Marlon Trottmann

Thesis

Jones Lang LaSalle (NYSE:JLL) continues to navigate the commercial real estate headwinds created by rising interest rates and the work-from-home trend. The ECB announced in June the first of its interest rate cuts, and the Federal Reserve is expected to lower rates in the US later in 2024. Signs of recovery in commercial offices are visible with global leasing volumes improving following a 7% YoY increase, while retail and hospitality continue their strong recovery with robust travel demand and increasing wages. I believe the real estate sector’s recovery will spur an increase in funding for new projects, and JLL’s service-based businesses are well positioned to benefit from these new commissions.

Introduction

JLL is one of the global leaders in the commercial real estate business, with 106,000 employees operating in over 80 countries and providing a broad range of services to landlords, investors and tenants, briefly summarized below:

-

Leasing

-

Property Management

-

Facility Management

-

Project and Development Services

-

Investment Management

-

Advisory Services

The real estate industry has been in turmoil for over four years in the wake of the events in 2020; however, as a service business that relies on skilled real estate specialists, headcount has been reduced by less than 3% from record levels set in 2019. Since those reductions, headcount has actually risen by 17%, which I believe highlights their resilience through one of real estate’s most challenging timelines since the 2008/2009 financial crisis. Of course, government financial support minimized the impacts at the time. The growth in headcount indicates their intention to move forward as a stronger business once real estate gets back in favor with investors.

Business Update

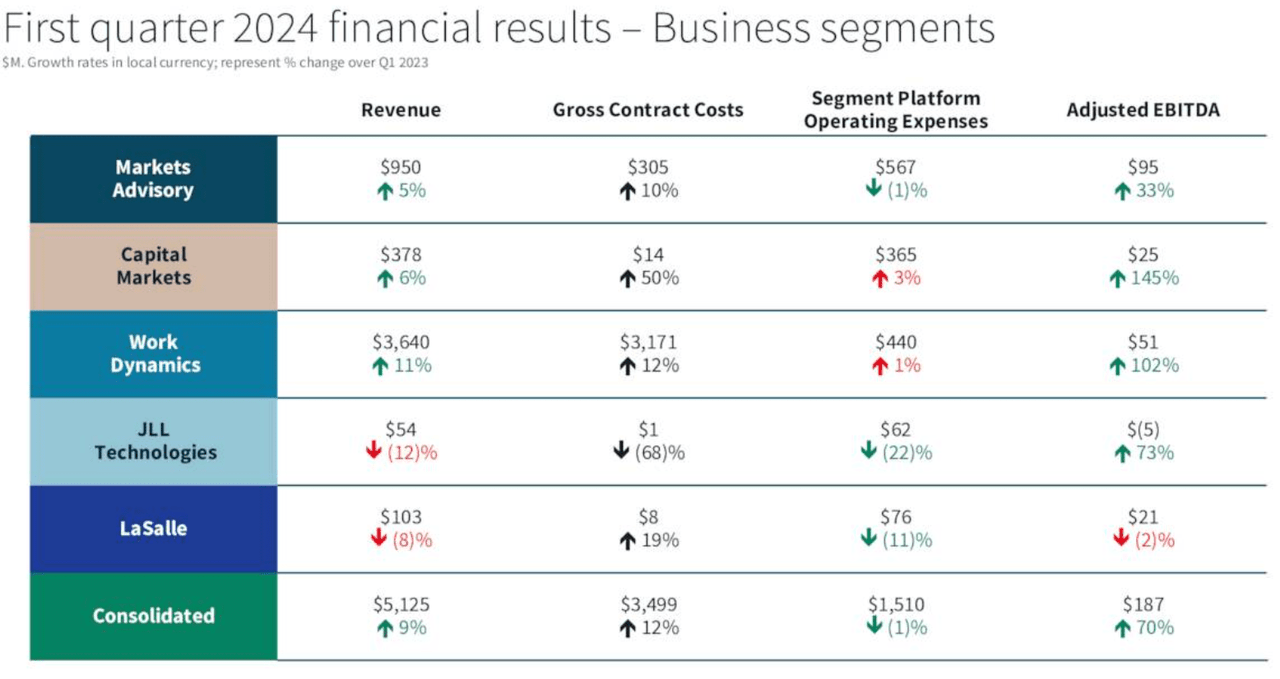

Q1 2024 results showed impressive YoY comparables, with revenues increasing 9% to $5.1 billion and adjusted EPS seeing a significant 150% increase from $0.71 to $1.78. The growth in EPS was primarily a result of higher revenues, capital market transactions and cost reductions across the business. Results were mixed across the business segments; Revenue in Markets Advisory, the group’s second-largest unit, gained 5% YoY, while the Capital Markets business unit grew revenues 6% YoY. Work Dynamics, the group’s largest revenue source, improved revenues by 11% YoY. Additionally, the two smallest business units, JLL Technologies and LaSalle, posted lower revenues of -12% and -11% YoY declines.

JLL Q1 Financial Summary (Q1 Earnings)

Commercial real estate remains a troubled real estate market, with transactions mostly frozen and developments postponed or canceled entirely. Global vacancy increased to 16.5% in Q1 2024, continuing the downward trajectory of occupancy since 2020. The US market remains the most troubled geographic area, primarily as a result of new leases reducing their usable space by 10–15%. This is a clear indicator of the continuing headwinds in the sector, where tenants simply do not require as much space due to many reasons, but in particular the work-from-home employees who no longer require a dedicated workspace.

In Europe and Asia, new leases in commercial real estate have been negatively affected by the lack of modern, energy-efficient, centrally located office space that is served by public transport. Hybrid and remote work options are less available in these markets when compared to the US, which has created a more stable office market with lower vacancy rates; however, the pause in development for new real estate projects has created a backlog of demand for modern, energy-efficient commercial space as businesses strive to provide attractive workspace to encourage employee wellbeing and retention.

JLL’s workplace and property management platforms are tailored to those businesses seeking to be the employer of choice and allow JLL’s team to facilitate upselling of existing clients to improve revenues when few new transactions are taking place. Technology uptake in real estate continues to lag behind most other industries for a variety of reasons, which ultimately stems from a fragmented, mature industry that has seen limited technological development when compared to other industries.

On a brighter note, the Investment Management business unit has been ramping up debt financing deals since the beginning of 2024 with a variety of transactions across the USA, such as:

-

$425 million refinancing of the Miracle Mile Shops in Las Vegas

-

$375 million acquisition financing for a mixed-use campus in San Diego

-

$520 million capitalization for a waterfront mixed-use development in Brooklyn

-

$750 million construction financing for a mixed-use project near Harvard University in Massachusetts

-

$869 million refinancing of a 25-asset national industrial portfolio.

Outlook and Opportunities

As I mentioned above, technology is of great importance to companies in the real estate industry, and through JLL Spark they invest in PropTech as venture capital. Being involved at the VC stage allows JLL to discover those PropTech ideas that may be game-changing for the industry and help differentiate their offerings from competitors. I believe PropTech is one of the most interesting developments in the real estate industry, and although technology adoption is relatively slow, I expect this business unit will be a future driver of growth for JLL.

Moving from technology to financing, JLL was recently honored as the leading commercial and multifamily portfolio debt originator for the 11th consecutive year. With transaction markets somewhat frozen over recent years and traditional lenders hesitant to fund real estate transactions, I believe JLL is well positioned to see growth in the debt origination market as investors return to real estate.

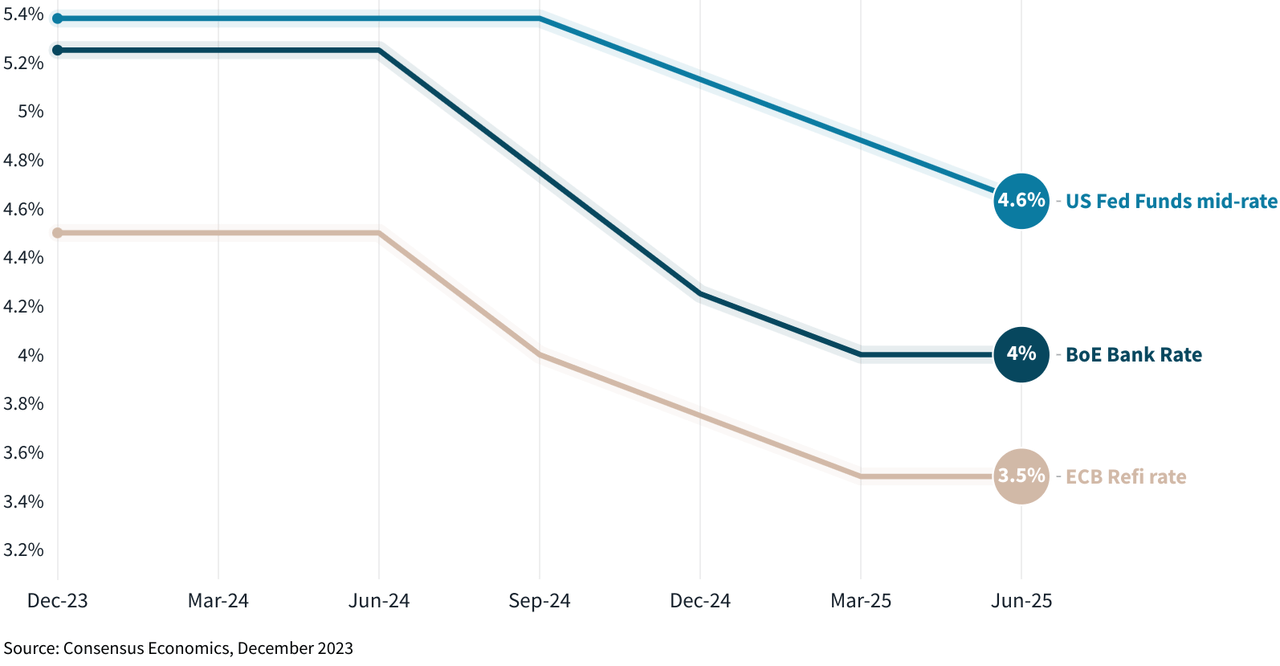

JLL’s dedicated market research team provides quarterly and annual status reports for their key global markets. While each geographic region has specific challenges and opportunities, the critical factor expected to impact each market is interest rates.

In the US, the first-rate cut is expected to occur in October, following the ECB 25 basis point cut in June. The Bank of England was also expected to cut rates in June; however, at this time, no announcement has been made. However, expectation of a cut in June was reduced after recent CPI reports failed to trigger action from the Bank of England. The latest information suggests we may see the BOE lower rates in August.

Interest Rate Forecasts (JLL Global Market Report)

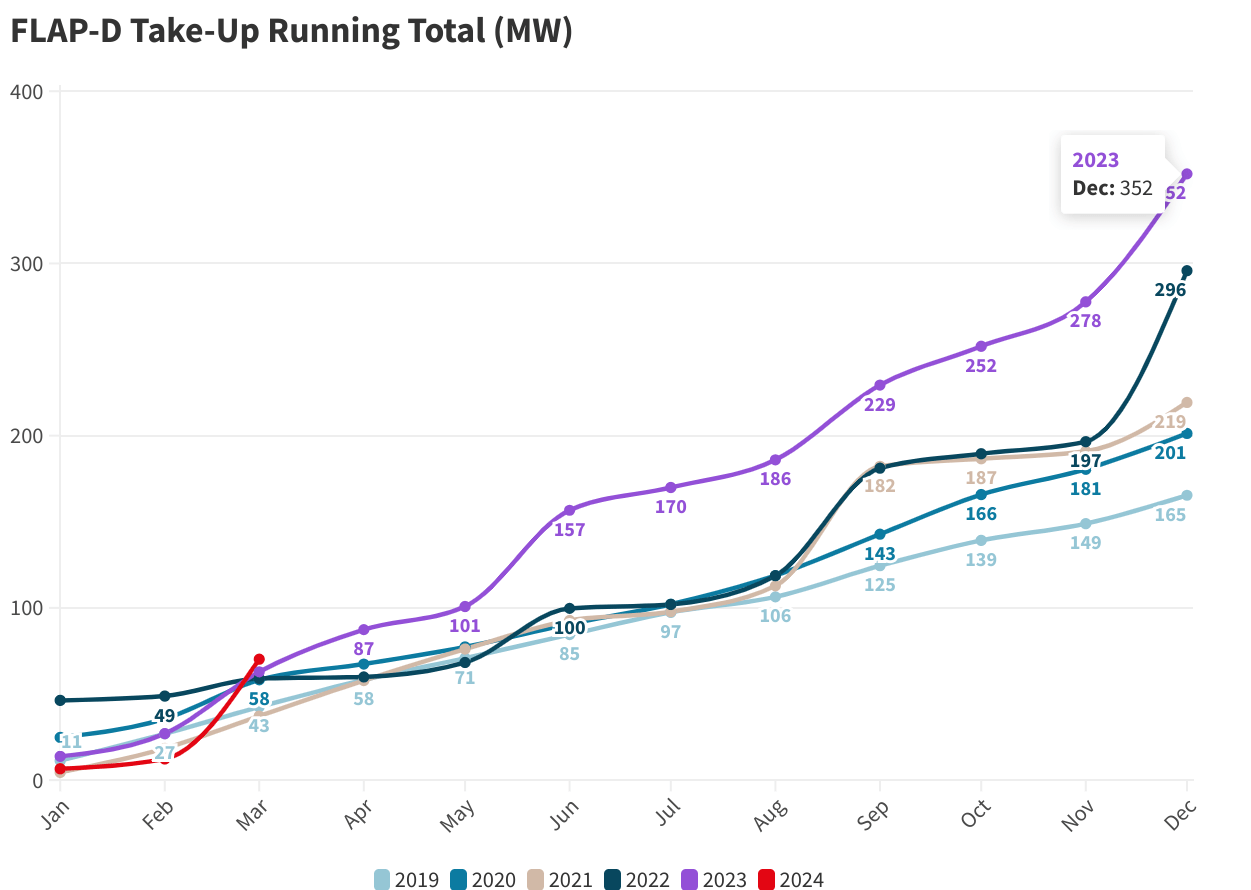

Data centers have become an important sector for JLL, with the development of this sector coming at an important time in the wake of the decline in office development globally. Data center development has been gaining momentum in recent years, particularly in the USA, where Q1 2024 inventory increased 24% YoY. Additionally, Europe has become an increasingly important market, with growth of 20% YoY.

In the data center space, JLL supports their clients in site selection and property management services, meaning they are involved in the project team from project inception and maintain the relationship through the operations period, creating a stable fee-earnings role through property management.

The below chart highlights the impressive surge in the data center development across the major European markets of Frankfurt, London, Amsterdam, Paris, and Dublin. 2024 has started off very strong, with JLL estimating 1,587 MW currently under construction and a further 969 MW in the planning stages in the core European markets, scheduled for delivery over the next three years.

European Data Center Market (JLL EMEA Q1 DC Report)

Competitors

Before I cover the risks to JLL’s business, I think it’s worth commenting on the competition in the real estate space. Real estate has always been a competitive industry, and the professional services offered by JLL are considered to be resilient and profitable areas in the industry, which creates a high level of competition for new work and skilled workers.

The following competitors, along with JLL, form the ‘Big 4’ of Commercial Real Estate. Each business has certain specialty areas, such as project management, financing or pre-construction; however, the majority of services overlap amongst the competition. The largest competitor is CBRE (CBRE), followed by Jones Lang LaSalle, while Cushman & Wakefield (CWK) and Colliers International (CIGI) are significantly smaller, but direct competition nevertheless.

Competitor Overview (Author, Data by Businesses)

Shareholder Returns

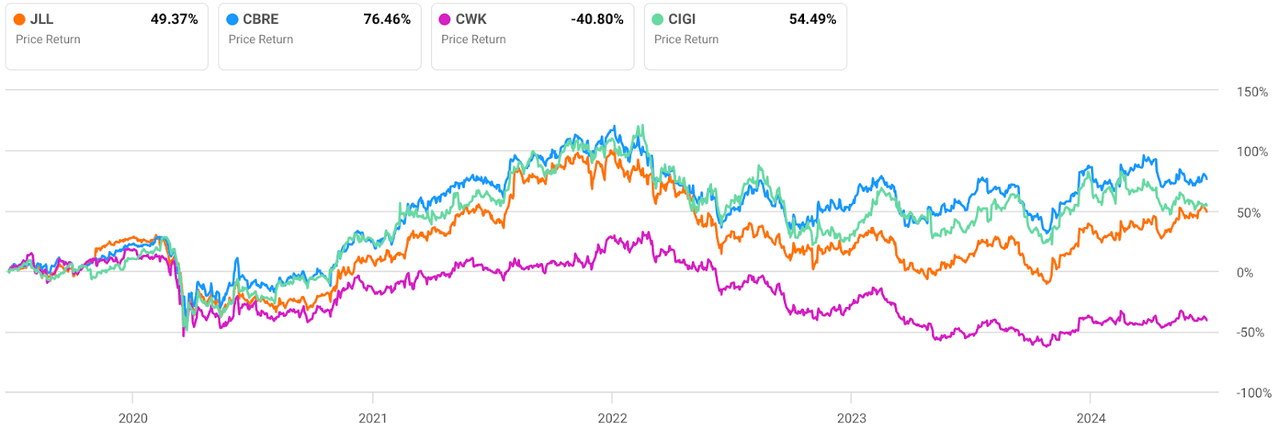

Over the past 5 years, JLL has marginally underperformed its closest competitors, CBRE and Colliers, returning 49% share price growth, while Cushman & Wakefield has underperformed the peer group following a series of negative earnings in recent times.

JLL eliminated the dividend in 2020 in response to the global lockdowns, and to date, it has not been reinstated despite improved free cash flow. At this time, I believe the company is making the correct decision by not distributing a dividend due to the headwinds in commercial real estate and the 1.9x net leverage ratio. However, as rates are expected to decline and earnings are robust, I would expect to see the reinstatement of a small dividend to appease shareholders in the not-too-distant future.

In Q1 2024, share repurchases amounted to a modest $20 million. For the remainder of 2024, repurchases are expected to offset stock-based compensation; therefore, shareholders are not really benefiting from these share repurchases but merely standing in place due to stock awards.

JLL’s Competitor Price Return (SA Charting)

Risks

Geopolitical tensions impact business confidence for investors, slowing investments decisions as well as creating supply chain challenges. JLL is truly a global business operating in 80 countries, which can lead to elevated levels of risk in certain geographic areas as a result of geopolitical issues.

Interest rates remain elevated, causing a slowdown in development and transactions as investors stay on the sidelines. JLL’s own market research suggests the second half of 2024 will be the starting point for a recovery, with declining rates revitalizing investment in the real estate sector back to historic levels.

Technology advancement is slow in the real estate industry. JLL operates its own business unit, offering technology solutions for clients seeking technology solutions, albeit a relatively small contributor to the top line. Competition in PropTech offerings that may better suit the end user could disrupt JLL’s in-house technology unit, meaning continuous innovation will be required and potentially further acquisitions in order to keep up with these advancements. Of course, acquisitions create their own risks for the acquiring company as they seek to integrate external technology into their existing offerings, although JLL has proven they are adept at M&A transactions.

Final Thoughts

In conclusion, I believe there will be a noticeable uptick in activity across the real estate sector later in 2024 and into 2025, following a long quiet period for the industry (excluding industrial and data centers). JLL has navigated these headwinds over the past 4 years and now appears to be in a great position to succeed. Competition is strong, and clients can in some cases change service providers quite easily; however, JLL’s strong Q1 report suggests their resilient revenues are improving, which reinforces their reputation for delivering a high-quality service.

In light of the recovering real estate market and strong growth in sub sectors such as data centers, I believe Jones Lang LaSalle is a Buy for those seeking exposure to the real estate sector and those looking for diversification from capital-intensive physical real estate ownership.

Credit: Source link

{kind=link}