bhofack2

Introduction

J&J Snack Foods Corp (NASDAQ:JJSF) makes snack foods and frozen beverages. Some of its brands include SuperPreztel Soft Pretzels, ICEE frozen pops, Dippin Dots ice cream, Hola Churos, and more. By segment, the company generates about 63% of revenues from Food Service, 14% from Retail Supermarket, and 23% from frozen beverages. In this article, I’ll dive deeper into the recent quarterly results of the company to assess the company’s outlook going forward.

Background

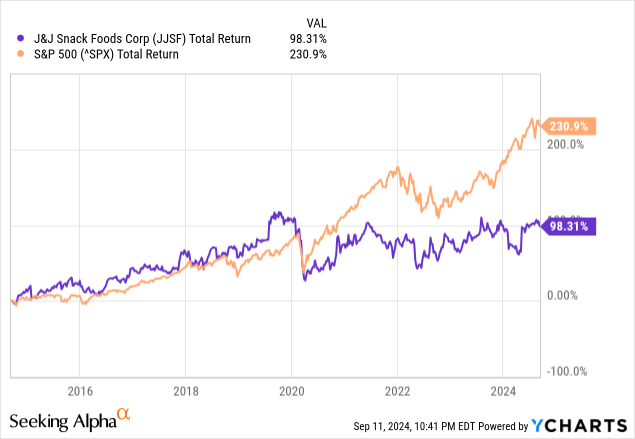

Over the last 20 years, J&J Snack Foods has delivered outstanding returns for shareholders, generating a 966.4% return, excluding dividends. Compounded, this represents a CAGR of 12.5%. However, over the last 10 years, the returns have been less impressive with a total return of 98% compared to the S&P 500’s return of 231%. Annualizing the stock’s return, we derive a CAGR of just 7.1%, indicating that the company’s growth rate has been decelerating in recent years.

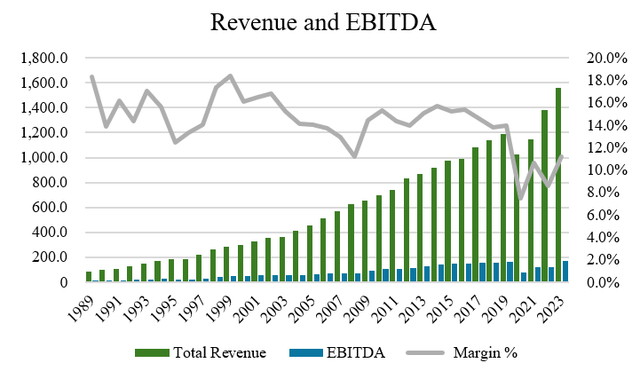

Some of this mediocre (but steady) growth can be explained by looking over at the company’s financial performance over time. Over the last 20 years, the company has compounded revenue and EBITDA at CAGRs of 7.5% and 5.9%, respectively. But over the last decade, the CAGRs have been less impressive at 6.0% and 2.9% CAGRs for revenue and EBITDA, respectively.

Author, based on data from S&P Capital IQ

Q3’24 Results and Outlook

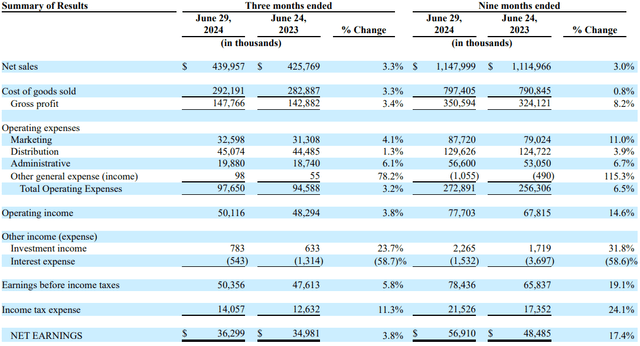

J&J Snack Foods reported its Q3’24 results on August 7 and the results came in slightly worse than expected. During the quarter, revenues came in at $440 million, up 3.3% year over year, missing consensus estimates by $1 million. On EPS, earnings per share of $1.98 missed sellside expectations by a penny. Given the slight miss, shares were down about 2% following the anoucement of the company’s third quarter results.

This quarter was somewhat of a mixed bag for the company. During the quarter, as revenues grew 3.3% year over year, the company’s gross profit grew slightly faster at 3.4%, indicating some gross margin expansion, as operating efficiencies led to a robust margin of 33.6%. Top line growth was mostly driven by good growth in the foodservice and retail segments, which grew 3.7% and 12.4%, respectively. The weak category this quarter was in frozen beverages, which declined 2.6% on a year over year basis. In spite of that, this quarter marked the company’s second highest quarterly net sales performance in the company’s half century history.

Company Filings

The reason I characterize the quarter as a mixed bag is because of some of the challenges the company had to face, as a result of some of the production delays in last year’s actors strike having a negative impact on the films slated for release, particularly in April and May. Why does this matter? Many of the snacks and treats that J&J snack foods produces are made for the theatre and so how box office sales trend has a direct impact on sales growth. As such, sales of frozen beverages, soft pretzels, and churros were weak and management estimates that the total financial impact as a result of the headwinds contributed to a loss of $7 million in sales compared to Q3’23.

Sure, recent results in the theatre category may have been weak. But what about when we look out ahead? As I discussed in a recent article on Cineplex (CGX:CA), there are a whole host of movies slated for release, including Inside Out 2, A Quiet Place, Twisters, Deadpool & Wolverine, and It Ends With Us. On the earnings call, J&J Snack Foods management team noted that they are optimistic about top line growth in these sales channels, noting that the opening of Inside Out 2 in mid-June has already helped to create momentum. With Frozen Beverage sales up 4% month over month, I feel confident in underwriting mid-single growth over the near-term for this category as a strong movie slate rolls out later this year and into 2025.

Moving down the income statement, operating income increased 3.8%, largely as a result of lower growth in total operating expenses (which grew only 3.2%), helped by lower growth on the distribution expense side, the company’s biggest operating expense. This, combined with lower interest expense, which was more than cut in half this quarter as the company’s debt was reduced, led to earnings growth of 3.8%.

Company Filings

As for the outlook for J&J Snack Foods, management is expecting to double its store count with a major grocery retailer under the SuperPretzel and Auntie Anne’s brand sometime in Q4’24. As a strong brand within the portfolio that makes up a meaningful portion of revenues, this has material growth that not only should be lower risk (being rolled out through a retailer) but also enhances the brands’ visbility. For the Dippin’ Dots brand, the company expects to be in 930 locations across AMC, Cinemark, and Marcus Theatres by the end of Q4’24. With a presence in 176 AMC locations, 134 Cinemark locations and 51 Marcus locations, this also represents a near doubling in terms of physical location presence.

My expectation is that this should translate into higher distribution expense over the next few quarters (as the company integrates them), but should be margin accretive going forward. This seems to be a reasonable assumption to make as the average length of a haul has decreased by about 38% with tim performance improving to 82% (from 73% last year). These efficiency gains will be hard to replicate again from a margin perspective, but the company has proven that it can be an efficient operator.

From a balance sheet perspective, J&J Snack Foods looks strong in the sense that its debt has gone down from $55 million just two years ago to having just $12 million in debt today (weighted average cost of 6.3%) against a cash position of $64 million. Liquidity is strong with over $200 million of available room on the company’s revolver. With a stronger financial position, the company is in a better position to pay out dividends, reinvest back into the business, or make opportunistic acquisitions. The last acquisition the company did was for Thinsters, which sells cookies.

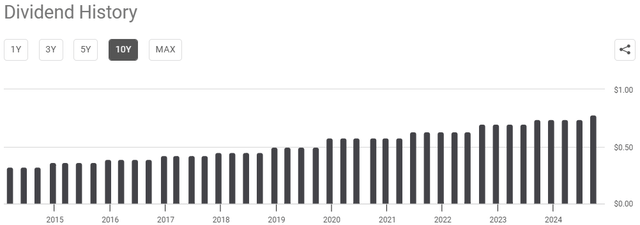

On dividends, with a track record of paying a growing dividend for nearly two decades, the company looks to be in a position to maintain its dividend with a payout ratio of 58%. With growing earnings as a result of some of the investments management has been making into the business, I’d expect the record of dividend growth to continue and so I view the dividend to be safe at these levels.

Seeking Alpha

Valuation and Risks

Based on the 5 sellside analysts who cover J&J Snack Foods’ stock, there are 3 ‘buy’ ratings and 2 ‘hold’ rating. The average price target is $192.25 and from the current price to the average price target one year out, this implies about 19.2% upside not including the 1.8% dividend yield.

While analysts may be bullish on the stock, I believe the stock does not represent good value at $161 per share. As mentioned previously, recent years have shown that the company’s top line growth has slowed down from 7.5% to 6.0% CAGRs in recent years, but that growth is likely to continue decelerating going forward. Consensus estimates for 2024-2026 suggests that the company’s net sales are expected to grow at 1.4%, 3.8%, and 4.1%, respectively, over the period.

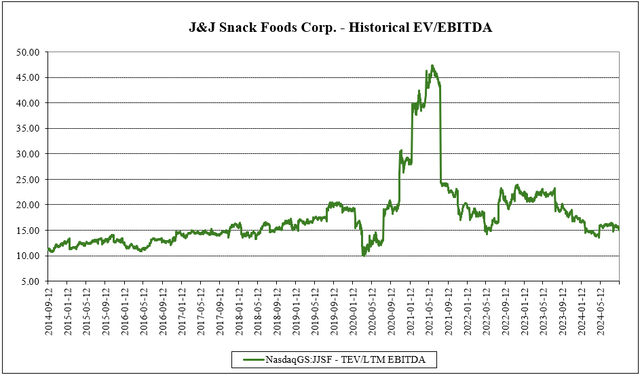

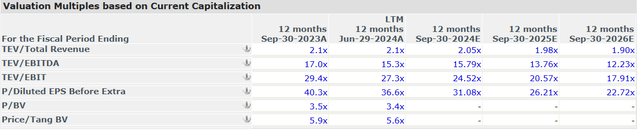

Lower expected growth is fine if that’s what’s being reflected in the share price. However, when looking at the company’s EV/EBITDA multiple of 15.3x, this multiple appears to be above the historical valuation average of 14.4x (excluding the 2020-2023 period when the EV/EBITDA multiple went through the roof as EBITDA was depressed). While a multiple of 15.3x on EV/EBITDA may not appear expensive on an absolute basis, investors should also consider the maintenance capex of running a food and beverage company, something that doesn’t get captured through EBITDA (as capex and depreciation are not including). As such, when using the P/E multiple of 37x or 31x on a forward basis, the valuation on the company can be a hard pill to swallow.

Author, based on data from S&P Capital IQ S&P Capital IQ

Another reason to suggest caution on valuation here is given the heightened risks when it comes to the consumer. For one thing, nearly all Americans are cutting back on their spending in some way, according to a recent CNBC and Morning Consult survey. In that survey, it was found that 92% of Americans are pulling back, further evidence that demand growth in the discretionary categories (like the snack foods that the company sells) could face pressure.

This is also a very tough market to operate in. Brands like Pepsi (PEP), Nestlé (OTCPK:NSRGY), and Mondelez (MDLZ) aren’t sitting back idly and are constantly innovating their product portfolios, backed by strong and durable brands that are even more popular and could be argued to have better pricing power (as evidenced by their margins). I think as a group, these companies could offer better value compared to J&J Snack Foods as they trade at an average P/E of 20.3x and 18.2x on a forward basis, multiples that appear more reasonable when considering that JJSF’s growth profile is unlikely to grow much faster than theirs.

Conclusion

Altogether, J&J Snack Foods has a track record of strong historical performance, but there are signs growth may be slowing down. While the company has announced plans for some of their brands to grow their presence and market share, execution will be key. It’s also not clear whether this growth has potential to accelerate given top line sales CAGRs continuing to trend lower as they decelerate. So while operational execution on margins is strong and efficiencies on margins continue to be generated, the cadence at which this can continue should also be questioned. Moreover, with all of these risks at play, coupled with an elevated valuation that seems to warrant caution, I’d be avoiding shares for now. Closer to the $125 level, with a valuation closer to that of its peers, I’d consider taking another look. In the meantime, I rate shares as a ‘hold’.

Credit: Source link

{kind=link}