JamesBrey

Transcript

BlackRock investment leaders recently met to discuss our Midyear Outlook.

There’s a growing consensus that interest rates will stay high for longer due to persistent inflation.

1) Higher rate reality hits

Seven months ago at our last Forum, markets were pricing in as many as seven Federal Reserve rate cuts.

Instead, the Fed has held rates steady and has started adjusting to the reality that rates will need to stay high for longer.

Market pricing has adjusted accordingly.

2) Higher inflation playing out

We see central banks forced to keep interest rates higher than before the pandemic. That’s because structural constraints on supply are driving persistent inflation.

Many have pinned hopes on AI boosting productivity in the long term, easing inflationary pressure. Yet, there’s a growing view among portfolio managers that the initial capital spending boom to unlock those gains could initially be inflationary.

Here’s our Market take

We think resilient growth supports our risk-on stance over a 6-12-month horizon, and we don’t see an AI bubble.

The profitability of mega-cap tech companies stands in contrast to the dot-com bubble, and we stay overweight equities, technology and AI.

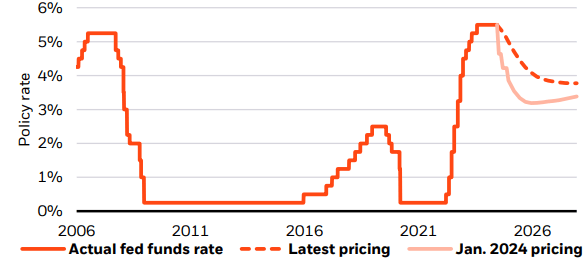

Higher rate reality hits

Historic and market pricing of fed funds rate, 2006-2027

Forward looking estimates may not come to pass. Source: BlackRock Investment Institute, with data from LSEG Datastream, June 2024. Notes: The chart shows the historic future fed funds rate and the expected future path priced into SOFR futures.

Since our last Forum seven months ago, the growing consensus among our portfolio managers is that we’re in a higher-for-longer interest rate environment. Back then, markets were pricing in repeated Fed rate cuts in 2024. Instead, the Fed has held its finger on the pause button, including last week. The Fed has gradually been adjusting to the reality that rates will need to stay high for longer – not only in the short term but also further out. That’s illustrated by the gradual upward revision of its own estimate of long-run interest rates. Market pricing has adjusted accordingly. See the chart. The European Central Bank’s move to cut rates earlier this month with growth improving, inflation still above target and unemployment at a record low did not mark the start of a deep rate-cutting cycle, in our view. The same will be true of the Fed if it starts to ease later this year, we think.

We see central banks forced to keep interest rates higher than pre-pandemic to tackle persistent inflationary pressures. The new macro regime is marked by higher inflation, higher rates, and lower growth due to supply constraints. We see this unprecedented macro cocktail persisting. Population aging, the rewiring of global supply chains, and the low-carbon transition are constraining production and driving capital investment as economies try to adapt.

AI to the rescue?

At our last Forum, AI garnered attention as a technology that could boost productivity in the long term, easing inflationary pressures. Those gains could still come – though they will likely take time to realize. And our portfolio managers increasingly think the initial AI capex buildout required to unlock the benefits could be inflationary. Capital spending on AI data centers has boomed since last year’s ChatGPT moment. A lot more is coming in the years ahead. This capex boom and draw on resources could create bottlenecks, meaning AI will likely be inflationary in the near term before unlocking any of the long-run benefits that could ease inflationary pressures. This nuance is not appreciated by markets or central banks, in our view.

Where do markets go from here? We believe the most likely scenario is a concentrated group of AI winners driving returns over a tactical horizon of six to 12 months. We stay overweight tech and the AI theme. The AI rally is supported by earnings and has more room to run, in our view. We don’t see an AI bubble, and the profitability of mega-cap tech companies stands in contrast to the unprofitable companies driving the dot-com bubble. Healthy corporate balance sheets and earnings momentum support our pro-risk view. We think the maturing debt of investment grade companies is manageable in coming years, even with higher rates. And earnings keep improving: Eight out of 11 S&P 500 sectors expanded net profit margins in Q1, LSEG Datastream data show. Our risk-on stance means we broadly prefer equities over fixed income. Yet higher-for-longer rates mean we like short-term bonds for income. Look for more details in our 2024 Midyear Outlook in coming weeks.

Our bottom line

We see a concentrated group of AI winners driving returns over a short-term tactical horizon. We stay overweight tech and the AI theme. Our risk-on stance leads us to prefer equities over fixed income, but we like the short end for income.

Market backdrop

U.S. stocks hit record highs and are up about 14% this year. U.S. 10-year Treasury yields fell roughly 20 basis points to near 4.20%. The U.S. CPI for May came in below expectations thanks to a broad moderation in core services inflation. The Fed held rates steady as expected and now sees only one rate cut this year. Yet, the Fed’s data-dependence means we don’t put much weight on its policy signals. French government bond yields jumped on worries about the snap election outcome.

We await UK CPI data this week and expect the BOE to look toward August to cut rates. Despite upside surprises in core services, falling goods prices are offsetting sticky services inflation – dragging overall inflation lower. Still, the BOE has acknowledged the risk of heightened inflation, especially due to the impact of geopolitical tensions.

Credit: Source link

{kind=link}