J Studios

I have always argued that we should be afraid of what the Federal Reserve is not afraid of. If the Federal Reserve is guarding against something happening, chances are they actually will prevent it. The problem occurs when the Fed is running policy for an objective that ignores the true risk.

The task of the central banker

The job of a central bank is relatively clear, but at the same time, relatively complicated. Central banks are responsible for maintaining the quality and the elasticity of a country’s currency. Central banks wind up being responsible for making sure there is enough money supply growth – and not too much, they are responsible for the adequacy of liquidity, price stability, financial stability, and, in some cases, they also have a responsibility to protect the value of the currency itself beyond simply relative to inflation forces.

In the US we add bank regulation of various sorts to the Fed’s portfolio and for good measure also give the Fed responsibility for achieving maximum sustainable employment. These two added charges are huge add-ons compared to an already complicated mandate for a central bank.

ECB cuts rates

On September 12th, the European Central Bank decided to engage another interest rate reduction and did so with both its headline inflation rate and its core inflation rate running at a pace in excess of its target and growing excessively since at least mid-2021. In addition, each of these price measures is engaged in a currently accelerating profile. The ECB did not cut rates because of inflation, rather in spite of it.

Return of the twilight zone – This is a choice that central banks would not have made in past years. Paul Volcker would not have cut rates under these circumstances. I doubt that Alan Greenspan would have either. But now we’re in a different regime, and it’s also true that central banks may see different risks than they had seen in previous regimes. When Volcker was the Fed Chair, inflation had been howling out of control for more than a decade. When Alan Greenspan became Fed Chair, inflation was still elevated, but Volcker had tamed the worst of it. Both these central bankers came in fighting a legacy of high inflation of different degrees. Central bankers today have had a different experience.

Since the Great Recession, the new experience has been the fear of deflation and the presence of the zero bound. Deflation refers to prices falling, and their ‘zero-bound’ refers to the impossibility or at least extreme difficulty in moving interest rates below zero.

Different strokes for different folks – Because of the change in circumstances, central banks have been making different policy choices. However, it made sense when Volcker was Chairman to raise interest rates and keep them above the rate of inflation when inflation had been running extremely high for over a decade. Still, the Fed did not adopt a policy declaring how it would be more aggressive in the future in the face of inflation. Nor did it signal unwillingness to cut rates if circumstances called for it. The Fed simply wasn’t issuing communications in Volcker’s day. But now, because the Federal Reserve is issuing communications and trying to provide guidance for the future, the Fed has been making policy pronouncements, and offering a background so-called framework statement. That statement, when last was issued, prioritized employment growth and diminished, to some extent, the Federal Reserve’s need to control inflation because it did not see inflation as a threat. At the time that choice seemed foolish to me, but as an older investor/economist I still have not lost my appreciation for the ability of inflation to combust. Meanwhile, the Fed had gone to a bunker mentality over deflation risk.

Bunker mentality creates a new reality – This choice was the result of the fact that inflation had not recently been present and deflation had been present. Deflation risk was most on the minds of policymakers. But economists realize that inflation can come and go and setting a policy directive that is biased towards only deflation, and it doesn’t adequately consider the risk of inflation, would leave policy vulnerable if inflation were to appear. And, of course, inflation did appear, and we were vulnerable. The Fed made the wrong choices, and we wound up with a slug of inflation.

Post bubble, but still pressure – Now that that inflation bubble has largely passed. Inflation has settled back down to a more even keel, but still, it’s above the Fed’s targets. And, despite the fact that the Federal Reserve has had inflation over the top of its target for over 40-months running, the Fed is still planning to cut interest rates. The ECB on September 12th cut interest rates with both its headline and its core rates running hotter than the target and with both of those inflation rates accelerating. The excuse is that they’re concerned about economic weakness. Note that policy is no longer preemptive in fighting inflation; it is preemptive in warding off economic weakness. That is a 180-degree shift from the Volcker-Greenspan era.

Has inflation targeting been coopted by central banks?

I blame a lot of this policy change on the existence of inflation targeting. Having an inflation target seems to give the central banks flexibility because the Federal Reserve, for example, can declare fealty to its target while at the same time it is bending policy to a different task. The central bank can claim to intend to reach that inflation target by promising to hit it eventually. Before there were policy targets, Federal Reserve policy would be vetted according to what the inflation rate was and how the central bank was reacting to inflation. Now the central bank has gained another degree of freedom with the ability to declare its fealty with a 2% target and yet not tell us when it intends to reach that target. This creates a situation where the Federal Reserve can use its credibility to point policy toward stimulating the economy even in an environment where inflation is excessive by promising that it isn’t taking its eye off the ball, and it will get inflation back down to its target of 2%. This has definitely become the land where you have your cake and eat it too.

The credibility blind-spot – The problem with this is that central banks always seem to view themselves as being credible, as having credibility. They rarely recognize when they’ve stepped over the line and their credibility is eroding. Fed Chair Powell constantly characterizes his policy moves as aimed at the dual mandate of maximum employment and the 2% inflation target when he announces his policy choices. He often elaborates that the Fed is trying to achieve a soft-landing, but all that does is to complicate things, since the term ‘soft landing’ has to do almost entirely with growth and employment and, as you can tell, the name doesn’t address anything about inflation. Soft-landings essentially neglect what happens to inflation and that’s why, historically, soft-landings (or anytime that the Fed has tried to spare the economy by not being as tough with interest rates) become associated with higher inflation afterward.

Bernanke and Inflation Targeting – Bernanke’s view of inflation targeting was adopted in January 2012. The Fed would declare an inflation target and then, since the Fed had credibility and the ability to reach this target, the market would join the Fed and everything in the economy would be geared toward the expectation of achieving 2% inflation in the future. There was nothing mechanical about how this would be done; there was no promise to target monetary aggregates; there was no mention of what real interest rates would have to be; and, of course, the Fed has no say over fiscal policy. This whole thing occurs by the magic of expectations and the belief that the Fed would do what it needed to do, an expression that would usually refer to adjusting interest rates in order to achieve the goal.

The Paradigm Dims – However, what Bernanke’s paradigm left out, was what would happen if the Fed came into a period when it lost its credibility, when it did not achieve its inflation target, and when markets would begin to be skeptical. Credibility lost is paradise lost in this world. The whole idea behind the Fed announcing a target is having the markets go along with it. It is essential that markets believe that the Fed is committed to do that. And that commitment means that the Fed knows what it needs to do and that the Fed will have the desire to do it. But when the Fed has demonstrated that it either did not have the technical knowledge or it did not have the backbone to enforce its target, how does the Fed recover and convince the markets that it is getting back on the straight and narrow path? How does it convince markets they can once again pull along with the Fed toward the 2% goal that the Fed abandoned temporarily? How is credibility reestablished?

The need to be tougher, not easier – This is a good question because it implies after the Fed has missed its inflation targets significantly it may be difficult to get the market on board which is another way to say that monetary policy may have to, for a period, keep real interest rates higher than they would have otherwise been – and for longer, in order to convince markets that it’s serious about reaching its inflation target after having missed it. But the Fed has used ‘higher-for-longer’ as a strategy to pursue a soft-policy option, to achieve a soft-landing. ‘Higher for longer’ is a clever misnomer since the policy was to let rates peak ‘less-high’ not higher. But then to get rates ‘high enough’ then keep at that level for longer. And we are still there. And inflation is no longer falling.

An inflation target as moral hazard? Another aspect of this is that with an inflation target, the central bank may actually feel that it can express fealty to this target and gain flexibility in making policy. By simply announcing and repeating that it is still committed to its target, the Fed doesn’t really have to do anything because sheer credibility will bring the markets along for the ride to focus on that 2% expectation. But this could turn out to be a complete miscalculation by the central bank. If the Fed tries to do this in a period after it lost credibility, using verbal assurances that contrast to actions may not work at all.

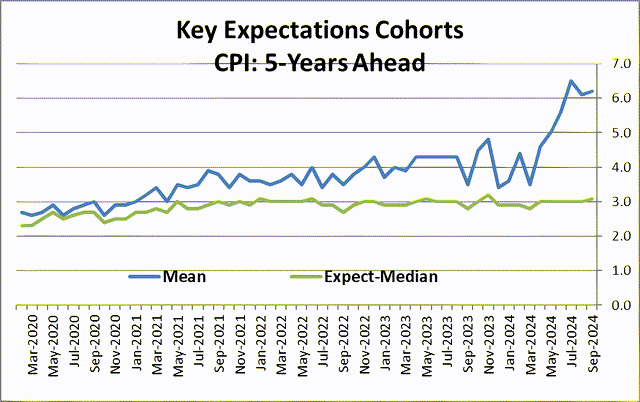

mean inflation expectations are very high (Haver Analytics, FAO Economics)

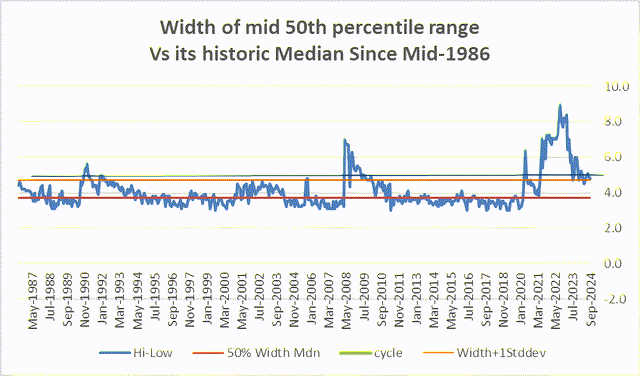

Fed policy is ‘good’ because expectations are anchored? Currently, we’re in a period where the Fed continues to repeat that inflation expectations are anchored, however, in the University of Michigan survey, while the median expectation remains anchored at 3.1% (September), the average or mean expectation has risen extremely high it’s over 5% (6.2% to be precise) and it resides at a level so high that only 25% of the estimates for inflation in the future are about as high as the mean expectation. Of course, there’s nothing in economics that says that the relevant expectation for the future is the mean or the median or anything else. And, in fact, when we look at a survey we find that expectations are widely different. Fully 25% of the expectations are over two-full percentage points higher than the median. It’s pretty hard to think that it makes sense for the Fed to talk about inflation expectations being anchored – maybe confined to the harbor, but clearly free-floating in a broad swath. Currently, in fact, the range that contains the middle 50% of all inflation expectations is historically wide, yet another indication that inflation expectations are, in fact, not anchored at all.

Wide band for 50% of expectations (Haver Analytics, FAO Economics)

Despite all this, the Federal Reserve wants to go ahead and begin cutting interest rates although, even now, inflation is running over the top of its target. The Fed thinks that interest rates are too high And they need to be brought down. By various measures, the economy has slowed, certainly job growth has slowed quite a lot, but it still appears to be adequate to keep the unemployment rate roughly stable around its current level, which seems to be around what most economists think of as full employment.

The cost of rate cuts

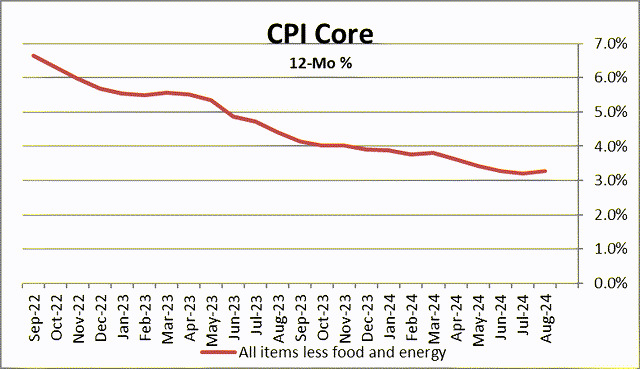

Looking at inflation, the change in inflation has pretty much come to a standstill so that with real interest rates ‘as high as they are’ inflation isn’t falling anymore and inflation is already over the top of the fed’s target… So, the question the Fed needs to ask itself is, given those circumstances, why would it cut rates? Why cut at all, let alone have a controversy over whether it should cut by 50bp? Economic growth may be slower, but it doesn’t look like it’s threatened in any way. And yet, the inflation rate, which is objectively ‘too-high’ is not falling! By reducing the interest rate, the real interest rate is going to fall and that should stimulate the economy more and cause inflation to be higher (or fall by less or fall more slowly).

no longer falling (Haver Analytics and FAO Economics)

The peril of the inflation target: Simply put, this seems like the completely wrong policy to be running in the economy at this time. And I’m prepared to argue that the adoption of inflation targeting has had a lot to do with this and that central bankers have simply found a way to abuse it, a way that Bernanke never really anticipated. He always expected that central bankers would ‘do what they needed to do’ to achieve the target rather than to create policy slack for themselves to acquire greater discretion to cut interest rates with inflation running hotter than the target prescribed using an endorsement of the ‘target rate’ to give their credibility cover. The point of inflation targeting is to reduce discretion and to keep policy in a narrower corridor so it does not stray.

The wrong battle at the wrong time – So… this is what I’m concerned about: We see the ECB making policy in this way; we see the Federal Reserve preparing to make policy in this way. Central banks are being run by a different group of people than the group of which I am a member. I joined the Federal Reserve in 1977, working at the Federal Reserve Bank of New York, at a time that inflation was high, and the central bank was just about to do what it needed to do to regain its credibility. Today’s central bankers have more fear of deflation and of ‘the lower bound’ because they have seen those conditions and experienced their bite as well as the fears they engendered. Even though the current risk on their doorstep is inflation, and inflation is running too hot, this is not the risk that they fear, and so this is not the risk that they are fighting. And that makes this risk more dangerous

Danger! Danger! – That’s my warning: to be wary of, and afraid of, what the Fed is not wary or afraid of. Right now, that’s inflation. The Fed thinks that inflation expectations are anchored when they clearly are not. The Fed probably thinks it has a lot more credibility than the markets really attribute to it. The Fed is confused by this because the markets want the Fed to do what it is planning to do: cut rates! Just because markets are willing to jump up and down and demand interest rate reductions doesn’t mean they think it’s good policy. It just means they think it’s a policy that could be implemented where they could make money! Cha-ching! If it turns out to create inflation and the Fed has to raise interest rates later, well, they’ll make money shorting the market and selling stocks later on. It’s very dangerous to look at what markets are doing and to make arguments about what it means markets are thinking. Because markets are mostly priced for very short-term events. Meanwhile, inflation expectations – broadly considered – show a significant cohort of investors with some real concerns. It’s the Federal Reserve that needs to have a broader perspective, and right now, the Fed seems to have lost its ability to think very deeply into the future and that’s a terrific risk. And all this ‘thinking’ is 100% contaminated by the political risk. Be sure to ‘vet’ all these conclusions on what policy ‘should do’ with a very open mind, well aware of the collateral issues. We may call the election period ‘the silly season’ but the decision made in this critical period can also have deadly consequences for later.

Credit: Source link

{kind=link}