Ronny Gäbler

Thesis

Crexendo, Inc. (NASDAQ:CXDO) is experiencing double-digit organic growth in mostly recurring revenue. Operating expenses are likely to compress over the next couple of years. Crexendo has the best-in-class product offering in a rapidly expanding industry. It has a pristine balance sheet and a large pool of bite-sized accretive acquisition targets.

The management team is heavily invested and seems shareholder-value-focussed. Analyst estimates for revenue seem plausible if only considering organic growth. However, they don’t understand Crexendo’s operating leverage, leading to low earnings estimates. They also entirely ignore the M&A strategy. That ticks just about all the boxes that I can think of.

Based on my free cash flow (“FCF”) model for pure organic growth, I could see the stock tripling within a few years. Factoring in their M&A strategy, a triple would be a disappointment.

Introduction

Crexendo offers Unified Communications as a Service (UCaaS) to enterprises. UCaaS connects a company using communication tools such as voice, video, messaging, collaboration, and the cloud. Crexendo also resells accompanying hardware. Most revenues are for recurring services, with rolling contracts typically lasting 36 or 60 months.

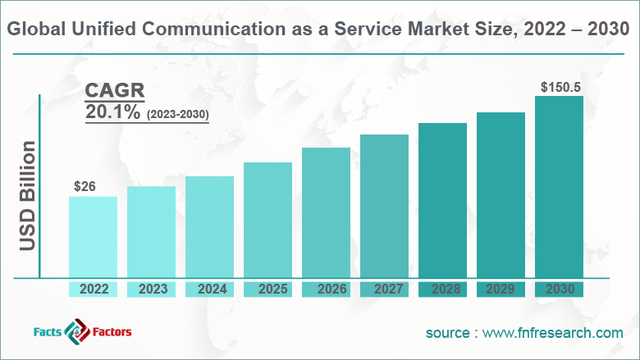

As shown by the strong growth trend below, UCaaS is being adopted by enterprises at a fast pace.

Global UCaaS market forecast until 2030 (FNF Research)

While there’s plenty of competition in the space, a Frost & Sullivan report stated that Crexendo has the industry’s fastest-growing platform. This trend is also evident in Crexendo’s revenue growth, which has quadrupled in the past five years, growing considerably faster than peers. I expect this trend to continue, supported by a healthy backlog that grew 36% in 2023 to nearly $69m, with $30m expected in 2024.

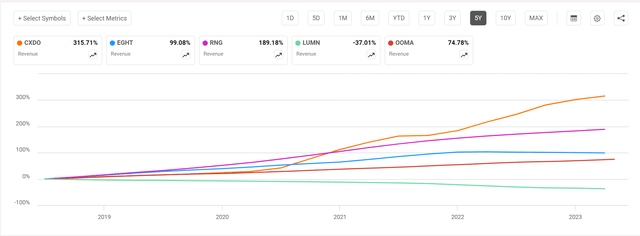

5 year revenue growth of CXDO and peers on % basis (Seeking Alpha)

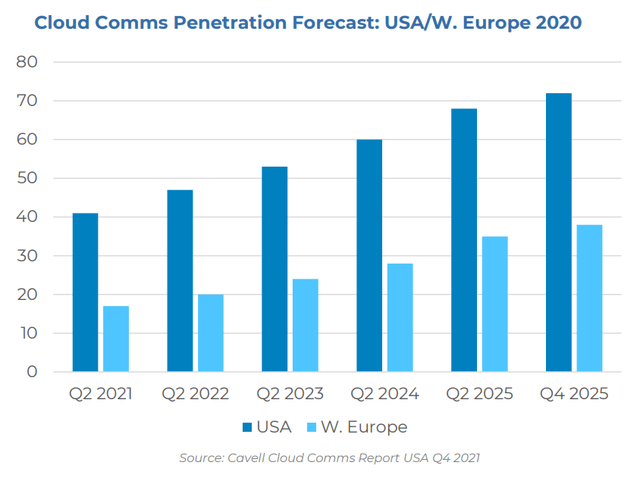

UCaaS adoption is lagging internationally, as seen below, representing a significant potential growth market. Crexendo grew 74% in international markets, including the UK, EU, and Australia. I foresee this as being a significant growth driver for Crexendo in the future.

Cloud comms forecast by geography (Cavell Cloud Comms Report USA Q4 2021)

Product

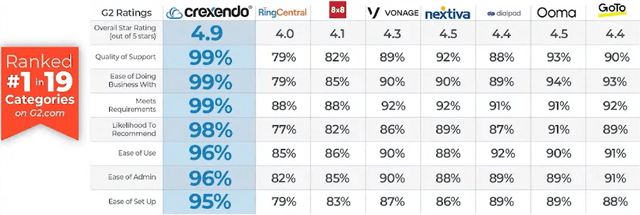

Crexendo’s strong growth is partially attributed to its superior product. The company recently won the Internet Telephony Product of the Year Award for the fourth consecutive year. The product has 200 excellent reviews on the software review site G2, far ahead of its competition. I noticed that the only two reviews below four stars are from 2020 and 2022, perhaps indicative of ongoing improvements in the product.

Customer satisfaction scores for CXDO’s platform vs peers (Chart by Crexendo, Data from G2)

Crexendo provides exceptional customer service and support, crucial for small and medium businesses often requiring extra assistance. The company is well-positioned to capitalize on the growth in this market segment.

Crexendo is currently integrating AI solutions into its platform. One example is an AI tool that automatically designs a hotline’s dial-option structure based on a company’s website or other information. Another example is taking action if it detects sentiment or key phrases within a call and performing an action. For instance, if a customer service call becomes heated, a manager can be notified and brought into the call to defuse the situation. Similarly, if a customer mentions electric vehicles during the call, a salesman with experience selling EVs could be notified, increasing upsell likelihood.

Crexendo doesn’t design all these tools itself; it currently offers 240 applications on the system via API. This keeps development costs relatively low while delivering an expansive variety of tools.

Crexendo markets this product directly to users under its Cloud Telecommunications Services (CT) segment and through licensees under its Software Solutions (SS) segment. I’ll discuss and analyze these businesses separately before considering the combined company.

Cloud Telecommunication Services

CT Introduction

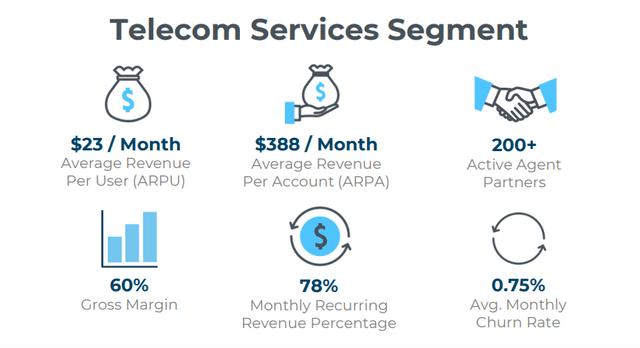

The CT segment offers UCaaS directly to businesses via its sales team and an additional 200+ agents who work on a commission basis. Most of the revenue generated comes from these services under a pay-per-seat model. CT currently represents around 65% of Crexendo’s total revenue and has over 96 thousand end users.

Cloud Communications Infographic (CXDO investor deck)

Around 20% of CT revenue comes from hardware reselling, which has lower margins but strengthens customer loyalty and satisfaction and is still profitable.

Crexendo faces significant competition in selling UCaaS directly to customers, but it competes well.

List of competitors to CXDO in D2C space (CXDO investor deck)

I like that Crexendo is the only company that develops and markets its platform to end customers. Competitors market Microsoft, Cisco, or other developer platforms. This control allows Crexendo to align its product to better meet customer needs. Also, Crexendo has minimal debt, while its competitors are highly leveraged, which drives up their cost base.

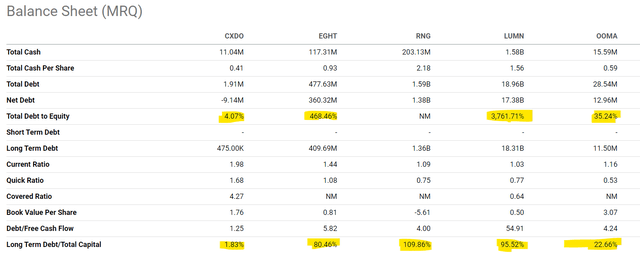

Balance sheet key numbers for CXDO and peers (Seeking Alpha)

The NetSapiens Acquisition

In June 2021, Crexendo acquired NetSapiens’ licensee-focussed “VIP platform.” This platform was the birth of the Software Solutions segment, which I will discuss later. The company is actively transitioning its direct customers from its legacy platform to the superior VIP platform, hoping to finish by the end of summer. Once complete, Crexendo will retire the old platform to reduce operating expenses by over $1m annually.

The Allegiant Acquisition

In November 2022, Crexendo acquired Allegiant Networks, a former customer of their Software Solutions offering. The acquisition added 650 direct customers and $10.5m in revenue, which grew 21% in 2023.

The Allegiant acquisition was partly motivated by the desire to expand Crexendo’s product offering, specifically in IT services, managed services (MSPs) and network services. These have a lower margin but result in stickier customers and a high UCaaS pull-through. Customers without IT/MSP services typically spend $350 per user, compared to $1200 for those with.

The gross margin for TC services fell from around 70% pre-acquisition to under 60% post-acquisition due to the addition of low-margin (~40%) revenue. At the time, management implied that gross margins would soon return closer to historic levels. The lower-margin IT services experienced surprisingly strong growth, keeping margins suppressed between 57% and 58% for a year. They increased to 60% in Q1, and management is still actively cutting expenses. I am cautiously optimistic about the gross margin upside here.

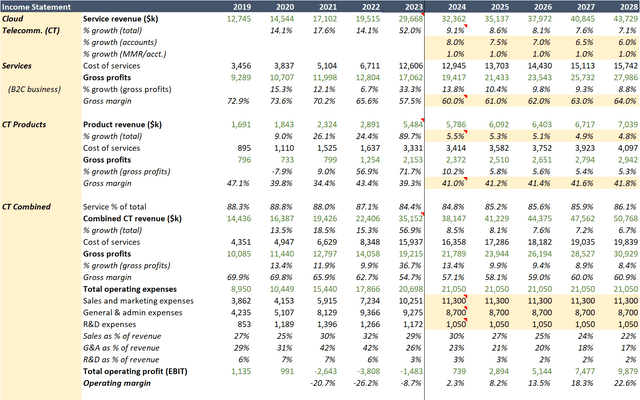

CT model

Below is my model for the CT business, which is part of my larger discounted cash flow (“DCF”) model.

Cloud Telecommunications elements of my model (My model)

Crexendo quotes CT services as growing 9% annually; we saw 9.6% YoY growth in Q1. Management has implied they do not plan any price increases soon. Nonetheless, I estimate an annual price increase of at least 1%, well below inflation, and an 8% user growth, which I reduce over time. Additionally, I estimate a slow but steady margin return towards historic levels, increasing by 1% a year to 64% by 2028.

I grow product revenue more conservatively, starting at 5.5%. This rate seems slow on a historical basis but matches the Q1 YoY growth rate of 5.7%. Using a lower estimate for this lumpy business line felt appropriate. Gross margins also fluctuate; we saw 44% in Q1. I took a 41% and increased it slowly.

Management anticipates operating expenses to fall over the year, partially driven by the $1m saving from retiring the legacy platform. To be cautious, I have changed 2024’s expenses in line with Q1’s change YoY and maintain them thereafter.

Crexendo exhibits strong operating leverage. As revenues increase, gross margins should improve, and operating expenses decrease. I anticipate operating margin expanding from breakeven to 23% in 5 years.

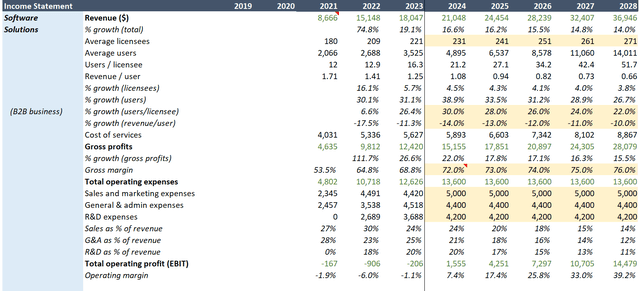

Software solutions

SS Introduction

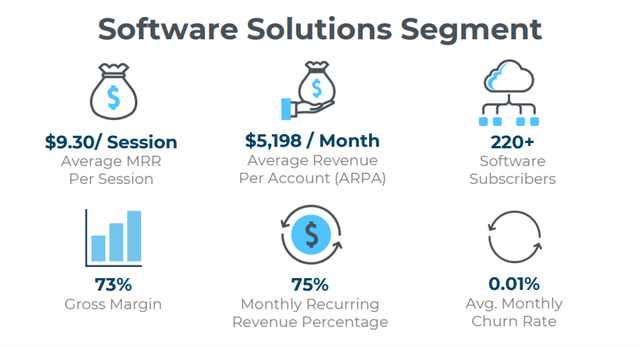

The SS segment offers UCaaS through licensees who market Crexendo’s platform. SS currently represents around 35% of Crexendo’s total revenue, with over 220 licensees serving over 4.5 million end customers.

Software Solutions Infographic (CXDO investor deck)

Crexendo competes with other platform providers in the space, particularly Cisco and Microsoft, who hold a large portion of the market.

List of CXDO competitors on D2C basis (CXDO investor deck)

Some investors wonder how Crexendo could compete against relative giants. For instance, fellow Seeking Alpha author Oliver Rodzianko expressed in January (emphasis added):

However, the investment seems to have risks over the long term, including massive competition from major and established players like Amazon.com, Inc. (AMZN) Web Services, Microsoft Corporation (MSFT) Azure, and Alphabet Inc. (GOOG, GOOGL) Cloud Platform.

In reality, Crexendo is actively winning over licensees from these competitors, with half a dozen licensees moving over from Microsoft and Cisco in 2023. In contrast, monthly licensee churn for Crexendo’s platform is 0.01%. I believe the reasons are twofold: quality and cost.

We’ve already discussed how Crexendo offers the best product in the market. Whereas Crexendo actively invests in its platform, the larger players are cutting their platform-related expenses. This will inevitably result in an increasing divergence in product quality.

Crexendo offers a unique pricing model which makes it a low-cost provider. Other platforms operate on a per-seat basis for licensees. Thus, to be profitable, licensees need to mark up the price for the end customer. In contrast, Crexendo uses per-session pricing for licensees who go on to sell on a per-seat basis. The arbitrage for licensees results in a 35-50% price reduction compared to other platforms. I like this Costco-esque model – sharing cost savings with customers can lead to robust growth and loyalty. It helps licensees compete by giving them margin flexibility that other platforms don’t have.

SS Model

Below is my model for the SS business, which is part of my larger DCF model.

Software Solutions elements of my model (My model)

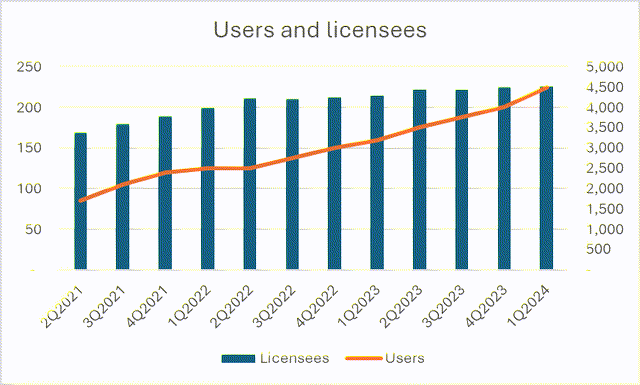

To understand the growth drivers in SS, I will explore the change in licensees, users, and revenue/user. While I discuss revenue/user, this metric ultimately represents the price/session and the number of sessions. However, I know how the number of users changes, not the number of sessions.

Graph showing licensee growth and user growth (Figures pulled from announcements/calls or estimated)

NetSapiens had around 170 licensees when it was acquired in mid-2021. Within a year, this number shot up to over 210. The growth rate has since slowed, partially due to Crexendo cleaning up its licensee list by removing/merging some licensees. The number is currently over 220. I’ll add around ten licensees each year to reflect the recent growth rate. This should prove conservative, especially considering the whole period’s growth rate is twice as high, and the recent growth rate appears artificially reduced due to the list cleaning I mentioned.

In Q4 last year, Crexendo’s user count surged 0.5m sequentially, hitting 4m. Management implied that by the end of FY24, they could grow by another 0.5-1m. They achieved 0.5m of that in Q1 alone, reaching 4.5m users. While my model suggests a YoY growth rate of 30%, higher than in previous years, most of the growth this year is locked in already.

Licensees, users and revenue over time, including ratios of these (Numbers from earnings reports or calls, ratios are calculated)

Revenue generated per end user appears to be declining. Since prices are not driving this, new users must use fewer sessions than existing users. When speaking with management about this trend, they mentioned that there is often a lag between new users on the platform and then starting to use sessions.

Take my breakdown with a grain of salt. The number of users per licensee appears to grow by 30% annually, while revenue per user declines by 14% annually. When asking management, they didn’t agree with these trends, stating user/licensee growth to be more like 5-15% and not acknowledging the revenue per user decline. I show these numbers anyway, given that I derive them from user, licensee, and revenue numbers provided by management. In any case, they lead to a segment growth rate of 16.6%, below Crexendo’s quoted 19% CT growth rate.

Gross margins hit a new high of 73% in Q1. Management suggested they could stay in the 72-73% range this year but should gradually continue to climb, seeing a roof likely near 76%.

As with the CT segment, I increase operating expenses in line with Q1’s relative YoY change and then hold them steady. Management is expecting cuts here, so I consider my estimates conservative.

This segment should exhibit similar operating leverage, but the organic growth should be faster. Thus, the operating margin in this segment will grow from around breakeven to almost 40% by 2028.

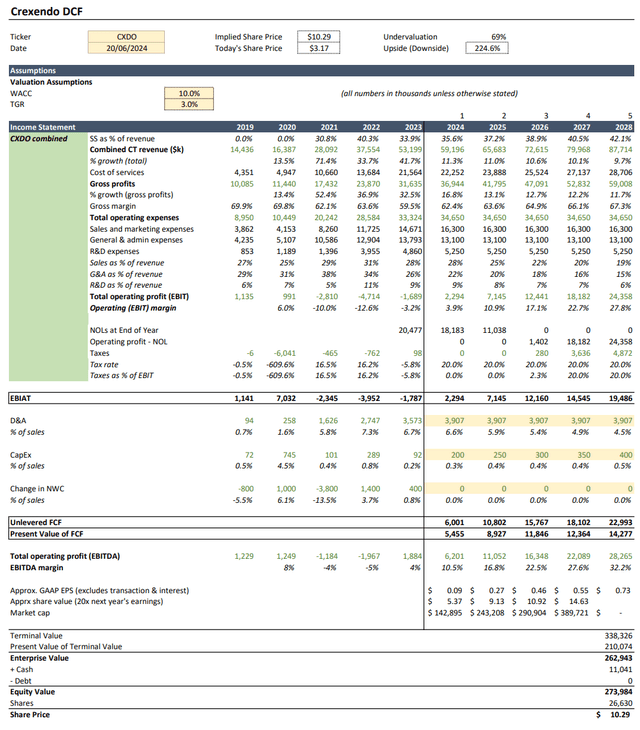

Valuation of combined business (organic only)

Below, I combine business segments and run a DCF analysis.

DCF model for CXDO’s combined business – organic only (My model)

Additional assumptions include no increase of D&A (conservative but matches steady operating expenses in other areas) or Net Working Capital, and slowly increasing Capital Expenditure requirements. WACC at 10%, and Terminal Growth Rate at 3% (low considering the impressive CAGR of the industry).

This model only considers organic growth but shows a potential undervaluation of 69% on a cash flow basis. I also included my expected EBITDA and net income (GAAP) for each year as an additional valuation metric. Using a multiple of 20x for next year’s earnings, I believe the share price is 41% undervalued on a GAAP basis. If using non-GAAP, which analysts tend to use for this company, 2025’s EPS would almost double to $0.50, suggesting a fair-value of $10 a share. If Crexendo could generate $0.73 of earnings (non-GAAP) by 2028, the share price could appreciate to $14.50, 4.6x higher than today.

Another validation of Crexendo’s value is the recent M&A in the space. In October 2023, competitor OOMA acquired 2600HZ for 5x revenue. 2600HZ had only 500k users and declining revenues. Crexendo is currently priced at 1.5x sales, despite a more robust offering and faster growth. Using this year’s revenue and a 5x sales multiple implies a fair value of $11 and an undervaluation of 71%.

Acquisition strategy

Crexendo hopes to make 1–2 acquisitions a year in the $10-15m revenue range from its pool of 220+ existing licensees. Allegiant came from this pool. These businesses would likely be immediately accretive, and Crexendo would look to cut duplicate operating costs.

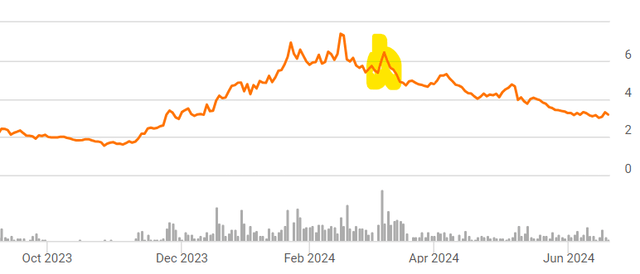

We’re looking at around $66m in revenue in 2025 on a pure organic business. However, the company hopes to hit $100m in 2025. To achieve this ambitious goal, Crexendo would have to make three acquisitions of around $10m. The acquisition strategy was my primary concern when performing this analysis because of the size of these acquisitions relative to the business and because the Allegiant acquisition brought lower gross margins. This sentiment was likely a significant factor in the recent decline in share price. The earnings release seemed otherwise positive, but management announced a resumption of their M&A efforts, which had been on hold for the last year.

1-year stock chart highlighting in yellow the announcement to continue with the acquisition strategy (Seeking alpha, highlight mine)

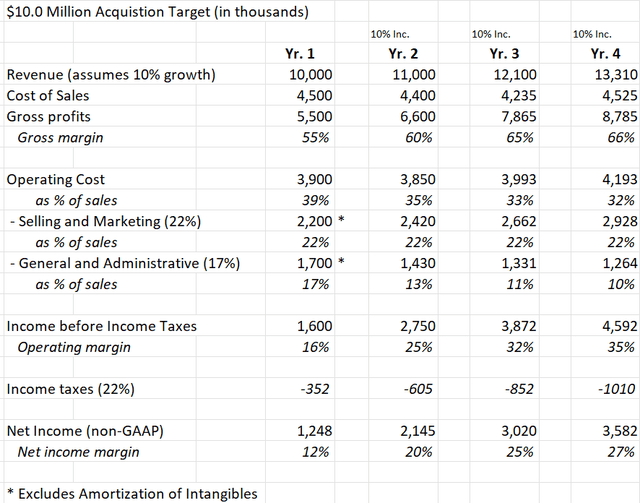

Covering this with management, they provided a rough model of what the profitability of these acquisitions might look like. Please note these estimates are forward-looking, with all disclosures that come with that. Actual results will differ. Nonetheless, the information below provides an excellent insight into the profile of companies that Crexendo aims to acquire. In addition, please note that I added estimates for the fourth year under conservative assumptions; I needed a 4th year for my DCF model.

Acquisition model example forecast (Numbers used by way of example by management – reality likely to differ)

There are several things to note here. First, management suggests revenue growth of 10%. This seems conservative, as cross-selling after an acquisition often accelerates revenue growth, as we saw with Allegiant. Second, the gross margins are significantly higher than with Allegiant. Whereas Allegiant expanded the offering with lower margin revenue, future acquisitions will likely have similar margins to Crexendo’s main services revenue pre-Allegiant. Third, while S&M expenses stay steady relative to sales, G&A expenses are stripped out as expected, reducing from $1.7m to $1.25m after three years.

All this leads to a profit margin of 12% after one year and 25% within three years. If management can deliver this kind of acquisition regularly, the payback period is a mere four years. These businesses would be hugely accretive for Crexendo.

If Crexendo makes nine acquisitions by 2028, they’ll spend ~$90m. Crexendo has around $8m net cash. Including the acquisition’s cash flow, Crexendo could generate around $107m in additional cash by 2028 (as shown later), more than enough to cover the acquisitions. The first acquisition should be easy, but the next 2-3 is when cash would be tightest, given cash flows have not yet ramped up, and the net cash will have been used on the first acquisition. I believe the company would need to raise up to an extra $20m to fund these earlier acquisitions.

If Crexendo used equity, I would hope it’s at higher prices than today, given the current undervaluation. As a thought exercise (acknowledging considerable uncertainty in financing), if Crexendo had to raise $10m via equity, that would represent a 12% dilution from today’s prices. If they raised at a $5 share price, dilution would drop below 10%, which, I think, would be more palatable for investors. That said, based on management comments, I believe the cash will come largely from debt. $20m in long-term debt would easily be manageable at these cash flow levels.

Valuation, including acquisition strategy

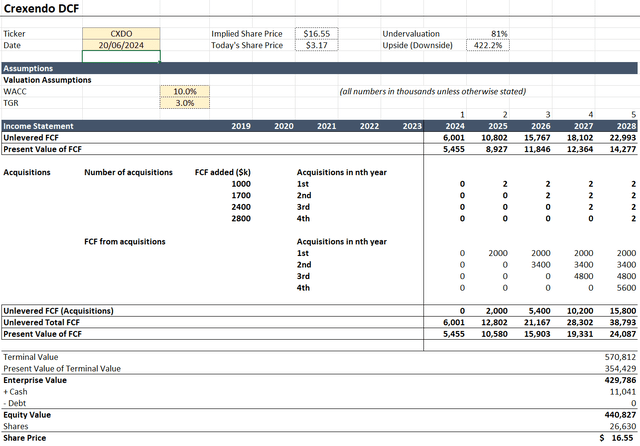

I’ve included my updated DCF analysis below. The FCF from the existing business remains unchanged, but I add on the FCF generated from the potential acquisitions. I assume two acquisitions a year, with just one this year. However, I include no contributions this year, since any acquisitions would contribute less than a year. In 2025, we should have one business reaching one year after acquisition, with two more in their first year. To simplify this, I estimate two acquisitions annually that reach the one-year-after-acquisition mark.

DCF model updated to include acquisition strategy (My model)

This model simply adds the FCF from the acquisitions to the FCF from the first model. To estimate the acquisitions’ FCF, I use the model provided by management above. The net income excludes D&A, so it would be similar to FCF. However, I slash the net income by 25% to be conservative and account for delays or worse-than-expected results.

As estimated above, the FCF generated would be very significant to the company, potentially lifting FCF by 19% in 2025 and 69% by 2028. The fair value of the share price when considering acquisitions would be $16.55. Even assuming a 10% dilution, we’re still looking at $15, or an 80% undervaluation.

Management

In March 2023, Crexendo announced Jeff Korn as the new CEO. He’s a veteran at the company and previously ran their legal division. I believe he’s hit the ground running. He immediately paused the M&A strategy to allow Crexendo to better digest previous acquisitions. He also cancelled the dividend, a move I fully support considering the returns I believe they could generate with their M&A strategy.

Overall, I like the management team’s philosophy. They recognize the value of happy customers. They want to grow fast, keep costs down and drive shareholder value. Check out this quote from a recent GEO investing interview.

What really keeps us up at night is our obligation to our shareholders and to the almost 3.5 million users on our platform…. We take that very, very seriously. We take generating cash very seriously and we take profitability very seriously. While we can’t control the stock price, we can control how we operate the business, and that’s what we remain focussed on… We always want to manage the business on fundamentals.

Actions speak louder than words, so let’s examine some of the strategic moves the team has been making: reducing debt, driving cost savings by letting go of NetSapiens’ expensive prime-location offices, and retiring the legacy platform.

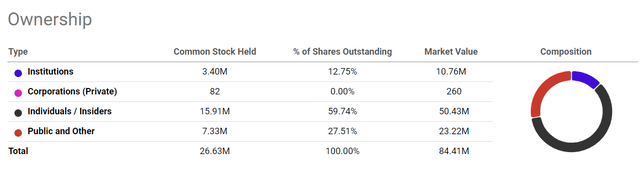

While recent insider purchasing has been small, there is some. Since May, the Chief Revenue Officer, Jon Brinton, has purchased 7,000 shares on the open market for around $25k. He was buying as low down as $3.22. The team is already highly invested.

Ownership chart (Seeking alpha)

Risks

The risk of insolvency is minimal, considering the net cash position and cash flow positivity.

As mentioned earlier, the biggest concern I see investors having is that Crexendo will lose out to its larger peers, Microsoft and Cisco. However, as noted prior, I believe this risk is overstated, and the opposite will continue.

My largest concern was that the business would grow revenue through unprofitable acquisitions. However, after speaking to management about it, my fears on this front are much smaller. Assuming the acquisition strategy is executed roughly in line with the plan, it will benefit shareholders and not simply drive revenue growth.

One important note is that the acquisition strategy’s resumption will reduce GAAP net income, given that non-cash amortization will likely increase substantially. This is why I preferred to value the business on a cash-flow basis.

Investors should also consider that financing of future acquisitions is still unknown. While I hope a large portion will come from cash, there will inevitably be debt or equity components. Debt carries its own risks, which are difficult to quantify without knowing the amount or terms. Equity raises at these levels would be a shame, though I wouldn’t mind limited dilution at higher share prices.

Naturally, the core of the thesis rests on continued organic growth and steady operating costs. Though I’ve tried to keep assumptions conservative, the investment thesis would be significantly weakened if revenue slows dramatically or if operating expenses increase quickly.

Further risks associated with microcap stocks should be considered. Liquidity will be lower than with larger names, and the market value may not reflect the stock’s intrinsic value for extended periods.

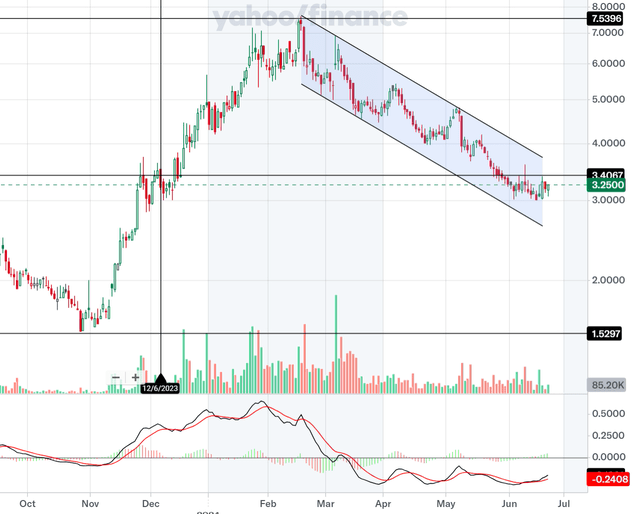

Technical analysis

Technical analysis for 1-year CXDO chart (Yahoo finance, additional lines mine)

The stock had a huge run-up from November last year until mid-February. Since then, the stock has been following a clear downward channel. The MACD indicator is negative, though it is beginning to pick up. I think the short-term trend is likely up, but it remains to be seen whether that will be a bounce in the medium-term downward trend or if it might mark a turning point. One thing besides fundamentals that gives me hope of this marking the turning point is that the stock is near the 50% retracement following its big run-up.

Summary

I rate Crexendo, Inc. stock a strong buy. It has the strongest product offering and business model in the industry. It is profitable and growing fast, with a net cash position and an attractive M&A strategy. However you look at it—on a sales, earnings, or cash flow basis—it is hugely undervalued. I am personally making it a core position of my portfolio.

|

Valuation model |

Fair share value (excl. M&A) |

Fair share value (incl. M&A) |

|

DCF |

$10.29 |

$16.55 |

|

P/E (non-GAAP) |

$10 |

|

|

P/E (GAAP) |

$5.40 |

|

|

P/S (based on recent M&A) |

$11 |

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Credit: Source link

{kind=link}