olaser

The final two weeks of September may see liquidity, which is already strained, fall even more. End-of-quarter changes in the Fed’s reverse repurchase facility usage are likely to rise from their recent lows, while the Treasury’s General Account held at the Fed is likely to increase. Both will lead to declining bank reserve balances held at the Fed, which could lead to an overall deterioration in market liquidity.

Additionally, the Bank Term Funding Program will continue to decline over the coming months as it returns to zero. We saw significant growth in the program’s usage in the fall of 2023, and the program could soon begin to decline faster as we overlap that period.

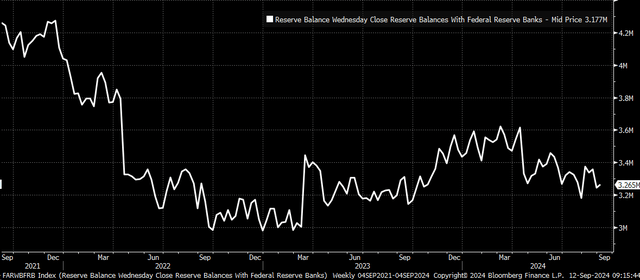

Declining Reserves Expected

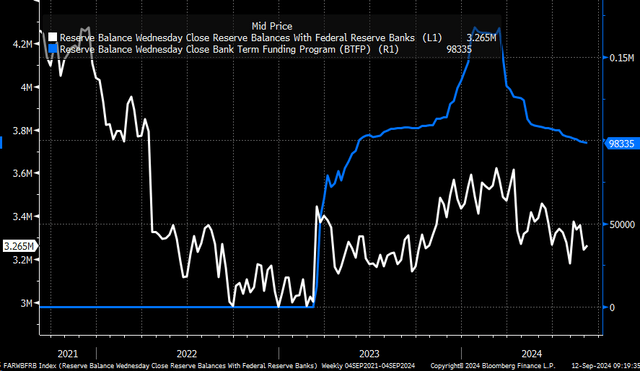

Reserve balances held at the Fed have been moving lower since peaking in April. They are likely to continue to head lower over time as the Fed continues with its quantitative tightening program, even though it is at a reduced pace. Reserves have declined to around $3.265 trillion as of September 4 from a peak of about $3.6 trillion in March.

Bloomberg

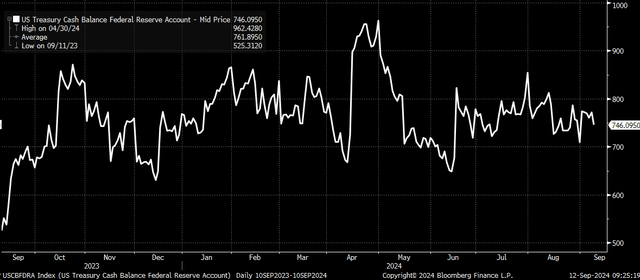

Over the short term, the Treasury General Account will likely surge towards the Treasury’s target of about $850 billion by the end of the quarter. This is based on the Treasury’s estimates on July 31 when it released its Marketable Borrowing Estimates. This would suggest that the Treasury general account rises by around $100 billion from its value of $746 billion on September 10 over the next couple of weeks. The bulk of the increase will come from the collection of quarterly taxes due the week of September 16. The Treasury General Account is a liability on the Fed’s balance sheet, and when the TGA rises, it draws down bank reserves.

Bloomberg

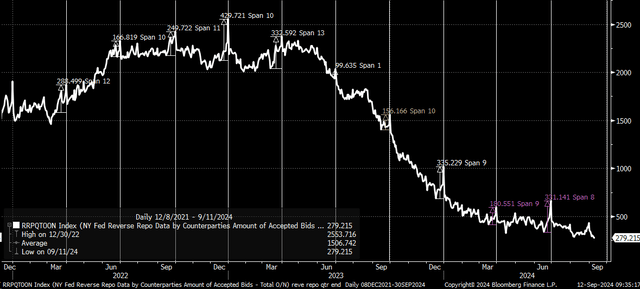

Furthermore, as we move into the second half of September, the usage of the reverse repo facility is likely to increase significantly, as we historically do around the quarter end. The balances can rise by around $200 billion in the final week of the quarter. The reverse repo facility is also a liability on the Fed’s balance sheet, and when it rises, reserve balances held at the Fed decline as well.

Bloomberg

This would suggest that reserve balances could decline by around $300 billion over the final two weeks of September. This would bring total reserves down to around $2.9 trillion to $3.0 trillion if the TGA and Reverse Repurchase facility increase as expected based on historical trends and guidance.

Reserves And Their Link To Assets

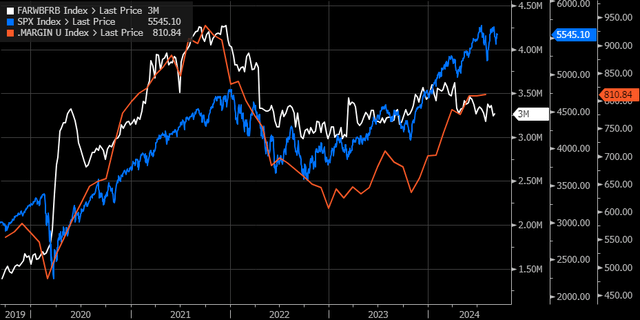

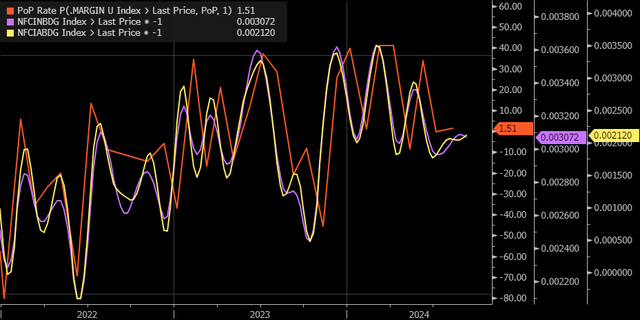

Changes in reserve balance have historically been linked to changes in Margin balance in the equity market. When reserve balances have increased, margin balances have increased, leading to more liquidity in the market and higher asset prices. When reserves have fallen, margin balances have declined, leading to lower equity values. Therefore, one would expect that as reserve balances fall during the final two weeks of September, we could see margin levels reduced over that same period. The declining margin balances would likely lead to reduced asset values.

Bloomberg/ FINRA

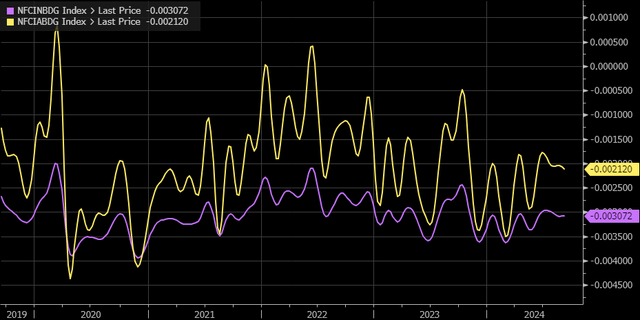

While access to FINRA only releases margin balance data monthly, the Chicago Fed National Financial Conditions Index provides weekly data on margin balances regarding whether conditions are easing or tightening. It potentially gives a view into changes in margin level on a weekly basis and whether the changes in reserves are indeed impacting margin balances in the market. The data shows that over several weeks, margin balance financial conditions have been relatively unchanged.

Bloomberg

Examining changes in margin balances monthly and then comparing those to the inverted changes in margin financial conditions shows that both track each other closely. When coupled with the overall declines in the size of the reserve balances, this suggests that margin balances in August were likely unchanged or saw a minimal change.

Bloomberg/ FINRA

BTFP

In addition, a factor over liquidity conditions over the next couple of weeks will be the continued decline of the Bank Term Funding Program, which currently stands at roughly $98.3 billion after peaking at around $170 billion in March. The BTFP has been draining at a reasonably predictable pace and could begin to drain at a face pace as the program overlaps with last year’s increase. This is likely to add some stress to the reserve balances over the next couple of weeks as well, as this value is unlikely to rise and should only continue to decline.

Bloomberg

If the reserve balances drop over the last two weeks of September, as based on historical trends seems likely, then we are likely to see more volatility in the market over the final two weeks of the month. This can be easily tracked since the reverse repo facility numbers are updated daily by the New York Fed at 1:15 PM ET, and the Treasury releases the value of the Treasury General Account daily with a one-day lag at 4 PM ET.

If the reserves drop as expected over the final two weeks of September, asset values could further decline.

Credit: Source link

{kind=link}