bashta

When Bonterra Energy (OTCPK:BNEFF) reported the first quarter results, those results appeared to take a step backward because natural gas production was a larger part of the mix. At least part of those results was influenced by a very cold winter, causing some shut-in. But the acquisition mentioned in the first quarter report of some Charlie Lake acreage demonstrates that management will continue to replace natural gas production (as discussed in the last article) in the product mix with more valuable liquids production while also growing overall production for the first time in years.

It may also be why this company barely managed a profit, while many gas producers I followed were shutting in production to try to get to a profitable quarter.

First Quarter Results

This primarily natural gas producer was affected by lower natural gas prices, even though the liquids value is now most of sales (in terms of Canadian dollars). The small number of liquids produced was enough to keep the company from running a large loss (which would have been the case with dry gas production).

(Note: Bonterra Energy is a Canadian company that reports in Canadian dollars unless otherwise stated.)

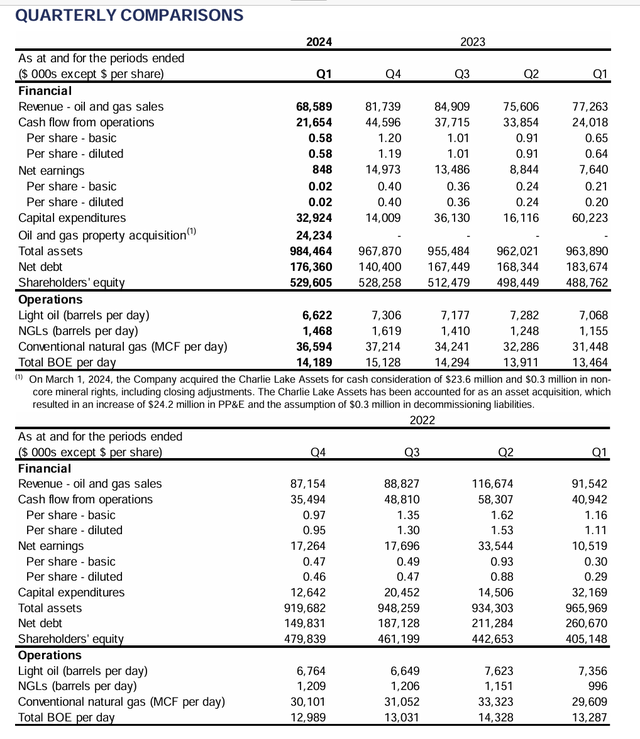

Bonterra Energy Summary Of First Quarter Operating Results (Bonterra Energy First Quarter 2024, Management Discussion And Analysis Filed With Sedar)

The lower commodity prices resulted in considerably less cash flow, which would raise the debt ratio considerably should the situation continue for the whole fiscal year. However, management has had the ability for some time to drill liquids rich acreage that should blunt the effects of the worst-case scenario.

Stock Price Action

The stock price has been weak because the first quarter comparisons were lack-luster, and the second quarter has the seasonal Spring-Breakup. Combine that with worries about a recession that have dominated the headlines for a few years (and what that would do to commodity prices) and you have the perfect scenario for a lagging stock price.

However, the changing product mix should offset any negative factors by increasing the company’s profitability at various pricing points. This company will be repaying debt with any free cash flow. Therefore, there will not be much of a priority to return cash to shareholders in any form, probably for a couple of years. This should, instead, be a turnaround story that should morph into a growth story.

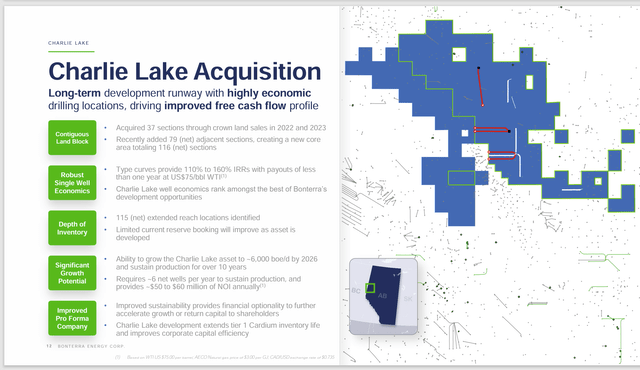

Charlie Lake Acquisition

This acquisition continues the trend that relatively new management has started towards drilling more profitable wells. There has been a kind of “tug-of-war” between this and the dry gas business because there have been some remarkable improvements in dry gas areas in Canada that resulted in extraordinary returns for some dry gas wells.

But most managements, like this management, appear to prefer the flexibility of the rich liquids areas to cater to a larger variety of commodity price scenarios.

Bonterra Energy Summary Of Charlie Lake Acquisition Prospects (Bonterra Energy First Quarter 2024, Corporate Presentation)

The summary given above is for the acreage acquired. Left out of the conversation is the fact that additional acreage is often very cheap in Canada, even in “hot” basins. While management has a peak production planned for this acreage, that can easily be expanded by acquiring more acreage if the purchase works out as planned. As a result, for many companies, the Charlie Lake area contains future production growth possibilities. Time will tell if that is the case here.

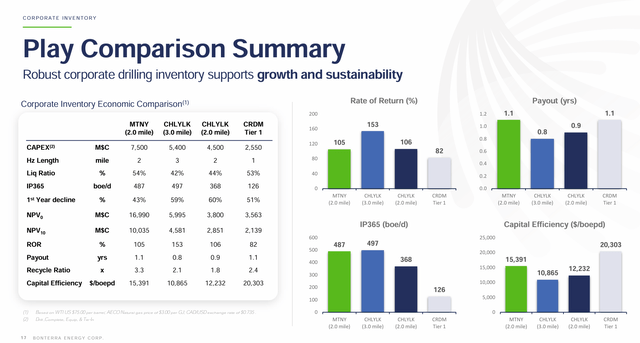

Portfolio Comparisons

As the below slide demonstrates, management has considerably improved the future drilling return choices over the original company business.

Bonterra Energy Summary Of Portfolio Returns And Profitability (Bonterra Energy First Quarter 2024, Corporate Presentation)

The results above should mean that the company generates more cash flow given the same commodity price levels than was the case in the past. Now whether this is worth the debt taken on remains to be seen as the new acreage does not yet have enough history to verify the figures shown above.

But there are many established competitors reporting the same thing. Therefore, the steps taken by management would appear to be logical.

What adds to the upside is the coming growth in North American ability to export natural gas. This may lead to the natural gas market in North America joining the world market. That would give this company some flexibility that is not really a part of the current corporate presentation. It is a potential upside scenario that evidently management is not banking on for the time being.

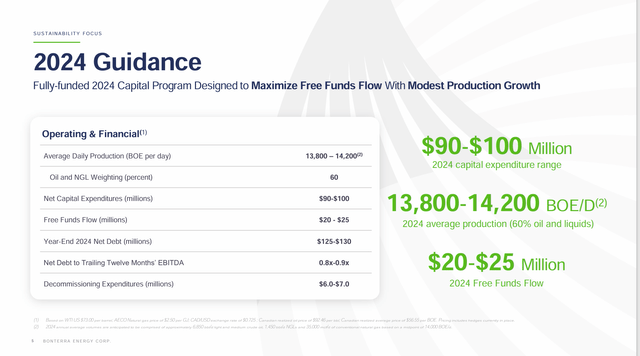

Guidance

The latest guidance assumes a continuing production mix improvement towards more valuable liquids production.

Bonterra Energy Fiscal Year 2024 Guidance (Bonterra Energy Corporate Presentation First Quarter 2024)

One of the things to remember is that the transition to more liquids itself will not increase things like profitability and free cash flow if the wells drilled to get there have low returns.

Therefore, the profitability of each well drilled will be critical for that free cash flow mentioned above. Canada itself has a lot of conventional opportunities using “modern completion techniques”. Therefore, the first-year declines shown before are not that unusual in Canada, even though they are lower than unconventional in the United States. This lower decline changes the cash flow picture considerably because there is a greater flow rate starting in the second year of production.

The difference between conventional and unconventional is of course clear to the company personnel (it is a porosity definition). But for the average investor, well costs and completions sort of blur the difference as they are becoming similar for both types of businesses.

Summary

Bonterra Energy is a company in transition from essentially a natural gas producer to more liquids production. Some would state that the company has already “gotten there”. But there is still the relative debt load compared to the EBITDA and free cash flow. Management appears to have the tools in place to properly “deal with” those issues.

Investors with some patience can consider this a strong buy, as the market has ignored the considerable management progress made so far. The “ignoring” is likely due to the relatively high debt load compared to what the market prefers.

As long as the results continue to go in the right direction, this stock should respond to the progress made by the relatively new management.

Risks

Any upstream company is subject to the high volatility and low visibility of future commodity prices. A company with perceived relatively high debt like this one needs some commodity price cooperation that it may not get in the future. Any sustained and severe commodity price downturn could materially change the future outlook of the company.

With any small company, the loss of key personnel can materially set back the future plans of the company. Small companies do not have the resources that larger companies have to offset the loss of a key person.

Any acquisition can turn out to be a future disappointment compared to management expectations. There is no exception to that here. Reducing the risk is that the acreage acquired is in an area that management knows well, and that others have likely derisked to some extent.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Credit: Source link

{kind=link}