CarmenMurillo/iStock via Getty Images

Investment thesis

Grindr (NYSE:GRND) holds a dominant position in its market and benefits from strong brand awareness among its target audience. Its user base remains largely unmonetized, offering significant potential for future growth through enhanced monetization strategies. The business is growing at over 30%, with adjusted EBITDA margins above 40%. Despite the strong growth expected this year, shares appear to be close to fully valued, while trading at an EV to adjusted EBITDA multiple of 15.5. Furthermore, increased competition as well as execution risks related to its monetization efforts, leads me to a Neutral rating on the shares.

Company overview

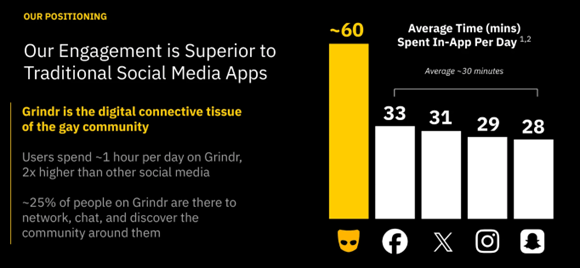

Grindr is a dating and social networking app for the LGBTQ+ community. The company aims to be the global Gayborhood in your pocket, as it plans to expand its offering beyond just casual dating and building long-term relationships. The company’s product stands out from other social media and dating apps, with users spending double the time on its platform daily, as shown below.

Investor presentation

The company enjoys 85% brand awareness, which allows it to grow with almost no spending toward marketing. The company’s current user base remains under-monetized, with a paying user penetration of just 7.4%. Following the appointment of George Arison as CEO in September 2022, the company has undertaken a serious effort to improve monetization through its Grindr XTRA and Grindr Unlimited product offerings. The majority of its revenue comes directly from users subscribing to these products on a monthly or weekly basis. The company also earns a smaller portion of indirect revenue through third-party and brand advertising.

Reasons behind its recent share price appreciation

Introduction of the weekly XTRA subscription

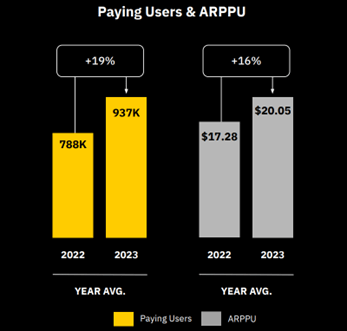

The XTRA Weekly subscription that was launched last year was a home-run product for the company. The addition of this weekly tier to the existing monthly tier appealed more to the immediacy of the user, even though it was priced higher. This was further elaborated by its CEO during the Q1 2024 earnings call when he said:

I think there’s one thing that I’d like to share with everyone, with respect to our usual behavior and that is that our app, offers immediacy to our community. And therefore, the weekly proposition has really followed that intent and major use case. And so we have not found the level of cannibalization that I might have expected, with respect to weekly and monthly.

Investor presentation

This led to a sharp increase in paying users and Average Revenue Per Paying User (ARPPU) of 19% and 16% respectively, as shown above. This trend continued in Q1 2024, with paying users increasing 17% to 1 million, while ARPPU was up 15%. The XTRA weekly product has led to higher margins for the company due to its higher pricing and well as high LTV since management noted that the reactivation rate of the product was high. Most importantly, its existing monthly offering had not seen cannibalization due to the weekly subscription.

Solid growth in indirect revenue

Though indirect revenue represented less than 15% of the total revenue in its recent quarter, it showed substantial year-over-year growth of 43%. The company continues to make strides towards increasing advertising revenue from brands that want to reach its cohort. The introduction of Ad banners last year has also been immensely successful in driving revenue growth.

Adjusted EBITDA margins staying above 40%

Despite an increase in marketing spend as well as an increase in Full Time Employees (FTEs), from 104 last year to 129 at the end of Q1 2024, the company continues to maintain its strong profitability, with an adjusted EBITDA margin of 42% in its recent quarter. Management expects margins to remain north of 40% in upcoming quarters, even as marketing and technology investments increase.

What to expect for the remainder of 2024

Mid-term strategy to be outlined at the Investor Day

The company will host its first-ever Investor Day next week, and I expect the management team to delve deeper into their Gayborhood vision. The company’s Chief Product Officer and Chief Brand Officer are expected to describe their roadmap for how they plan to evolve the current product offering. I also anticipate that the company’s CFO will provide detailed insights into the capital allocation plan for the next three years. This should include how the free cash flow generated by the business will be allocated between debt repayment and shareholder returns.

Impact from new products

The company faces tough comparable quarters this year following the successful launch of the XTRA weekly subscription in the middle of last year. To overcome the potential year-over-year growth deceleration, the company has launched the Unlimited Weekly subscription in February. At double the price of the XTRA Weekly subscription, the Unlimited subscription could potentially be a major contributor to the company’s growth this year.

The company also plans to launch the Right Now and Roam products later this year. The Right now product makes it faster and easier for users that are nearby to connect. The Roam product helps users interact with people in other locations globally and is especially helpful when making travel plans.

Ramp up in marketing spend

Following multiple years of negligible marketing spend, management has recently increased its efforts towards raising brand awareness in the market. The company has enjoyed success in launching its own podcasts with the aim of bringing together the LGBTQ+ community to discuss hot topics. This month the company is promoting the Grindr Bus Tour, which will be visiting 10 cities, and participating in different pride events. Its CEO expects the company to generate significant returns on its marketing spend, as he recently stated:

And so again, that is going to be a reasonable investment but the ROI you’re going to get from that, we believe from the engagement with the user is going to be really, really significant.

Debt concerns diminish as FCF improves

The company has nearly $315 million of debt on its balance sheet, alongside $21 million in cash. This implies a net debt to adjusted EBITDA ratio for this year of roughly 2.3. At the end of last year, the company refinanced its high-cost lending facility with a new $300 million term loan at SOFR+3% together with a $50 million revolving credit facility. This is expected to save the company approximately $17 million in interest costs this year. The lower interest costs should translate to higher FCF conversion from its adjusted EBITDA, and help the company reduce its debt burden.

Valuation

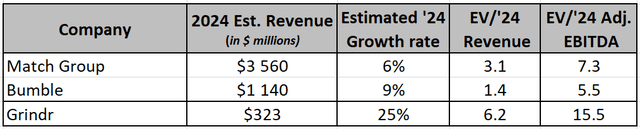

The company continued to perform strongly in Q1 2024 with year-over-year revenue and adjusted EBITDA increasing by 35% and 45%, respectively. Management’s full-year revenue growth and margin guidance points to the company generating $323 million and $130 million in revenue and adjusted EBITDA, respectively. This is in line with analyst expectations, and therefore, I have incorporated these figures into my valuation of the company.

Based on estimates from the companies and Seeking Alpha

As shown in the table above, the company is trading at an EV to Revenue multiple of 6.2 and an EV to adjusted EBITDA multiple of 15.6. Comparable public market peers like Match Group (MTCH) and Bumble (BMBL) are trading at much lower valuations, which is likely justified considering their lower growth rates and profit margins. Nevertheless, Grindr’s valuation appears to be rich, and its forward returns will depend on the company continuing to show strong growth over the coming years through the introduction and successful monetization of new products and features.

Risks

Increased competition

According to me, the biggest risk facing the company is competition from larger players. Match Group in particular provides an offering for the LGBTQ+ community through its core products like Tinder, as well as dedicated products such as Archer. The initial success of Archer, which is an offering for gay men, was specifically touted by the company during its recent earnings call. When specifically asked about Archer, Grindr’s CEO acknowledged that it is common in the dating space for people to use more than one product, but that his company aims to be the predominant player in the market. More specifically regarding the impact from Archer, he added:

As far as Archer specifically, I think there has not been a lot of conversation about that in the community because it hasn’t really taken off. So on that one specifically, we’re not in any way concerned.

Failure to improve monetization

Though its under-monetization provides a future opportunity for the company, there is also the risk that its strategy could prove unsuccessful as its new products risk cannibalizing its existing offerings. Furthermore, ramping up monetization too quickly could potentially lead to less engagement on its platform and the loss of users and revenue for the company. So far, the company has been prudent in their monetization efforts, by rigorously testing and adapting to market feedback.

Valuation multiple compression

Shares are valued at a premium to its peers as investors expect the company to continue to show strong growth in the upcoming years. If the company fails to live up to these growth expectations, future returns could face a significant headwind due to multiple compression.

Conclusion

Despite its attractive growth rates and high profit margins, I believe a Neutral rating is justified at the current valuation owing to the competitive and execution risks involved.

Credit: Source link

{kind=link}