AvigatorPhotographer

Note:

I have covered Borr Drilling Limited (NYSE:BORR) previously, so investors should view this as an update to my earlier articles on the company.

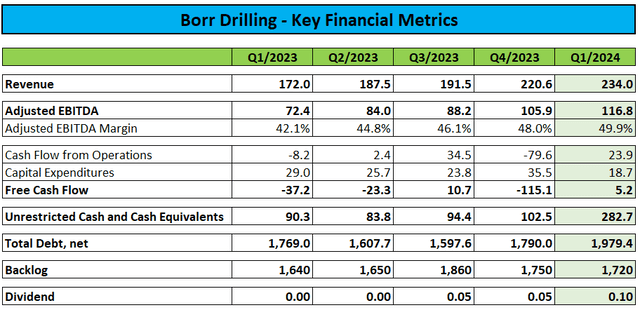

Last month, leading offshore driller Borr Drilling reported Q1/2024 results somewhat below estimates due to a combination of slightly lower-than-expected revenues and higher financial and tax expenses:

Company Press Release / Regulatory Filings

Operating cash flow generation for the quarter was impacted by higher working capital levels resulting from “late invoicing for certain contracts“, as outlined in the press release. However, the company still managed to squeeze out a small amount of free cash flow but this was more than offset by $23.8 million in dividend payments and $10.6 million used for the repurchase of convertible debt.

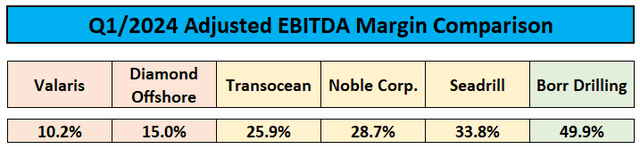

Adjusted EBITDA margin of 49.9% reached new all-time highs with the company outperforming peers handsomely:

Company Press Releases

However, the company remains highly leveraged.

Borr Drilling ended the quarter with unrestricted cash and cash equivalents of $282.7 million and $1,979 million in debt, up from $102.5 million and $1,790 million at the end of last year with the increases resulting from the issuance of an additional $200 million 2028 10% Senior Secured Notes in February.

As a result, total liquidity increased to $432.7 million from $252.5 million at the end of Q4/2023.

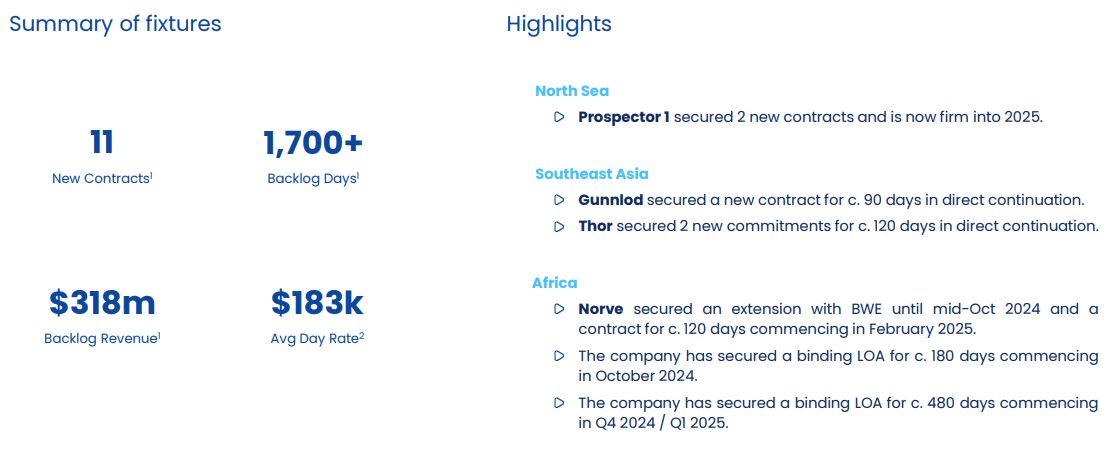

Backlog was down slightly to $1.72 billion. Year to date, the company has been awarded eleven new contract commitments with an aggregate value of $318 million and an average dayrate of $183,000.

Company Presentation

In the press release, Borr Drilling confirmed a clean dayrate of above $200,000 for a recently announced binding letter of award:

Notably, in the second quarter, we achieved our first-ever contract exceeding $200,000 per day on a clean day rate basis.

This milestone not only underscores the premium quality and operational excellence of our fleet, but it is a positive confirmation of our views of a well-balanced market despite the recent developments in Saudi Arabia.

Based on statements made in the earnings release and on the conference call, it seems fair to assume that the newbuild rig Vali which is scheduled for delivery in October will be deployed under this contract.

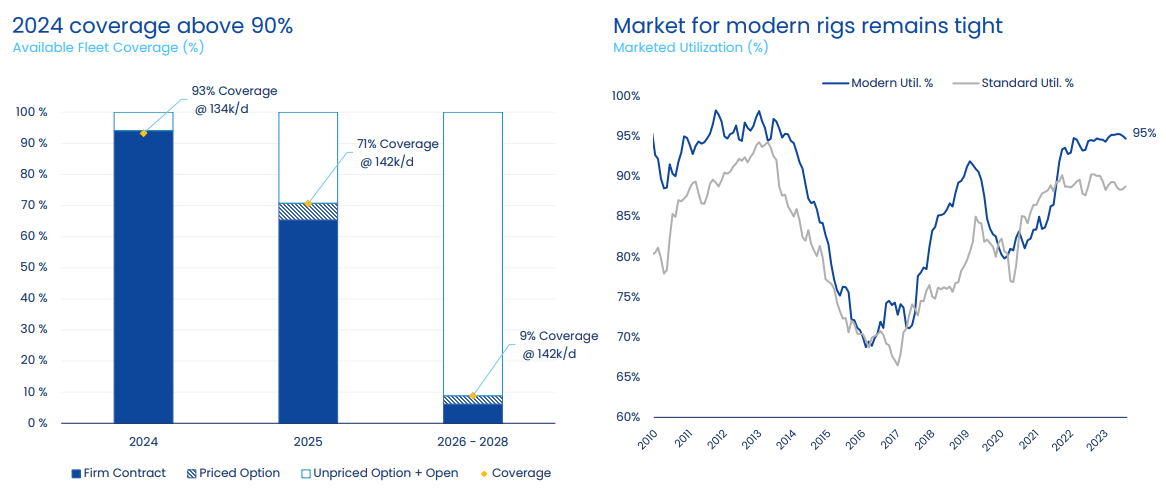

As a result of the most recent awards, contract coverage for 2024 (including priced options) has increased to 93% (previously 87%) with an average dayrate of $134,000.

Contract coverage for 2025 has lifted from 64% to 71% with the average dayrate moving from $134,000 to $142,000:

Company Presentation

On the call, management remained optimistic on the jackup market environment despite potential near-term disruptions from Saudi Aramco’s (ARMCO) recent decision to suspend 22 jackup rigs, including Borr Drilling’s Arabia I rig (emphasis added by author):

On a broader market perspective, utilization for modern jack-ups remains strong at approximately 95%, not adjusted for Aramco’s suspension of the 22 rigs, including our Arabia I. We note that some of the suspended rigs have already been re-contracted elsewhere, while others may not be competitive international markets due to their vintage capability, lack of international footprint of their current operators.

We anticipate that around 13 of these rigs are potentially competitive international market, which would result in utilization remaining at healthy levels above 90%. However, we see this fluctuation utilization to be temporary as incremental demand levels should offset and surpass the number of rigs potentially available in Saudi Arabia. Based on the current tenders and discussion with our customers, we continue to project incremental demand of 20 rigs to 25 rigs within the next 12 months to 18 months.

On that note, we remain optimistic about our ability to re-contract the Arabia I during the third quarter. While we have witnessed some competitor fixtures below general market rates in certain geographies, we expect this dynamic should be short-lived as fundamentally the jack-up market remains well-balanced and tight.

The company reiterated expectations for full-year Adjusted EBITDA of $500 million to $550 million.

Perhaps most importantly, the company doubled its quarterly cash dividend to $0.10 per share and projected further increases over time:

Lastly, the Board approved a doubling of the quarterly dividend to $0.10 per share, reflecting a positive outlook. We would expect the dividend to continue increasing over time in line with our earnings outlook.

While I would like Borr Drilling to focus more on reducing its sizeable leverage, the generous dividend increase should be considered a strong sign of confidence in the company’s outlook going into 2025 and beyond.

At current share price levels, annualized dividend yield calculates to 6.5%.

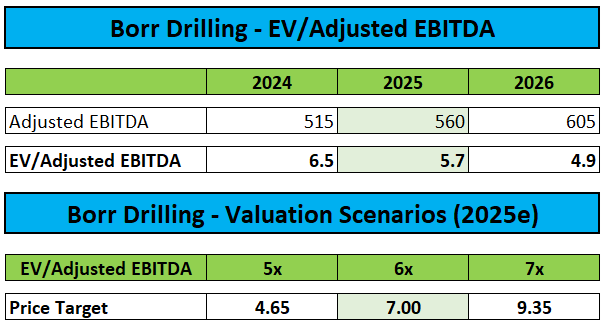

Following the strong contracting activity so far this year in combination with encouraging market commentary by management, I have increased my estimates but remain well below my original assumptions to account for potential Saudi Aramco impact:

Company Projections / Author’s Estimates

While the stock’s industry-leading 6.5% dividend yield looks appealing, limited upside to my increased $7 price target is keeping me from upgrading the stock at this point.

However, I would become more constructive on Borr Drilling should the share price move back below $5.80.

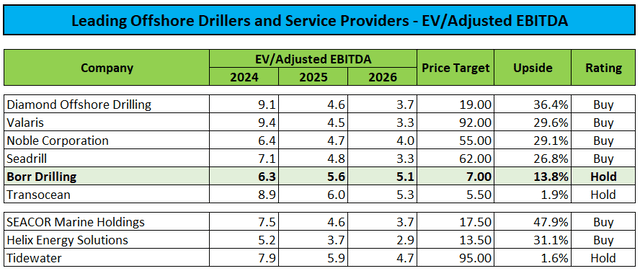

Investors looking for exposure to the offshore drilling industry should consider peers like Diamond Offshore Drilling (DO), Valaris (VAL), Noble Corporation (NE) and Seadrill (SDRL) which are all trading at substantially lower forward valuations while commanding vastly superior balance sheets.

Author’s Estimates

Please note that offshore support vessel provider SEACOR Marine Holdings (SMHI) provides for even higher upside.

Bottom Line

Borr Drilling reported slightly weaker-than-expected Q1 results and reiterated full year guidance as management remained optimistic on jackup market conditions even in light of some potential near-term fallout from Saudi Aramco.

The company has managed to secure additional contracts at decent rates in recent months thus further increasing earnings visibility for the remainder of the year and going into 2025.

To reflect the positive outlook, Borr Drilling decided to double the quarterly cash dividend to $0.10.

While management’s commentary and commitment to shareholder capital returns is encouraging, my upwardly revised estimates and price target are not sufficient to upgrade the stock.

As a result, I am reiterating my “Hold” rating with an increased price target of $7 based on an assigned multiple of 6x the company’s projected 2025 EV/Adjusted EBITDA.

However, I would become more constructive on Borr Drilling should the stock price move below $5.80.

Credit: Source link

{kind=link}