty Images

Dear readers/followers,

In this article, I’m updating my thesis on the German industrial Knorr-Bremse (OTCPK:KNRRY) (OTCPK:KNBHF), with the native symbol KBX on the German market. This is a low-yield company that has held a very solid upside for some time, and where I have put capital to work for over a year at this point.

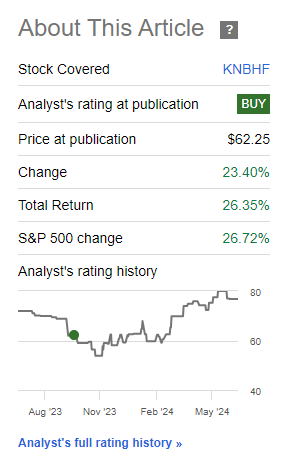

Since my last article, I have bought more and the company is up more than 26% TSR since that time, in this case since September of last year. You can see the total rate of return and how good things have gone for the company and my investment in that article, which you can find here, or see below.

Seeking Alpha Knorr Bremse RoR (Seeking Alpha Knorr Bremse RoR)

Knorr-Bremse is a German industrial company that manufactures braking systems for commercial vehicles and has strong fundamentals. That is one of the main reasons why I have been investing in the business. Despite challenges and headwinds, the company has an order book filled to the brim with good-quality orders, and there’s upside left at the right price.

However, this company is not as great an opportunity or investment as I believe that KION (OTCPK:KIGRY) is, another company I have been writing about. In this article, I will consider changing my recommendation for this business.

Knorr-Bremse – This company has an upside, but now it’s fairly premiumized

I love buying cyclical industries when the market discounts them. This was the case for Knorr-Bremse when I bought the lion’s share of my position. Knorr-Bremse is the world premiere/largest manufacturer of all things braking systems. With over 30,000 employees and over €5B in revenues on an annual basis, Knorr is a company you can “count” on. The company deals in both more common braking systems, but also far more specialized systems for larger assets and vehicles.

The company is A-rated due to a very low debt. Less than 38% long-term debt to capital is what Knorr-Bremse can offer you, aside from a yield that unfortunately is quite conservative at 2.3%, given that you can get better yields risk-free from basically any savings account or quality CD.

In this article, we can start by looking at the 1Q24, which the company reported at the beginning of May. Results were excellent due to the significant profitability increase, and the sort of reversal that I forecasted in my articles on this company.

KGX works in two divisions – and those divisions continued to see very good trends and demand, with an order intake of €2.1B at quarter-end, which means that the order book is now up over €6.6B. Revenue grew by 3.5% YoY, and operating EBIT rose 24% YoY to €238, corresponding to a 12.1% EBIT margin, up over 200 bps year-over-year.

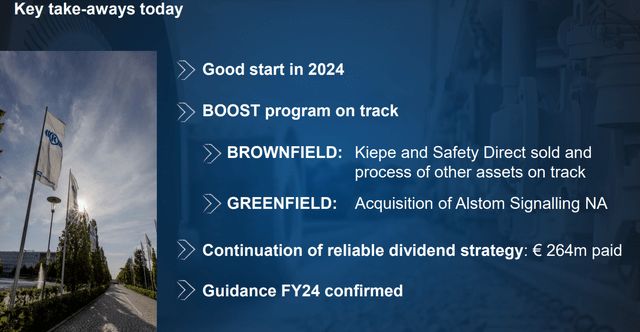

Knorr-Bremse was, as of this quarter, also able to confirm the full-year targets and trends, and the ongoing improvement program under the 2026E BOOST strategy program saw progress, with all initiatives fully on track.

Knorr-Bremse has sold non-core assets in the form of Kiepe Electric and SafetyDirect.

Knorr Bremse IR (Knorr Bremse IR)

While at the same time, the company is acquiring new assets in the form of the Signalling business from Alstom (OTCPK:ALSMY). This underpins the company’s transformative path while increasing and diversifying the company’s mix. I don’t view this as favorable as some investors seem to given that it represents somewhat of a diversification into other business areas – but I can see the company rationale from management.

And, as management specifies, this is a high-moat entry area, which also represents a higher NA revenue share, a solid 16%+ operating margin, and already a 25-30% market share.

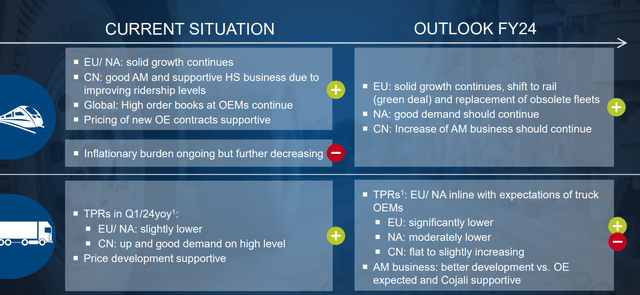

Overall, the macro-level trends for the company here are very positive.

Knorr BRemse IR (Knorr BRemse IR)

Inflation is slowly normalizing, and growth continues. NA is especially solid and positive here, and the ongoing “green deal” of the company should improve things further. FCF improvements are ongoing and Knorr is also optimizing working capital usage with a solid, continuing book to bill at over >1x for over 10 quarters in a row now – or 2.5 years in the RVS segment. The well-filled order book that keeps filling adds to company revenue and profit visibility, and in the CVS segment, the company is improving on the pricing and cost discipline side, leading to a solid set of margin improvements here as well. CVS is now at 11%.

The company has every reason to be happy with the results here – in no small part because the company managed such a good performance during a very difficult macro.

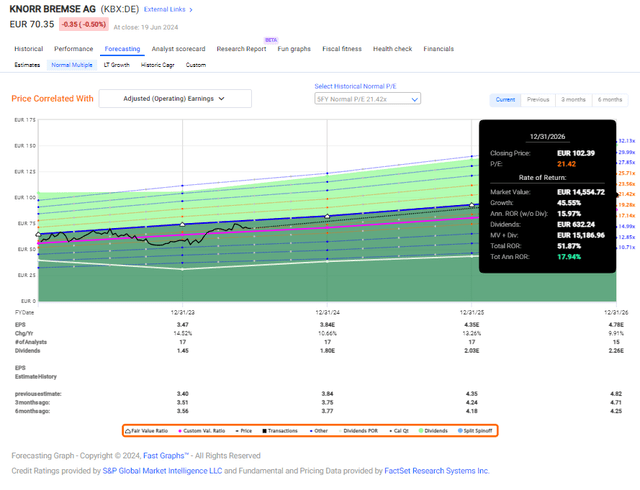

The combination of good efficiency and profitability increases, coupled with volume here, is what makes for a good result. The question of whether this is sustainable is central to the continued, positive thesis for the business, and as things currently stand, this is a forecast that is actually being made. The current expectations from both the company and from analysts are growth rates of 10-13% for both 2025 and 2026E (Paywalled F.A.S.T graphs link), which would go a long way to justify a premium here.

But how high a premium, exactly?

This is the question.

KBX has, as I’ve covered before, been at a lower price than we’re seeing it, even at some of the lows where I covered it in the past. Back in October 2022, when I started establishing my position in the company, I did so at below €50/share for the native share. However, at €70/share we’re still at a level that, based on valuation trends, we could consider being somewhat attractive, and potentially much more attractive than some other companies on the market today.

Still, we’re now 20% higher than we’ve been before- and that will “bite” into the upside appeal.

Risks for Knorr-Bremse at this time are primarily the Alstom deal and similar deals going forward. The company is currently at 5% CAGR on a forward basis, which I based on previous growth rates and the state of the US market being somewhat optimistic. The company also needs to overhaul between 3,500-4,000 stations across the US – by their own numbers. This will hopefully add to aftersales, but the timing on this is not yet clear. This also is related to another main risk – the move into rail signaling/rail overall. The company has stated its clear intention to become a system supplier for the entirety of rail – which is potentially interesting, but also, without a doubt, not risk-neutral.

There’s also the point on company culture, which management addressed on the earnings call.

I think it’s a good question, Vivek, because we have a certain form of reputation when it comes to pricing that we are very stubborn, very stiff. I am afraid to tell you, and especially our clients, this will not change. But what we will change is how communicating we are. That means transparency has to open up also to the externals. It has to be understood what we’re doing, why we’re doing it, and it has to be predictable what we are doing, which was in the past sometimes eventually sometimes a little bit erratic. But we will focus on that so that we are not only a very good player in this area, but we are also an agreeable area in this area.

(Source: Frank Weber, Knorr 1Q24 Earnings Call)

Knorr-Bremse is a very decentralized business for being a German business, but the fact that it’s changing its culture is clearly due to something needing to change – as is the focus on “results-first”, that the company is now enacting.

With that, let’s look at an updated valuation for Knorr-Bremse.

Knorr-Bremse – There’s still an upside here, but it now requires premiumization

Remember, I gave Knorr-Bremse a PT of €100/share. That means I’m not going to shift my recommendation here. The company is still a “BUY”, and my targets and expectations have only changed marginally.

However, this upside is now down from over 25-28% per year to less than 18% per year – all because the valuation has increased. I base my expectation on a 5-year normalized P/E premium of 21.42x, to which you’re seeing the upside here.

Knorr-Bremse Upside F.A.S.T graphs (Knorr-Bremse Upside F.A.S.T graphs)

There’s some risk in forecast accuracy. The company misses around 50% of the time negatively – but the quality here is undeniable – and for the future, the company is still expected to grow at a double-digit rate. For an industrial growing at this rate, I consider a 19-21x P/E to be completely valid here.

The upside you see above is one I see completely likely based on the company’s positive market position, and what growth we’re likely to see in the rail segment, and in overall other sectors and macro. Yes, there is risk – yes, there are plenty of geographies here, some of which can be considered problematic (such as some of NA and some of EU). However, even when just forecasted at 17-18x P/E, the company still delivers.

I believe Knorr-Bremse commands a higher premium, more than we saw in early 2022 of 19-21x P/E. On that basis, this is the upside that we can see, and one I consider actually to be relatively conservative if these earnings materialize.

Some of the best ways of looking at Knorr-Bremse remains looking at the analyst targets and growth estimates, and following those on a quarterly basis. The company had a great 1Q. In the last article, the average target was well below €65/share. Now, the company’s average analyst target is well over €70/share. Slowly, analysts are coming around to this company. 16 analysts now have targets ranging from a low of €50/share up to €90/share. When I started looking at this, some thought this company was worth €35-€40/share. The average here is €75/share, with 8 analysts out of 16 at a “BUY” – the rest at “HOLD”, with only one at “SELL”.

I continue to view Knorr-Bremse as a company with a high potential for outperformance. I remain positive in my conviction of this company, and give you the following thesis for Knorr-Bremse as of June 2024.

Thesis

- Knorr-Bremse is the world’s leading manufacturer of braking systems for railways and with a strong presence in commercial trucking. It has absolutely stellar, A-rated fundamentals with a superb balance sheet and a very well-covered dividend. It’s well-managed, and as of recent earnings, has a very well-filled order book.

- At any cheap valuation below €50-€75/share, this company becomes what I consider to be a “BUY”, even a strong one. The upside for the company is easily in double digits, without estimating too high or too crazy numbers.

- At the current valuation, I still consider Knorr to be a very solid “BUY” and I give the company an overall PT of €100/share based on what I believe to be a normalized fair-value target from growth rates and rocks-solid fundamentals. I believe Knorr is worth at least a forward 21-22x P/E with an EPS growth rate of 11.75% annualized for 2025E – this comes to around €99.78, which I then round to €100/share. It’s high, but the company’s fundamental advantages are high as well -and the recent results confirm this.

Remember, I’m all about:

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has realistic upside based on earnings growth or multiple expansion/reversion.

This means that the company fulfills every single one of my criteria except that it is no longer clearly “cheap”, making it relatively clear why I view it as a “BUY” here.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Credit: Source link

{kind=link}