tadamichi

By Sean Bogda, CFA, Grace Su & Jean Yu, CFA

Fiscal Easing Boosts International Stocks

Market Overview

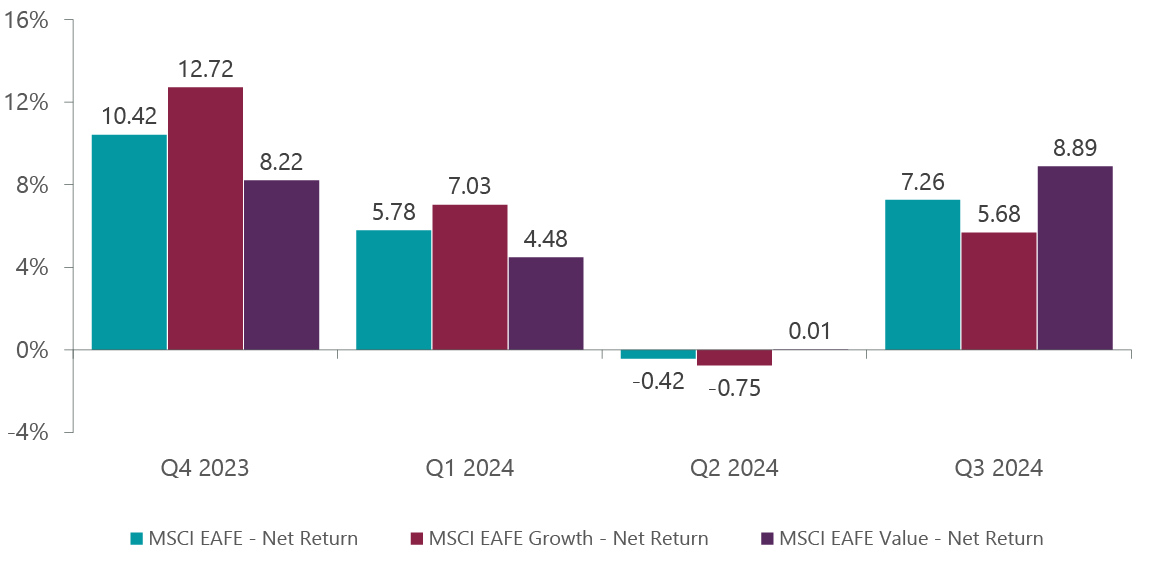

International markets generated positive returns in the third quarter as rate cuts and financial easing from global central banks helped spark a rotation into value sectors such as real estate, utilities and communication services. Additionally, a late-quarter surge by Chinese stocks proved helpful to more cyclical sectors including materials, industrials and consumer discretionary. The benchmark MSCI EAFE Index showed positive returns across nine of its 11 sectors, with only energy and information technology declining. Value outperformed growth during the quarter, with the MSCI EAFE Value Index returning 8.89% versus the 7.26% return of the MSCI EAFE Index and the 5.68% of the MSCI EAFE Growth Index (Exhibit 1).

Exhibit 1: MSCI Growth vs. Value Performance

Data as of Sept. 30, 2024. Source: FactSet.

Despite the Bank of Japan having telegraphed its intention to raise interest rates for quite some time, the size of its rate hike in August caught investors off guard, leading to a spike in market volatility on concerns that tightening of economic policy would pressure its nascent recovery. This was further exacerbated by a violent unwinding of the pervasive yen carry trade as the currency strengthened during the quarter, all of which culminated in Japan being the worst-performing region in the benchmark. Despite the increase in market volatility, we are seeing signs that Japanese businesses have become more efficient and profitable – in part due to improving corporate governance measures – and are beginning to share these gains with employees in the form of the largest wage increases in over a decade, which will hopefully translate into greater consumer confidence and spending.

International investors were not disappointed when the Federal Reserve elected to cut rate by 50 basis points at its September meeting, sparking a strong rally in U.S. markets and a rotation into smaller value and cyclical stocks. With the first rate cut in the rear view, the question now shifts from “when” to “how much,” with policymakers carefully watching as inflation appears to be coming back in line with its target and whether the U.S. economy can indeed stick a soft landing. Investors now look toward the U.S. presidential election in November, rampant with speculation as to what the permutations of political math would mean on policies surrounding international policy, trade and immigration.

“With the first rate cut in the rear view, the question for the Fed now shifts from ‘when’ to ‘how much?'”

The European Central Bank (ECB) and Bank of England also cut interest rates during the quarter, the second cut in three months for the ECB and the first in four years for the BoE, as the U.K. and eurozone central banks have embarked on a more measured approach considering the slow growth rates in their respective economies. In the U.K., the snap election and landslide victory of the previously opposition Labour Party in July has resulted in a significant shift in political direction as well as economic priorities and policies. While the U.K. economy continues to hold up more strongly than those across the Channel, this new direction has spurred greater uncertainty as to the details on what these new policies would mean for the economy and markets.

While businesses and consumers continue to painfully adjust to an economy no longer tethered to property development and globalization, Chinese stocks surged late in the quarter following the announcement of an unusually broad stimulus package aimed at revitalizing the world’s second-largest economy. The People’s Bank of China announced that it would cut both policy interest rates and mortgage rates and, along with its existing plan to lower bank reserve ratios, set aside billions in stimulus funds for loans to brokers and insurers to purchases equities and help listed companies finance share buybacks. While the tone of Chinese government officials seems more determined than in prior iterations of policy support, there remains a considerable amount of skepticism from economists and investors that these initial efforts can translate into a durable and sustained turnaround for the broader Chinese economy.

Quarterly Performance

The ClearBridge International Value Strategy outperformed its benchmark in the third quarter as strong performance from our holdings in the consumer discretionary and financials sectors overcame headwinds from our energy exposure.

In consumer discretionary, the combination of macro tailwinds and strong idiosyncratic drivers helped spur outperformance for Spanish retailer Industria de Diseno Textil (OTCPK:IDEXY, Inditex) and U.K.-based catering company Compass Group (OTCPK:CMPGF). Inditex, a fast fashion, footwear and accessories retailer, continues to show strong operational execution despite softer consumer trends in Europe. The company’s investments in technology and building out both its ecommerce and omnichannel operations, store refurbishments and supply chains continue to reap the rewards of creating a differentiated and positive experience for its customers versus its competitors. Compass Group has also been able to show strong performance, delivering higher growth rates relative to its pre-COVID levels, due to the company’s strategic focus on growing its outsourcing business and targeting underdeveloped markets in Europe where it can benefit from its size and strength.

Financials also proved beneficial, particularly European and U.K. banks with strong, well-known franchises. Our leading contributor in the sector, U.K.-based Lloyds Banking (LYG), provides a wide range of banking and financial services globally and continues to use its well-capitalized balance sheet to its advantage despite a challenging economic environment. Likewise, BAWAG (OTCPK:BWAGF), an Austrian bank, continues to perform well and completed two acquisitions during the period – Barclays Consumer Bank Europe and Dutch bank Knab – which will expand the bank’s strong brand presence across Europe.

Oil prices declined significantly in the third quarter, as signs of rising inventory levels in the U.S., lackluster demand from China and the prospect of further production increases from OPEC+ members outweighed investor concerns about a widening of Middle East conflicts. These broad-based headwinds weighed on the performance of our exploration and production holdings Shell (SHEL) and Noble (NE). However, we continue to have high conviction in these names as Shell has been able to maintain strong operating metrics despite the downturn. Likewise Noble, a leading offshore drilling contractor, continues to have a strong strategic position as the leading provider of drilling ships, which we believe has ramping earnings potential when demand rebounds.

Stock selection in Japan was also a positive contributor to performance, driven by strong year-to-date contributor Hitachi (OTCPK:HTHIY) and relatively new holding Fujitsu (OTCPK:FJTSF) – a Japanese IT services firm. Heavy reliance on technology during the COVID-19 pandemic highlighted the need for more investment and modernization in IT services for both consumers and businesses, creating a multiyear wave of investment that directly benefits Fujitsu. Hitachi has also benefited from demands for investment and modernization in areas like power grids. Additionally, the company closed the acquisition of Thales’ rail signaling business, which we believe will create synergies that should improve the profitability of its domestic systems integration business.

Portfolio Positioning

We added a new position in utilities company National Grid (NGG), which transmits and distributes electricity and national gas in the U.K. and U.S. The current investments in AI and data centers will undoubtably also increase demand for energy and, with the company’s shares currently trading at a historical discount, we believe that the market is overlooking National Grid’s attractive long-term outlook, improved balance sheet and footprint within favorable regulatory environments.

We also added SONY, the Japanese electronic equipment and devices conglomerate. While a cyclical slowdown in demand for the company’s image sensors has weighed on recent earnings, it has also created a compelling entry price to gain exposure to its attractive games and gaming platform segments, including the PS5 gaming console. Additionally, we believe that the divestiture of its financial services business will result in a greater focus on core strengths within its content businesses.

We exited our positions in Inpex (OTCPK:IPXHF), a Japanese energy company engaged in oil and natural gas production, and Metso Oyj (OTCPK:OUKPF), a Finnish industrials company that provides solutions and services for aggregates, minerals processing and metal refinement industries. Inpex reached our price target during the quarter, while Metso was sold to fund more attractive investments.

Outlook

The two macro shocks during the quarter, Japan and China, serve as good reminders of extreme imbalances in the market today – notably the significant market concentration in a narrow sleeve of growth mega themes in the U.S. With the prospect of an increasing liquidity backdrop, stable economic prospects across most major international markets and the potential for Chinese policy support to remove a major drag from global growth, conditions remain supportive for a continued rotation to value and cyclical segments of the market.

In addition to increased market breadth, we also have seen the capex cycle around generative AI broaden out significantly as investors grapple with constraints around power and infrastructure. We are optimistic that this will continue to offer us opportunities to participate in this secular growth theme through stocks which remain overlooked and reasonably priced.

The improving economic and financial conditions notwithstanding, we recognize remaining event risks in light of the coming U.S. election and the geopolitical situation. As such, we have stayed balanced in our portfolio positioning, adding to utilities for defense and Chinese consumer companies for offense, with flexibility to pivot as things develop.

Portfolio Highlights

The ClearBridge International Value Strategy (MUTF:SBIEX) outperformed its MSCI EAFE benchmark during the third quarter. On an absolute basis, the Strategy had gains across 10 of the 11 sectors in which it was invested. The financials and industrials sectors were the main contributors, while the sole detractor was the energy sector.

On a relative basis, overall stock selection positively contributed to outperformance, partially offset by asset allocation effects. Specifically, stock selection in the consumer discretionary, financials, IT, consumer staples and health care sectors benefited returns. Conversely, stock selection in the materials sector, overweight allocations to the energy and IT sectors and an underweight to the utilities sector weighed on returns.

On a regional basis, stock selection in Europe Ex U.K., Japan and the U.K. and an overweight to North America were beneficial. Conversely, stock selection in North America, an overweight to emerging markets and an underweight to Asia Ex Japan detracted.

On an individual stock basis, Inditex, Fujitsu, Nexans (OTCPK:NXPRF), Hitachi and BAWAG Group were the leading contributors to absolute returns during the quarter. The largest detractors were Samsung Electronics (OTCPK:SSNLF), Shell, Gerresheimer (OTCPK:GRRMF), Marubeni (OTCPK:MARUY) and Galaxy Entertainment Group (OTCPK:GXYEF).

During the quarter, in addition to the transactions mentioned above, the Strategy initiated new positions in Willis Towers Watson (WTW) in the financials sector, Toho (OTCPK:THOOF) and Tencent (OTCPK:TCEHY) in the communication services sector, THK (OTCPK:THKLY) in the industrials sector and Akeso (OTCPK:AKESF) in the health care sector. The Strategy exited positions in Bayerische Motoren Werke (OTCPK:BMWYY) and Galaxy Entertainment in the consumer discretionary sector, Nihon M&A (OTCPK:NHMAF) and Julius Baer (OTC:JBPCF) in the financials sector and Japan Airlines (OTCPK:JAPSY) in the industrials sector.

Sean Bogda, CFA, Managing Director, Portfolio Manager

Grace Su, Managing Director, Portfolio Manager

Jean Yu, CFA, PhD, Managing Director, Portfolio Manager

|

Past performance is no guarantee of future results. Copyright © 2024 ClearBridge Investments. All opinions and data included in this commentary are as of the publication date and are subject to change. The opinions and views expressed herein are of the author and may differ from other portfolio managers or the firm as a whole, and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither ClearBridge Investments, LLC nor its information providers are responsible for any damages or losses arising from any use of this information. Performance source: Internal. Benchmark source: Morgan Stanley Capital International. Neither ClearBridge Investments, LLC nor its information providers are responsible for any damages or losses arising from any use of this information. Performance is preliminary and subject to change. Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent. Further distribution is prohibited.

|

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Credit: Source link

{kind=link}