franckreporter/iStock via Getty Images

Investment Thesis

AI has had, no doubt, a prolific impact on enterprises, influencing the decisions of the enterprise’s CIO office and how they allocate their IT budgets. Per Bloomberg Intelligence estimates, the impact on IT budgets, which was estimated to be under 1% in FY23, will grow to a reported 5% in FY26 and possibly to 12% in FY32.

C3.ai (NYSE:AI), the maker of the full-stack enterprise AI platform, is one such company that operates in the enterprise AI applications space. The company is set to report its earnings on Wednesday, May 29, 2024, next week after markets close. As C3 AI heads into earnings next week, it needs to overhaul its approach towards acquiring customers. Per my analysis, the company spends at least nine-tenths of its revenue generated on acquiring customers, which is a steep price to pay to acquire customers, in my opinion.

I will initiate my ratings on C3.ai by recommending a Sell on the company with its full year FY24 earnings around the corner.

Note: I will be referring to C3.ai as just C3 throughout this research note.

About C3’s business model transition

C3 bills itself as the maker of enterprise AI application platforms that its enterprise clients can use to build, deploy, and scale their own individual AI applications. According to S1, C3 offers their model-driven architecture via their C3 AI suite to scale applications. In my view, C3 aims to provide drag-and-drop functionality to build and scale AI applications, removing the need for some enterprises to hire full-time developers.

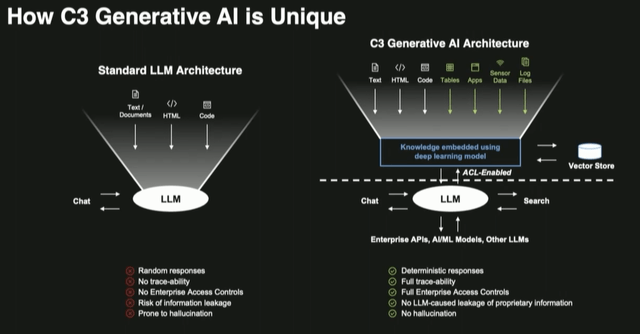

In the AI age, C3 has delves deeper by offering its C3 GenAI architecture to enterprises to build their own GenAI applications based on the architecture mentioned below in Exhibit A. The architecture model taken below is a screenshot from their Investor Day presentation last year.

Exhibit A: How C3 differentiates its GenAI architecture vs other AI Architecture (FY23 Investor Day Presentation, C3.ai)

The Redwood City, CA-headquartered company leans heavily on its sales pipeline by partnering with consulting companies, system integrators, point solution companies, and hyperscalers to acquire customers.

The company generates revenue by selling ~3-year subscription plans, which, according to its FY23 10-K, accounted for 86% of its total revenue. In addition, the company also generates incremental revenue from usage-based pricing.

C3 needs to address its soaring cost of customer acquisition

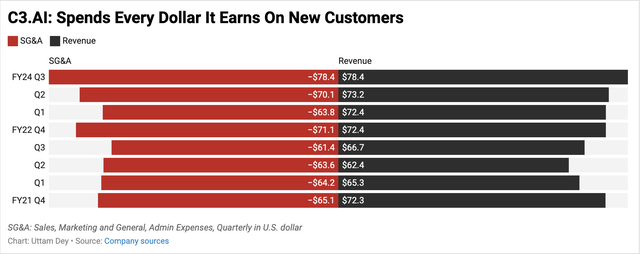

As the company heads into next week’s earnings, it needs to severely address its customer acquisition costs, which continue to grow in line with its revenue, as seen in Exhibit B below.

Exhibit B: C3 spends almost every dollar it earns to acquire new customers (Company sources)

As seen from Exhibit B above, C3 spends almost every dollar it generates in revenue to acquire new customers. In my view, this is not a healthy sign of demand. In the Investor Day presentation last year, management noted they were seeing improvement in their sales processes as “sales pipelines doubled” and “sales cycles decreased by 20–30%,” which was leading to improved sales productivity for the company.

From Exhibit B above, it appears the company spends ~90 cents to acquire every $1 in additional revenue on average. In the last quarter, it got even worse, where the company spent all of its revenue generated in Q3 FY24 on Sales, Marketing expenses. Therefore, per my observation, since management made their comments on doubling sales pipelines on Investor Day last year, SG&A expenses have increased since then. In fact, on a y/y basis, while revenue in Q3 increased 17.5%, SG&A increased 27.6%.

In the past, management has not shied away from doubling down on their cost-intensive method of focusing on enterprise sales to generate leads and customers. At Needham’s TMC Conference last week, management mentioned that “we have to pay our dues to get the door” when responding to a question on industry-specific sales strategy. In the Q3 earnings call last quarter, here is what management had to say about ramping up their sales teams:

So, the sales, we are still hiring actively in all of our sales functions, but not as fast as we’d like. So our sales force is not as high as we initially projected when we provided these sort of assumptions, but we continue to ramp up on that.

A reasonable assumption would be 1.5, 2 quarters before they get fully ramped up and get going on closing their first pilots.

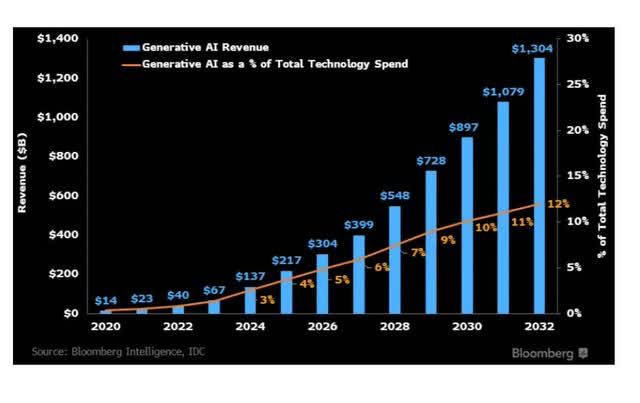

Moreover, the growth rate seems to be slower than the overall growth rate as projected by Bloomberg Intelligence’s market report on the projected sales of enterprise AI applications, as seen in Exhibit C below.

Exhibit C: C3 spends almost every dollar it earns to acquire new customers (Bloomberg Intelligence)

As seen in the exhibit above, per the report, GenAI revenue is estimated to grow at a 76% CAGR between FY20 and FY24. In contrast, C3’s revenue has grown at just 18.5% CAGR. For a company that beats the drum about GenAI, this seems quite tepid, in my opinion.

C3 Customer Mix Is Still In Transition State

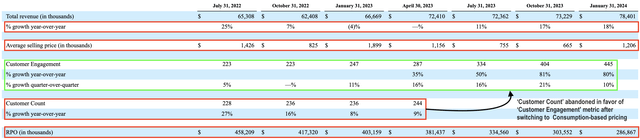

Upon deeper inspection, I note that the company has an unfavorable customer mix that may be impacting the company’s revenue trends indirectly. Per its Q3 FY24 10-Q, two of its customers accounted for at least 45% of its revenue. All other customer metrics that the company deemed operational metrics earlier do not make sense to track any more after management switched gears from implementing a consumption-based pricing model. Therefore, the falling trends seen in Remaining Performance Obligations and Average Selling Price are worth noting for now, but may not make sense to look at down the road. Nevertheless, I have added this to Exhibit D below.

Exhibit D: C3’s customer trends and RPO trends (Q3 10-Q, C3.ai)

I believe most of the customer mix may be due to the contracts it receives via its sales contracts with its integration partners Baker Hughes (BKR), one of the world’s biggest oil field contractors, and RTX Corp. (RTX), an American multinational aerospace and defense conglomerate.

Management seems to be now focusing on capturing customers in the defense industry. Per an Q3 earnings call, management mentioned that defense now accounts for ~15% of its total revenue. Here’s an excerpt from that call:

Our US federal business continues to show significant strength. Third quarter revenue was up over 100% year-over-year, and bookings were up 85%. We signed new and expansion agreements with the Missile Defense Agency, the Department of Defense, the United States Air Force, and the US Intelligence community, including seven new generative AI agreements at the Missile Defense Agency, the United States Air Force, JROC, and the US Marine Corps.

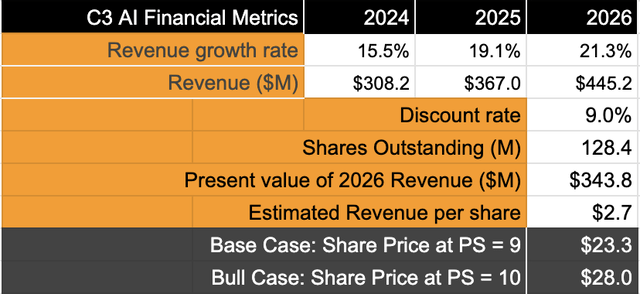

C3 is overvalued heading into Q4 earnings

As the company heads into Q4 earnings, C3 looks overvalued. Here are my assumptions:

- In terms of revenue, I expect the company to grow in double digits, buoyed by its high customer acquisition costs. The growth rates are in line with consensus expectations and the mid-term model. There might be a moderate deceleration in costs this year, but it is highly unlikely it will have a meaningful impact on margins.

- Due to this outlook, I will also resort to estimating my target price using sales forecasting in lieu of any operating profit history, GAAP or non-GAAP. Based on my estimates, I project C3 to grow its revenue by ~18.6% CAGR between FY23 and FY26.

- I expect management will see a ~4.5% CAGR in share dilution rates. Between FY21 and FY23, shares outstanding have been diluted by 5.5% CAGR. I expect that to slightly moderate over the next three years as management will continue to dilute shares to fund its business expansion plans.

- I have used a discount rate of ~9%, with assumptions for the rate listed here.

Exhibit E: C3.ai’s stock is overvalued at current levels (Author)

Based on my model’s Base case scenario, I believe C3 commands a forward sales premium of ~9x, which shows there is ~10-11% downside if I compare C3’s sales growth to the long-term growth rates of the S&P 500.

Even in the Bull case scenario, if management is able to deliver a beat and raise, I project sales growth to rise to ~20.3%, which should imply a forward sales multiple of ~10x. This would suggest a 5-6% upside in stock from here, but I am highly doubtful these gains would last because the company has some fundamental issues in its sales model that need to be fixed before it can return to sustainable growth mode.

What To Look For in Q4 Earnings

- Business Operational Metrics: Management has abandoned most of their operation metrics, such as RPO, ASP and Customer Count as highlighted in Exhibit D. Metrics such as Bookings will help to understand forward trends rather than depend on management’s verbal commitments.

- Sales costs: Management has guided to higher sales expenses in the past. Any pointers on when the intense sales-fueled revenue growth will end will be appreciated.

- Guidance: Per consensus expectations, Q1 FY25 revenue is expected to be $85.89 million, up 18.7% y/y while non-GAAP EPS loss is expected to be -15 cents. For the full year FY25, the company is expected to lose 66 cents per share on revenue worth $367.5 million.

- Q4 Numbers: Finally, the company is expected to lose 30 cents per share on Q4 FY24 revenue worth $84.4 million. That should translate to the company losing 66 cents per share on revenue of $308.4 million. This is in line with management’s guidance, where they expect Q4 revenues to be ~84 million and full-year FY24 revenue to be ~$308 million at the midpoint of their guidance.

Note: the company has had a series of turnover in its CFO chair. This Bloomberg report summarizes all the changes in the CFO position of the company with the most recent change coming this year.

Caution: Investors should also note that the company is currently of particular interest among short-sellers, with over 30% of its shares outstanding being shorted. Short sellers such as Spruce Point and Kerrisdale Capital have issued research notes shorting the company’s stock. This may create distorted volatility in the company’s stock, which may affect fundamentals.

Takeaway

With the risk/reward not appetizing enough, heading into Q4 earnings, I believe the company’s stock is significantly exposed to sizable risk given the fundamentals of its business. I am not encouraged by management commentary or the steps they are taking to rectify business fundamentals, and thus I will initiate a Sell rating on C3.

Credit: Source link

{kind=link}