Sergei Dubrovskii

(Note: Cenovus Energy is a Canadian company listed on the NYSE that reports using Canadian dollars unless otherwise stated.)

Cenovus Energy (NYSE:CVE) has made tremendous progress since I wrote an article on the great bargain that the purchase of the ConocoPhillips (COP) partnership interest. Back in 2017, cash flow in the years before the acquisition maybe hit C$1 billion in a good year. Now it does that more than quarterly.

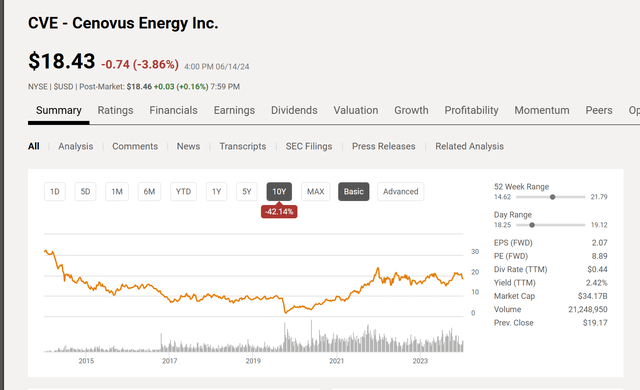

Cenovus Energy Common Stock Price History And Key Valuation Measurements (Seeking Alpha Website June 15, 2024)

But as the stock price history shows, you as an investor would never have known about the business progress made from the stock price action for several years after the acquisition.

When I wrote the last article, I stated there was more cash flow on the way because the percentage available to shareholders to distribute was about to increase. But then I received questions about why the stock price is acting the way it is if that is the case. The last time around, as the stock price history clearly shows, it did not respond.

What happened instead is the price-earnings ratio kept declining as profitability measures increased because Mr. Market was focused on other things that obviously looked scary and would threaten the future of the stock (and the company). There were naturally some quarterly bumps and bruises along the way. But nothing as catastrophic as Mr. Market imagined.

It really was not until after the covid challenges began fading that the stock price finally began to respond to business improvements that were showing up quarterly ever since the acquisition.

This points out the patience that investors need in this industry. Even though the financials kept getting better, the stock price took years to respond to that “better”.

Even now, the price-earnings ratio is still very low, despite the fact that thermal oil companies are known cash flow generators. Thermal projects often have a major cash requirement upfront before any production can begin. This requirement is then capitalized over the project life to provide a depreciation component that is the envy of the unconventional crowd (because they wish they had it). As a result, thermal companies cash flow decently even when they report losses (as a general rule). This comes into play in several parts of the business and is a big advantage for well-run thermal companies.

The fact that Mr. Market has not responded all that much to the cash flow situation here shows how picky he is about cash flow being important.

Management even announced a base dividend increase of 29% with the first quarter earnings report, and the stock price basically yawned. This happened despite the fact that management also stated that they expected to hit the net debt target that would allow a greater percentage of free cash flow to be distributed to shareholders. At this point, the stock price action points to Mr. Market passing out from sheer boredom.

Yet, thermal companies often have cash flows better than their unconventional counterparts (generally) throughout the business cycle due to the large upfront costs that are capitalized. This even considers the fact that thermal oil is a discounted product to light oil, and the discount often widens during cyclical downturns. That makes the base dividend more defensible during a cyclical downturn than is the case for the unconventional business. But you certainly would not know that from the stock price action lately.

Refining Business

This company is the latest company to join the integrated portion of the industry through a pickup of a large volume of refining capacity with the Husky merger. This merger insulated the company from expanding discounts during cyclical downturns by allowing the company to refine its thermal production into value added products whose prices hold up far better during a cyclical downturn.

But the market has yet to give this company credit for the refining side of the company because these refineries have only been owned for roughly 3 years. That is generally not enough history for the market.

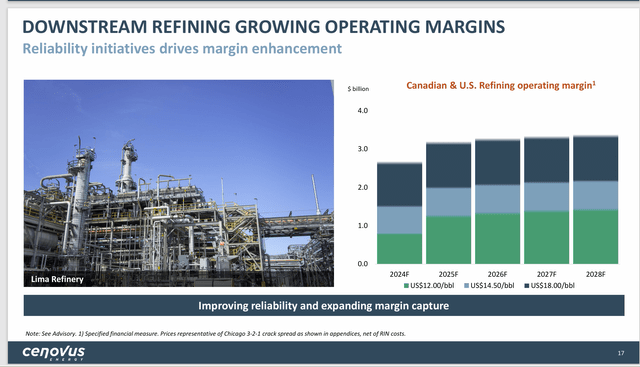

Cenovus Energy Downstream Margin Guidance (Cenovus Energy First Quarter 2024, Earnings Conference Call Slides)

Management clearly is continuing to improve operations, even though the market has yet to fully recognize the improvements already completed. The guidance above clearly points to greater profitability ahead. Yet, that current price-earnings ratio would appear to project little to no profitability improvement.

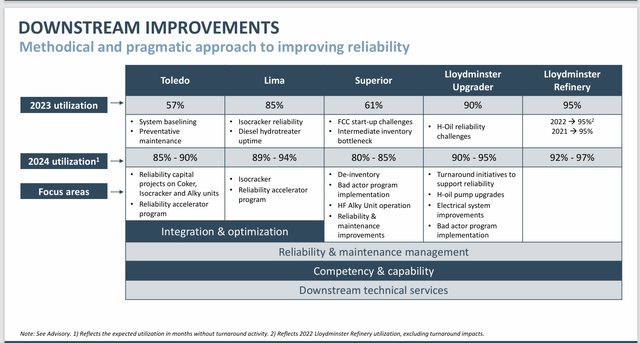

Cenovus Energy Downstream Fiscal Year Initiatives To Improve Profitability (Cenovus Energy First Quarter 2024, Earnings Conference Call Slides)

Yet, downstream clearly has some sizable profitability improvement planned for the current fiscal year. Last fiscal year was the Superior startup after the construction completed. That refinery alone will have some very positive comparisons compared to the previous fiscal year without considering the efficiency projects underway that are shown above.

There is a similar story for the Toledo Refinery that was shut down by a fire. Just getting the utilization up as shown above will send a lot more product through both refineries, which should dramatically increase the profitability of those two refineries.

In the meantime, there are profitability enhancement projects shown above that should lead to more profitability, as shown in the slide before.

The acquisition of Husky was a large acquisition. These large acquisitions often take years to optimize. Even though the market does not expect it, it would appear that management has profitability enhancement projects underway that should allow profitability to grow in excess of revenue for at least a few years.

Deep Basin

Along with all the acquisitions and sales has been the ignored Deep Basin assets acquired from ConocoPhillips. Now that debt is getting under control, that may be changing, as there are some fantastic possibilities here.

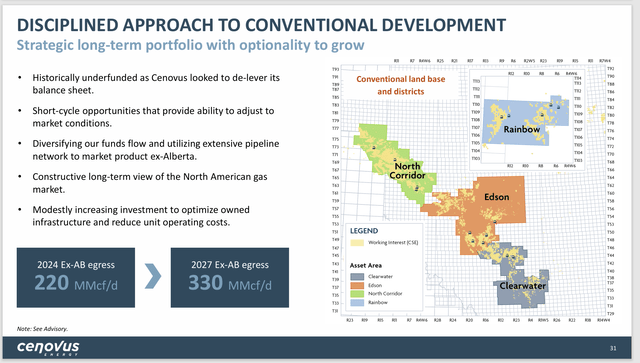

Cenovus Energy Conventional Business Opportunities (Cenovus Energy First Quarter 2024, Earnings Conference Call Slides)

This was traditionally a natural gas business. Since the acquisition was made, the technology has advanced to the point that several of these areas can now be drilled for more valuable liquids production. That alone could substantially increase the profitability of this business.

Competitors like Tamarack Valley (OTCPK:TNEYF) are reporting as many as 3 paybacks for wells drilled in the Clearwater area in the first year of production. Now that management of Cenovus has the main business “under control” some of the conventional prospects are beginning to attract attention. This acreage is looking more valuable as technology advances. It is only a matter of time before the company cashes in on that value.

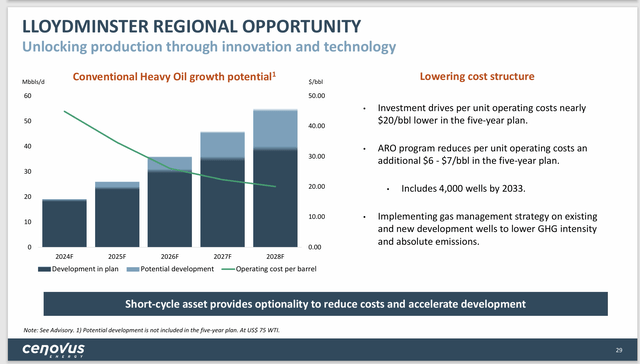

Cenovus Energy Lloydminster Regional Profitability Opportunities (Cenovus Energy First Quarter 2024, Earnings Conference Call Slides)

This is yet another part of the acquired Husky business that can be improved still more in the future.

Heavy oil is particularly profitable for the company, as the manufacturing part of the business takes a discounted upstream product and refines it into something more valuable. As a result, the company is not nearly as exposed to the heavy oil discount as it was when it sold the upstream product on the market (or when Husky had to sell product on the market).

Summary

As long as the company continues to improve profitability, then this stock remains a strong buy, as it is nothing close to being overpriced. People always ask me about “buy under” but the stock is so cheap that any reasonable strategy is likely to result in good capital gains. “Buy under” is something to worry about later when the price-earnings ratio heads past 13.

However, as was shown by the stock price history above, sometimes, this stock takes a while to respond to profitability improvements because Mr. Market has his focus on the latest strategy that will destroy the industry. Of course, that destruction has yet to happen. But then again, Mr. Market also has yet to change his ways.

The very worst that will happen is a repeat of the past, when the price-earnings ratio contracted until Mr. Market finally noticed an improvement. This reinforces the idea that they “do not run the stock market for our benefit”. Ever since business school, when I first heard that, I have often wondered whose benefit the stock market runs for.

One thing that should improve valuation throughout the market cycle is the acquisition of all that refining capacity. Integrated companies are far less exposed to the volatility of the upstream business. In addition, the value-added part of the process is enhanced by using discounted products like thermal oil.

This company should show profitability advances over the next several years. But the results of that increased profitability could be delayed until the market is good and ready. Therefore, the value of those improvements to the market can value widely as shown on the stock price chart. That makes this idea one for patient buy and hold investors, as the stock price can be very volatile along the way.

Risks

A sustained and severe downturn in upstream prices can affect even an integrated company unfavorably. The result could be a materially different outcome than what was discussed above.

Any or all of the profit enhancement projects may not work out as planned. Cost overruns which affect the profitability of these projects are possible.

The loss of key personnel could prove consequential to the future prospects of the company.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Credit: Source link

{kind=link}