Maksim Safaniuk/iStock Editorial via Getty Images

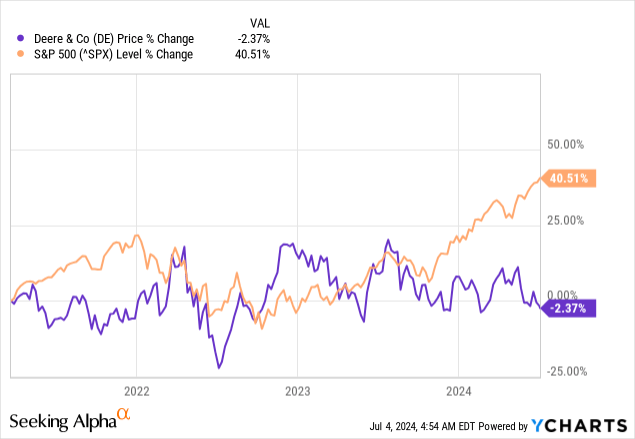

It has been a bit more than 3 years since I first published my bearish thesis on Deere & Company (NYSE:DE) and although the stock did not fall materially over the period, it has been an utter disappointment for shareholders.

Since March of 2021, DE is in a negative territory, while the broader equity market delivered a return in the excess of 40%.

Following this poor performance in recent years, however, Deere’s valuation has been slowly normalizing, which has recently made me reconsider my sell rating on the stock. Having said that, however, it is too early to for a buy rating and there are significant risks lurking ahead for Deere.

Therefore, as the stock slowly approaches buy territory, it is important for existing and potential shareholders to keep a close eye on the deteriorating outlook and look at the valuation through the lens of forward business fundamentals.

Deteriorating Outlook

The risk of a cyclical downturn for Deere is something that I have been covering extensively in my analyses over the years. As the share price reached extreme levels, however, investors seemed to have disregarded all these risks, and they are now paying the price of a stock that is consistently underperforming.

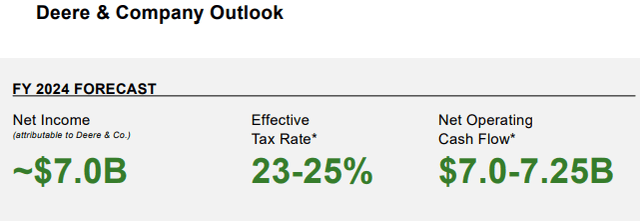

The market was caught off-guard during the last quarter when Deere’s management lowered their outlook for the whole fiscal year 2024. The net income figure for FY 2024 is now expected to be roughly $7bn, down from a range of $7.5bn to £7.75bn provided during the previous quarter.

Deere Investor Presentation

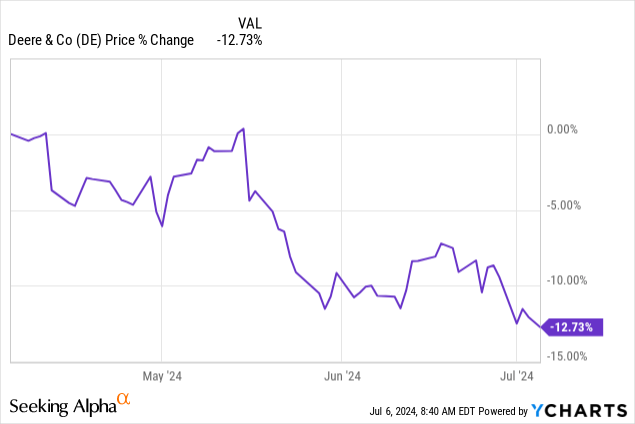

Although this was somehow expected, investors were not prepared and the stock fell sharply since mid-May when the company reported its Q2 2024 results.

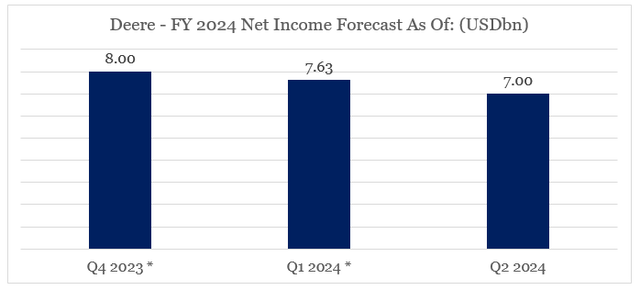

As a matter of fact, this wasn’t the first time when Deere’s management lowered their outlook for FY 2024. The initially provided outlook as of the end of fiscal year 2023 was even higher.

prepared by the author, using data from Quarterly Investor Presentations

* using the mid-point of the provided range

All that speaks volumes for the uncertainty of these very short-term outlooks, as agriculture machinery purchases remain highly cyclical and at the mercy of the highly volatile commodity prices.

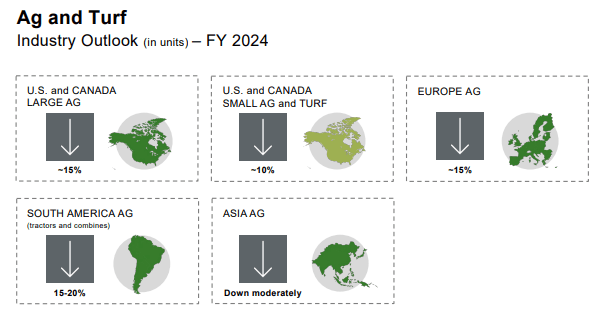

All that is clearly illustrated even by Deere’s broader industry outlook for FY 2024. At the moment, units growth in North America and Europe is expected to be a negative 15% to 10%, depending on the size of the machinery.

Deere Investor Presentation Q2 2024

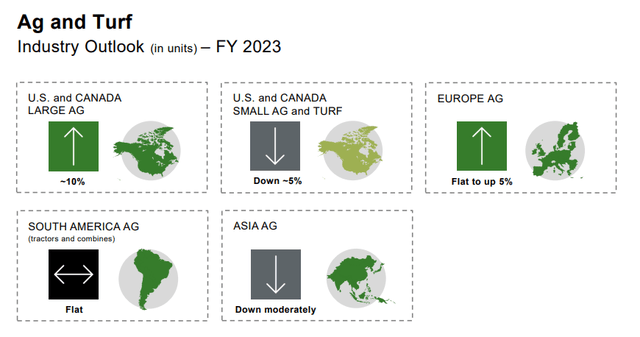

Just a year ago, the same figures for these regions were for growth of between 5% and 10% with small agriculture machinery expected to contract slightly.

Deere Investor Presentation Q2 2023

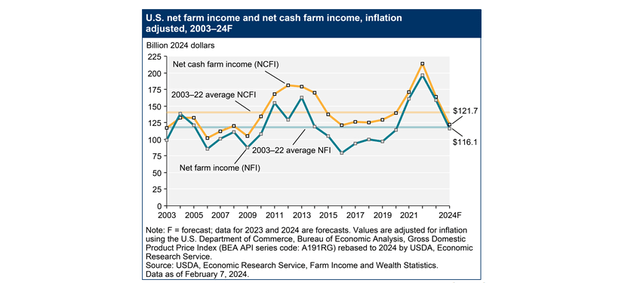

This is something that I have been warning about just as U.S. net farm income was hovering at its cyclical highs a few years ago. As we see from the graph below, the U.S. Department of Agriculture now expects a major contraction in net farm income.

U.S. Department of Agriculture website

The deteriorating industry outlook and business fundamentals would not have been a problem for Deere shareholders, provided that the share price was accurately pricing-in all that and was also providing a margin of safety in an event that the cyclical downturn of the industry would take a turn for the worse. Unfortunately, this is not something that appears to be the case.

How Is Deere Priced?

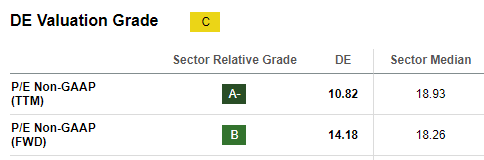

On the surface, it is quite easy to conclude that Deere’s share price is currently very cheap. After all, it is very hard to make a case of the stock being expensive when it trades at 14 times its forward earnings at a time when the P/E ratio for the S&P 500 is approaching 30.

Seeking Alpha

We should not forget, however, that when dealing with a stock in a very cyclical industry; these ratios could be very misleading during cycle peaks and troughs. As a starting point, Deere’s current net income figure is still near the company’s cyclical highs of FY 2023 and there’s plenty of downside left if demand continues to deteriorate.

prepared by the author, using data from Seeking Alpha

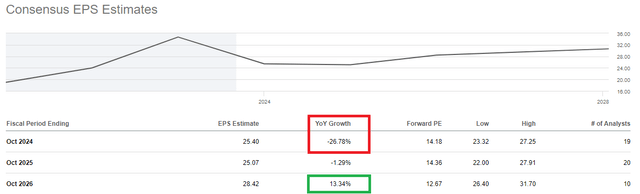

When it comes to forward estimates, earnings are currently expected to fall by nearly 27% in FY 2024, remain relatively flat the following year and return to double-digit growth in FY 2026.

Seeking Alpha

These estimates are quite optimistic, in my view, for a number of reasons. Firstly, the expected drop in FY 2024 is still lower than the one based on Deere’s management’s most recent outlook. The net income figure for FY 2023 stood at $10.2bn and given the outlook of around $7bn we are currently looking and a drop of 31%. Of course, one could explain this difference with various one-off items and analysts publishing their forecasts on a normalized basis. Even if that’s so, we have already seen two consecutive quarters of management lowering their expectations for the rest of the year. That is why, I believe that current analysts’ estimates are not leaving much margin of safety, in case 2024 turns to be worse than expected.

Secondly, the current price targets of sell-side analysts seem to factor in just a 1-year drop in earnings and then a quick recovery in the following years. Once again, this is a very optimistic scenario which is having a profound impact on the final target prices of these analysts.

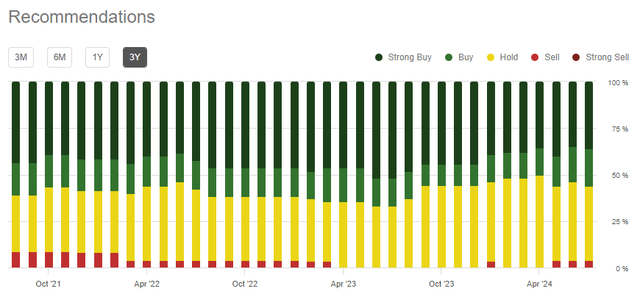

Moreover, as we could see down below, the consensus view on Deere has not changed when it comes to ratings. This creates a risk on its own should the downturn cycle persists for more than a year, and we witness a wave of analysts rushing to downgrade the stock.

Seeking Alpha

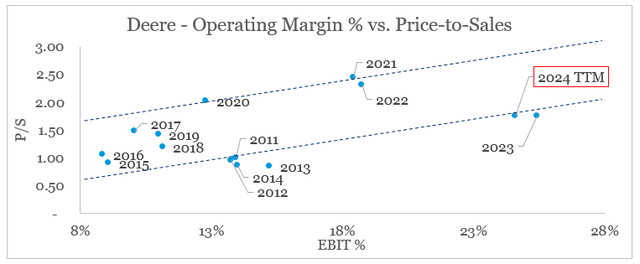

By comparing Deere’s operating margin to the stock’s price/sales ratio, we could get a decent view of what is currently being factored-in in terms of the deterioration of business fundamentals. As a starting point, the stock is no longer valued at excessively high levels as it used to be in FY 2021 and FY 2022. That is why it is harder to make a bearish case at the moment, but that doesn’t mean that DE is attractively priced at the moment. Although margins are still at record highs, they have a long way down, if we witness a proper cycle downturn. With that, the price/sales multiple is still way above the levels it was back in the 2015-16 period when net farm income bottomed during the previous cycle.

prepared by the author, using data from Seeking Alpha and SEC Filings

Conclusion

Deere’s stock is no longer a sell in my view, but is unlikely to become attractive anytime soon. The wave of outlook downgrades has just begun a few quarters ago, and betting on a quick recovery is very risky. Moreover, the stock remains priced at levels that already assume a very minor downturn in demand for agriculture machinery across the globe. Although this might be just so, it skews the risk-reward ratio of the stock at unfavorable levels for current investors.

Credit: Source link

{kind=link}