JHVEPhoto

Broadcom (NASDAQ:AVGO) (NEOE:AVGO:CA) reported results for the second quarter on 13th of June, and broadly topped analysts’ consensus: Revenue jumped 43% YoY, while adjusted EBITDA surged 59% YoY. Following the earnings announcement, AVGO shares surged by about 15%, to a record >$800 billion market capitalization. Broadcom stock has rallied more than 200% since I covered the stock in January 2023, assigning a “Buy” rating. While I still believe in the core thesis that Broadcom is a key beneficiary of the GenAI CAPEX investment cycle, I turn more pessimistic in the assessment about whether AVGO stock is a “Buy” — mostly as a function of valuation, with shares trading at >35x P/E and >20x P/B. As a function of valuation anchored on a residual earnings model, I downgrade AVGO shares to “Hold” and set my target price at $972.

For context: Broadcom stock has significantly outperformed the broader U.S. stock market this year. Since the beginning of the year, AVGO shares are up by approximately 55%, compared to a gain of about 14% for the S&P 500 (SP500).

Seeking Alpha

Broadcom Beats Q2 Estimates

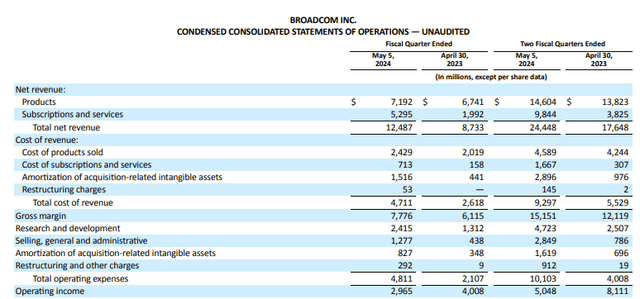

On Thursday, June 13th, Broadcom released its financial results for the second quarter, topping Wall Street’s expectations in both revenue and earnings. During the period spanning from February to the end of April (May 5th, actually), the semiconductor and communication infrastructure giant reported sales of approximately $12.5 billion, up 43% YoY and approximately $500 million above consensus estimates, according to data compiled by Refinitiv. Product revenue stood at $7.2 billion, reflecting a 7% YoY growth, while subscription revenue surged by 165% YoY, to $5.3 billion (now accounting for 42% of sales).

In terms of profitability, Broadcom’s operating margin at the group level came in at 23.7%, with the company reporting an operating income of approximately $3 billion, compared to $4 billion for the same period one year earlier. Headwinds to profitability were mostly related to high quality OPEX such as R&D (reported at $2.4 billion, up $1.1 billion) and SG&A ($1.3 billion, up $0.9 billion).

Broadcom Q2 Reporting

After accounting for roughly $1.8 billion in non-operating and tax expenses, Broadcom reported a net income of about $2.1 billion, equating to earnings of $4.42 per share. Although Broadcom’s net income was down compared to the $3.5 billion reported one year earlier, results exceeded analyst expectations by about 10%, according to data collected by Refinitiv.

Bullish Outlook for FY 2024

Together with Q2 results, Broadcom also provided guidance for the remainder of 2024: On a full-year basis, management now expects revenues of about $51 billion, which would imply a 42% YoY topline increase compared to the prior year period. On profitability, Broadcom guided for a 61% EBITDA margin, which would suggest $31 billion of operating profits (excluding D&A).

10-For-1 Stock-Split

Other highlights relating to Broadcom’s earnings reporting include the announcement of a ten-for-one forward stock split. On that note, while the stock split does not create economic value, the move could boost investor sentiment on improved trading liquidity for options contracts. The stock split will materialize on July 12, 2024, after market close.

Strong AI Momentum Drives EPS Upgrade Cycle

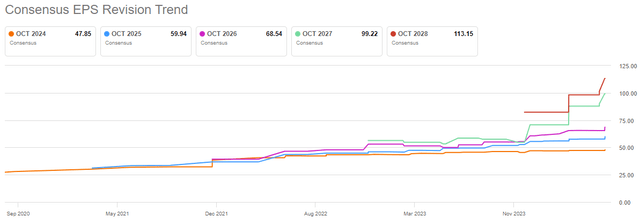

Over the past 12-24 months, Broadcom has enjoyed a strong upgrade cycle in EPS estimates (see below), with analysts expecting as much as $100 of earnings per share by FY 2027, compared to $48 earnings per share in FY 2024 (28% EPS CAGR).

Seeking Alpha

Pointing to the bullish consensus momentum, I highlight that the earnings revision cycle is primarily driven by positive AI exposure. In fact, Broadcom’s networking segment is poised to benefit from hyperscalers’ shift towards increasingly diverse data center ecosystems and the growing demand for custom compute chips. On that note, I am especially bullish on AVGO’s ASIC opportunities, with major customers including Google (GOOG) and Meta Platforms (META).

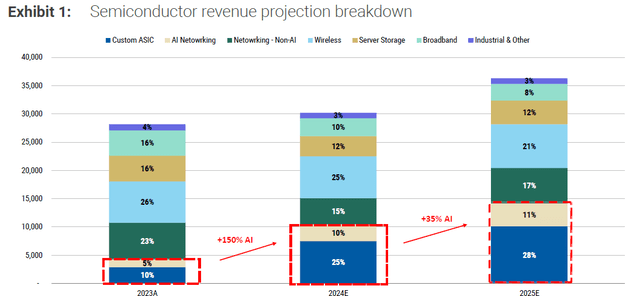

Fueled by (1) the integration of Ethernet in AI data centers, (2) the continuous expansion of Google’s TPU, and (3) the onboarding of two new ASIC customers, the research team at Morgan Stanley projects Broadcom’s AI revenue to jump to $14 billion by FY 2025, up from $4.2 billion in FY 2023 (Source: AVGO research note dated June 9th: “Resume coverage of AVGO at OW as one of the strongest AI plays”).

Morgan Stanley

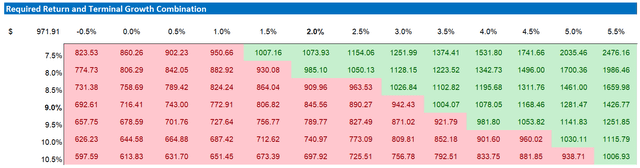

Valuation Update: Raise TP To $972/ Share

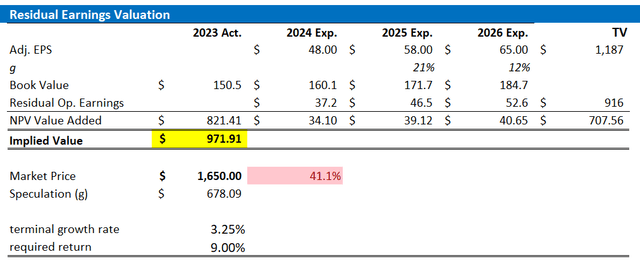

Following a stronger-than-expected earnings momentum over the trailing twelve months, I am revising my valuation assumptions for Broadcom stock. With estimates anchored on analyst consensus estimates, with adjustments of +/- 10%, I now project Broadcom’s earnings per share for FY 2024 to range between $47 and $49 (non-GAAP). Additionally, I forecast these earnings will rise to $58 in FY 2025 and $65 in FY 2026. Beyond FY 2026, I anticipate a compound annual growth rate in earnings of approximately 3.25%, which is about 100 basis points above the projected nominal GDP growth and likely conservative. I am maintaining my cost of equity assumption at 9%. With these updates, I now assess the fair value of Broadcom stock at $972, a significant increase from my previous estimate of $693, but well below Broadcom’s current market trading price.

For context, the value “Speculation” is just the difference to fair implied value. A positive value implies a premium; or in other words, markets are speculating to price more fundamental upside compared to my estimates.

Company Financials; Refinitiv Estimates; Author’s Calculations

Below also the updated sensitivity table.

Company Financials; Refinitiv Estimates; Author’s Calculations

Investor Takeaway

Broadcom exceeded Q2 estimates with a 43% YoY revenue increase and a 59% YoY surge in adjusted EBITDA. The company has a bullish outlook for FY 2024, projecting revenue to reach $51 billion and an EBITDA margin of 61%. Broadcom’s commercial momentum remains strong, driven by hyperscalers’ shift towards increasingly diverse data center ecosystems and growing demand for custom compute chips. While I believe Broadcom is well-positioned to benefit from the GenAI CAPEX investment cycle, I am concerned about AVGO’s valuation, which stands at over 35x P/E and over 20x P/B. As a function of valuation anchored on a residual earnings model, I downgrade AVGO shares to “Hold” and set my target price at $972.

Credit: Source link

{kind=link}