AzmanJaka/E+ via Getty Images

Investment Thesis – Insulet’s Rise & Sudden Fall Explained

A couple of weeks ago, I shared a note with Seeking Alpha readers on Tandem Diabetes Care (TNDM), a maker of insulin pumps for use alongside integrated continuous glucose monitoring devices.

Tandem’s stock price had been reduced to ~$15 per share in November 2023, having traded at >$150 per share in December 2021, after a series of missed earnings targets, and overblown fears around the negative impact of new GLP-1 agonist weight loss and Type 2 diabetes (“T2D”) drugs, such as Eli Lilly’s (LLY) Zepbound / Mounjaro, and Novo Nordisk’s (NVO) Wegovy / Ozempic, on the addressable market size of the iCGM industry.

In 2024, however, Tandem’s share price has risen by >60%, as the company forecast for revenues of $868mm in 2024, and a breakeven adjusted EBITDA margin (across the first 6 months of the year).

Tandem’s two biggest rivals in the insulin pump space are Medtronic (MDT), the medical device giant, and its subsidiary MiniMed, and Insulet Corporation (NASDAQ:PODD), the subject of this post, which markets and sells its Omnipod range of products – continuous insulin delivery systems for people with insulin-dependent diabetes.

While Tandem stock had a year to forget in 2022 with shares slipping from ~$150 to ~$35 in that year, in Insulet’s case, it was 2023 that brought with it a harrowing bear market.

Insulet, which has been a listed company since 2007, after issuing ~6.7m shares priced at ~$15 per share, raising ~$100m, achieved its all-time high share price of ~$330 at the end of May 2023, after reporting revenues of $1.3bn in 2022, up from $1.1bn in the prior year, and an operating income of $95m, with net income of $4.6m. Guidance for 2023 was for revenue growth of 14% – 19%, with an operating margin of “high single digits”.

Fears around the impact of GLP-1 drugs seemingly gave Wall Street the jitters, however, because by September 2023, Insulet’s stock price had fallen to a four-year low of ~$130 per share, down a staggering 60% in just four months.

Did The Market Misinterpret The Impact Of The GLP-1 “Revolution”?

At the end of May this year, analysts at Goldman Sachs forecast that the obesity drug market would reach $130bn in annual revenues by 2030, with Eli Lilly and Novo Nordisk controlling most of the market. That suggests that Zepbound and Wegovy will likely become two of the best-selling drugs of all-time, but does that mean the iCGM market will be negatively affected?

In 2023, Insulet delivered $1.7bn of revenues, operating income of $236m, and a net income of $206.3m, up from $4.6m in the prior year. The company had an excellent year performance-wise, but ended the year with its stock priced at $200, down ~40% from its May highs.

The stock price staged a recovery in August, when Insulet’s CEO James Hollingshead made a purchase of $1m worth of shares at $181 per share, but was soon falling again when research published in the New England Journal of Medicine (“NEJM”) suggested that the use GLP-1 agonist drugs by Type 1 diabetics – the core population for iCGMs – may reduce or even eliminate the need for insulin injections.

A month after that, analysts at Piper suggested they felt that GLP-1 drugs would have “virtually no impact” on the iCGM market, and that the selloff of companies such as Tandem, Insulet, and Dexcom, which makes iCGMs, was overblown.

There is clearly disagreement on the nature of the relationship between GLP-1 drugs and iCGM devices and insulin pumps, but in the here and now, it would be fair to say the iCGM and insulin pump industries are thriving.

In Q1 2024, Insulet reported revenues of $442m, up ~23% year-on-year, with net income of $51.5m, or $0.73 per share. Guidance for 2024 is for revenue growth of 14% – 18%, with operating margin of ~13.5%.

Meanwhile, Dexcom, maker of the popular G7 iCGM, is forecasting for 2024 revenues of $4.2bn – $4.35bn, up from the $3.62bn earned in 2023. Abbott Laboratories’ (ABT) Freestyle Libre device earned $1.5bn of revenues in Q1 2024, up 22.4% year-on-year, while Medtronic has reported “high-forties growth in US insulin pump sales with continued sequential increases in customer base.”

Insulet is certainly not shying away from the GLP-1 debate, either – speaking on the Q1 2024 earnings call with analysts, CEO Hollingshead commented:

we continue to analyze the market impact of GLP-1 use. Analysis of actual claims data demonstrates that GLP-1 use accelerates the adoption of insulin among people living with type 2 diabetes. The data are definitive and striking and strengthen our conviction in the size of the unmet need and the size of the business opportunity for our growing type 2 portfolio. We are finalizing our analysis and look forward to providing a more detailed update soon.

In summary, far from being a hindrance, Insulet is claiming the data it is seeing suggests use of GLP-1 drugs is increasing, not decreasing insulin pump use.

Looking Ahead – Does Insulet Stock Remain Undervalued As We Look Beyond 2024?

Clearly, this is the question that most investors would like to know the answer to, and there are useful metrics we can apply to try to answer this question.

Let’s consider first the forecast operating margin of 13.5% on revenues up ~16.5% year-on-year (at the midpoint of guidance), which equates to revenues of ~$1.98bn. That gives us operating income of ~$267m, and last year, interest and other expenses came to ~$30m, so if we subtract a similar sum, we can estimate net income in 2024 of ~$235m.

Insulet’s market cap valuation today is $13.5bn – 69.4m shares multiplied by $193 – giving the company a forward price to earnings ratio of ~57x. It’s a high figure that does not emit clear buy signals (as a figure in the low single digits might, for example), unless the market is anticipating explosive revenue growth and paying a premium for stock as a result.

I mentioned that the industry is thriving at present, which is borne by the growing revenue numbers, but equally, it is competitive.

Consider the fact that Tandem, for example, is forecasting for revenues of ~$860m in 2024 – almost half the figure Insulet is guiding for – yet Tandem’s market cap valuation (at the time of writing) is $3.1bn – 4x smaller than Insulet’s. If value for money is your abiding principle as an investor, Tandem appears to be the better horse to back.

Interestingly, however, analyzing its competition in its 2023 annual report / 10K submission, Insulet states:

Our Omnipod platform competes for consumers in the insulin delivery market. Because most new Omnipod users come from Multiple daily injection (“MDI”) therapy, which currently is the most prevalent method of insulin delivery, we believe that we primarily compete with companies that provide products and supplies for MDI therapy.

We also compete with companies in the insulin pump market, which today consists of tubed pump companies, including Medtronic MiniMed, a division of Medtronic public limited company (“Medtronic”), and Tandem Diabetes Care Inc. (“Tandem”). Medtronic historically has held the majority share of the tubed insulin pump market.

With the GLP-1 agonist weight loss drug market being so new, it is easy to forget that the iCGM / insulin pump market is also still new, and there are still millions of customers to migrate from MDI, to iCGM. This is further backed up by Insulet’s reporting that 85% of new customer starts in Q1 2024 were from MDI.

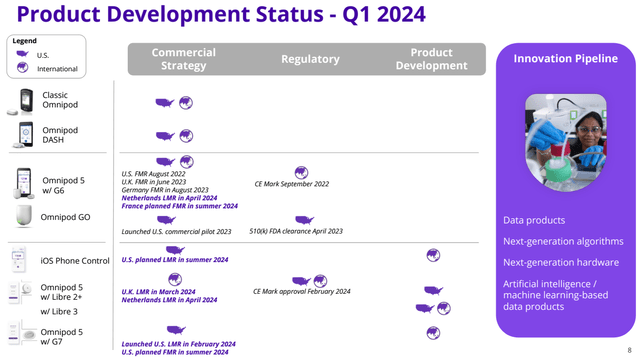

Furthermore, market penetration outside of the US remains low, and as we can see below, Insulet is building up its partnerships and compatibility with the latest iCGM products from Dexcom, Abbott, and with Apple’s (AAPL) iOS operating system.

Insulet product development status (Q1 24 earnings presentation)

Concluding Thoughts – In The Current Environment, Is Insulet Stock A Buy, Sell, Or Hold?

If there is a hierarchy in the treatment of Diabetes patients you could make the case that using GLP-1 drugs to prevent the requirement for insulin injections altogether would be top of the tree, followed by the use of automated, insulin pumps, with MDI being the least favorable option.

The fact MDI is still the most widely used option (in 2021, apparently, CGM and insulin pump market penetration stood at ~30%), plus the fact that GLP-1 drugs cannot yet be relied upon to eliminate a Type 1 diabetics’ requirement for insulin injections, makes a strong case in my view for the continued expansion of the iCGM industry.

As a larger company, the growth opportunity in play for Insulet is arguably less compelling than Tandem’s (although, as the smaller company, the risk of the company failing is higher), but when you consider that Insulet stock is trading at the same value today as it was in 2020, and that revenues in that year were $904m, and net income $6.8m, the support for a “buy” recommendation is strong, in my view.

Insulet trades at a 40% discount to its all-time high valuation, and a price to sales ratio of ~7x. Profitability has been somewhat elusive, but as the technology develops (remember, this is still a relatively new industry), margins may start to increase. Insulet still has millions of customers to convert from MDI i.e. there is still much “low hanging fruit” to pick, and it has received FDA clearance to market its Omnipod 5 device to Type 2 diabetes patients using basal insulin last year, opening up a market of ~20m people in the US alone.

The threat that GLP-1 drugs will “eat iCGMs” lunch is indeed overblown, in my view, and especially so in the medium term, and therefore, although I expect continuing volatility, I expect Insulet stock to continue to stage a recovery in 2024, and would set a 1-year price target of between $250 – $280.

Credit: Source link

{kind=link}