BestForBest/iStock via Getty Images

Investment thesis

The company’s management team has recently taken a series of steps to improve the financial stability of the company. Despite a significant share price decline since its Q1 earnings release where results were below management’s guidance, I believe certain key metrics point to the company’s platform gaining traction with its bank partners. According to my estimates, Cardlytics’ (NASDAQ:CDLX) shares are fairly valued at 26 times 2025 FCF. However the company does have multiple potential growth levers that could drive FCF materially higher than my estimates, owing to the company’s fixed cost business model. Nevertheless, high customer concentration and the risk for further shareholder dilution lead me to assigning a neutral rating to Cardlytics’s shares.

Brief recap of recent events

Debt refinancing and capital raise

The company’s CEO and CFO have been with the company since July 2022 and July 2023 respectively. Besides subsequently working on optimizing the company’s cost structure, the management team has recently refinanced the company’s debt by repurchasing its existing convertible note and replacing it with a $150 million convertible note, due only in 2029. The company also raised $50 million in an equity offering, which it used to resolve the dispute with SRS. These actions have left the company in a much healthier financial position, as highlighted by its CEO during the Q1 2024 earning call when he said:

With our capital needs addressed through our $50 million raise and new convertible notes not due until 2029, we are focused on higher growth rates. Our Q1 results and projected Q2 results continue to give us confidence. We have strong tailwinds behind us and we have scale that allows us to provide the best breadth and depth of offers for our banks and measurable outcomes for our advertisers.

To narrow its focus, management decided to sell its Entertainment business at the end of last year, which it had acquired in 2022 for $15 million in cash and stock.

Positive impact from the Ads Decision Engine

The company has been migrating its bank partners over to its Ads Decision Engine (ADE) which runs on AWS. ADE allows the bank’s customers to see more relevant and targeted ads. Banks on its ADE platform saw a 30 percentage point difference in redemptions last quarter, versus banks that weren’t. More than 80% of its bank partners are using ADE, and the company continues to upgrade the product to introduce further improvements.

Partnership with American Express

In March this year, the company entered into an agreement with American Express (AXP). This will enable Cardlytics to offer it marketing platform to American Express card members. The financial impact from this partnership still remains unknown, though the potential from American Express’s large customer base remains high.

Financial highlights

Created using company data

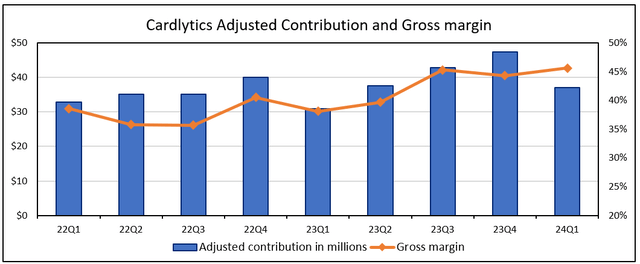

The company’s share price declined by nearly 40% following its Q1 earnings, as revenue and billings came in below management’s guidance. Most importantly, the company saw a sharp increase in adjusted contribution, which was up 20% year over year as shown above. This metric was within management’s guidance, and was exceptionally strong, as it was up 27% when adjusted for the loss of revenue from the divestment of Entertainment. Despite being a company specific metric, Adjusted contribution is the key metric that investors should focus on when tracking the profitable growth of the company. This was further highlighted by the company’s CEO when he said:

Adjusted contribution is an important metric that reflects our business performance as it is the money we keep from our billings after paying out customer rewards and bank revenue share.

The growth in contribution profit was mainly attributed to the strong growth in redemptions, which grew 20% year over year. This has been supported by renegotiated agreements with some of its major bank partners, as well as significant improvements in its technology, such as the addition of ADE. Additionally, the company’s marketing platform benefits from industry tailwinds as it offers a cookie-less identity solution.

Though adjusted EBITDA was $0.2 million in the quarter, operating cash flow was negative $17.6 million. Despite the fixed cost nature of its business model, management expects operating expenses to normalize around $40 million, compared to the current rate of $36.8 million a quarter. The expected increase is mainly driven by investments in technology and its growth initiatives.

Management’s guidance calls for 12% growth in billings in Q2, at the midpoint. Adjusted contribution is expected to be between $40 million to $45 million, which would be a growth of 13% at the midpoint. Beyond Q2, management expects growth rates to decelerate as they overlap some of the impact from re-negotiated contracts last year. Despite FCF being negative in Q1, management expects to be FCF positive in the second half of the year, together with full-year positive adjusted EBITDA.

Valuation

As the company continues to be unprofitable on a GAAP and FCF basis, it is difficult to value the business using traditional metrics. I therefore chose to base my valuation on 2025 estimates, where I expect double-digit year-over-year growth in adjusted contribution, from $180 million this year to around $200 million in 2025. Considering the company’s largely fixed cost model, I expect this to translate to FCF of around $15 million. At today’s share price of $8, this implies a Price to FCF of roughly 26. I consider shares to be fairly valued, given my expectation that FCF would likely double even with modest growth in adjusted contribution in 2026. This would imply a Price to 2026 FCF of approximately 13.

Despite my conclusion that shares are fairly valued, I believe there are multiple factors that could potentially drive further upside to my estimates. I will walk through some of these in the next section, and also highlight potential risks.

Potential growth drivers and risks that investors should consider

Strong growth in redemptions

Management views growth in redemptions as their North Star, as it believes it to be a leading indicator of demand for the product. Following a year-over-year growth of 20% in Q1, management expects strong growth in redemptions to continue in the upcoming quarters, as explained by its CEO when he stated:

So I think longer-term, you would see that as we continue to grow billings, we’re going to, hopefully, continue to drive a lot more redemptions, but we should keep more in adjusted contributions. So you’re going to see some differences in the economics for the business as a whole, but we think that we can manage that in a very healthy manner going forward.

Solid momentum in its international business

The company’s international business grew over 50% year-on-year last quarter, and management expects similar growth rates in upcoming quarters. The main factor driving this is the auto-enrollment program with Lloyds (LYG), where customers no longer have to opt in for its offers. Additionally, the company also signed a new bank partner, Monzo which is now live in the UK for its 8 million customers.

Revenue potential from Bridg and the American Express partnership

I believe Bridg as well as the potential from the American Express partnership provide future optionality, that is not reflected in the company’s valuation currently. In the case of Bridg, though revenue was up just 1% year over year in Q1, the company continues to onboard top regional grocers, such as the recent agreement with Giant Eagle’s Leap Media Group. Further additions like this will strengthen its Rippl network as it seeks to become an alternative in a cookie-less advertising world.

Despite the uncertainty regarding the magnitude of the impact from the partnership with American Express, even a modest revenue contribution could significantly boost the company’s profitability, as it would involve minimal incremental cost.

Dependency on large banks

There are currently no competitors with a product offering like what Cardlytics has. Despite this, one of the biggest risks that the company faces is customer concentration, with the top three banks representing 85% of the bank partner contribution in 2023. If one of these large banks reduces its focus on the Cardlytics platform or chooses to leave the platform entirely, it could have a significant impact on the company. In 2022, one of its largest clients, JPMorgan Chase (JPM) acquired Figg, with the aim of bringing a similar solution in-house. Though this sort of risk is yet to play-out in the company’s numbers, it is something investors should watch out for.

Shareholder dilution

Besides the risk of increased dilution due to the $150 million convertible notes due in 2029, investors also face the risk of dilution due to high stock-based compensation. Stock-based compensation for the TTM was roughly $40 million, which is more than 10% of the company’s current market cap.

Conclusion

Cardlytics shares are fairly valued based on my current estimates. However there are multiple growth levers for the company, which, if successful, could drive profits significantly higher than my estimates owing to the company’s fixed cost business model. However the significant risks that I’ve highlighted above make me stay with a Neutral rating.

Credit: Source link

{kind=link}