paulprescott72

Africa Oil Corporation (NYSEARCA: OTCPK:AOIFF) has numerous exciting assets, however, at the end of the day, it has a single producing asset. That asset is a 50% shareholding in Prime Oil and Gas and it’s associated offshore Nigerian production. That asset had substantial debt, with dividends paid to the parent companies. As we’ll see throughout this article, the company’s consolidation moves will enable strong shareholder returns.

Africa Oil Corporation New Strategy

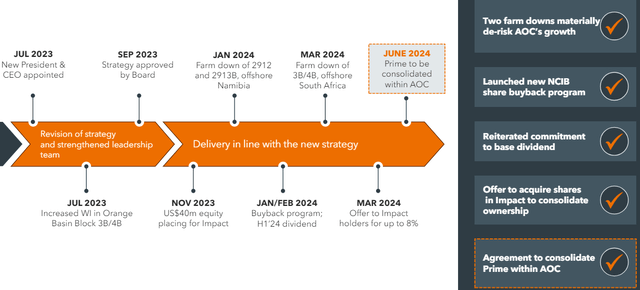

Africa Oil Corporation revamped its strategy in mid-2023 and over the past year has worked to focus on its growth potential.

Africa Oil Corporation Investor Presentation

That includes two farm downs to de-risk the company’s growth prospects, along with an equity investment placing for Impact. The company has also continued to pay a reasonable dividend of roughly 3% and has continued to buyback shares, buying back $40 million USD of shares or ~5% of its outstanding float. It can repurchase up to 10% of shares.

That, combined with the proposed consolidation we’ll see below, will enable continued long-term growth and shareholder returns.

Africa Oil Corporation Proposed Consolidation

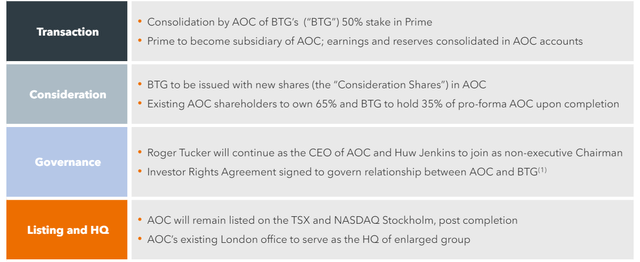

The company is consolidating with BTG, specifically BTG’s 50% stake in Prime Oil and Gas.

Africa Oil Corporation Investor Presentation

That will result in Prime Oil and Gas becoming a subsidiary of AOC, with all earnings and reserves going straight to AOC. As a result, BTG will have a 35% growth through the issuance of new shares. The $800 million USD company will grow to a $1.2 billion USD company, valuing the company’s Prime Oil and Gas assets at $800 million.

Africa Oil Corporation Investor Presentation

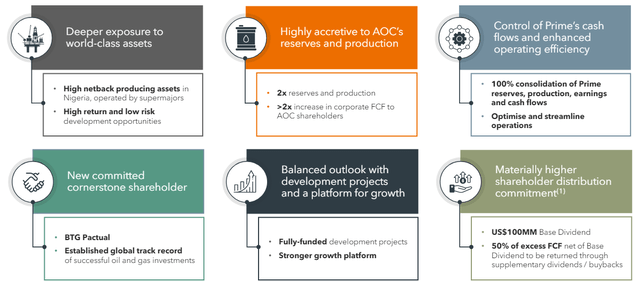

The deal provides immediate cash flow from strong Nigerian assets that have strong long-term growth potential. It doubles the reserves and production of the company and enables streamlined financial reporting and an increase in FCF to shareholders. The company is now committed to a $100 million USD base dividend, or a high single-digit yield of more than 8%, along with stronger overall returns.

That doesn’t count the company’s strong buyback program or its excess FCF that it can utilize for shareholder returns.

Africa Oil Corporation Asset Overview

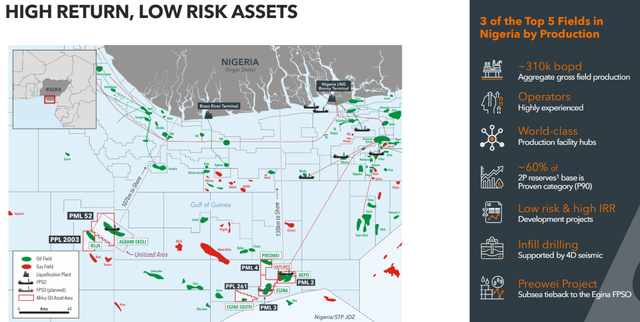

The company has strong assets in Nigeria, assets that it will now have full ownership of, partaking in 3 of the top 5 fields in Nigeria by production.

Africa Oil Corporation Investor Presentation

The 3 fields have ~310 thousand barrels / day in aggregate gross field production with experienced operators. The vast majority of the company’s reserves are proven, with continued development opportunities, and products such as Preowei to expand production. The company expects 2024 production to be a pro forma 36k barrels / day, with an 8-year reserve life.

The assets have generated $850 million in dividends in the last 4 years alone, and that dividend production is expected to remain strong. Pro forma year-end net debt will be $365 million, a comfortably affordable level from Prime, and one that can be managed. At current prices, Prime Oil and Gas earns more than $700 million in annual EBITDA.

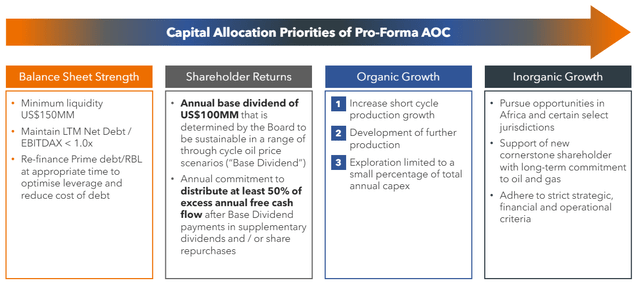

Africa Oil Corporation Shareholder Returns

Africa Oil Corporation will have a strong pro-forma balance sheet committed to substantial shareholder returns.

Africa Oil Corporation Investor Presentation

The company expects to maintain at least $150 million in liquidity while maintaining LTM net debt / EBITDAX at <1.0x. The company plans to re-finance Prime debt / RBL, and we expect the combined structure will make that much easier for the company. The company is committed to hefty shareholder returns with $100 million in base dividends + 50% of excess FCF.

That’s a dividend yield of more than 8%, plus continued shareholder returns, through buybacks. The company has exciting organic growth opportunities, with minimal risk due to its farm-down transaction. At the same time, the company is still looking for alternative long-term growth opportunities, something worth paying close attention to, given its historical success here.

Thesis Risk

The company’s largest risk is weakness in oil prices as long-term demand tops out and low-cost competition exists from numerous sources such as American shale. That could hurt its ability to generate returns from its existing assets, while slowing down its ability to develop new assets. That’s worth paying close attention to.

Conclusion

Africa has long been an unpopular jurisdiction for oil companies to invest in, with instability presenting a major risk. That’s visible through the company’s original project, Kenya, which was never built due to an inability to raise the necessary capital for a takeaway pipeline. That’s combined with long-term growth concerns as oil demand remains weak and cheap production arises.

The company is issuing 35% more equity, to BTG, to enable it to take full ownership of Prime Oil and Gas. That will move the company to a net debt position, but enable it to grow substantially and have additional cash. The company is planning to move to a more than 8% debt load plus additional share buybacks. All of that makes the company a valuable investment.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Credit: Source link

{kind=link}