Douglas Rissing

The Federal Reserve let money flow into bank accounts last week, presumably to help keep any market pressure off of the Fed’s policy rate of interest, which the Fed just raised a week ago.

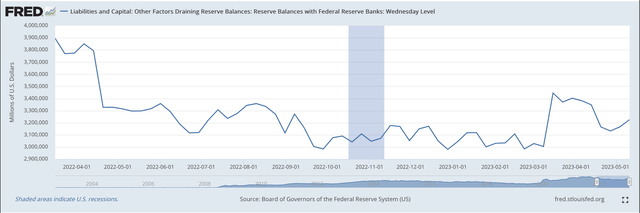

Reserve Balances with Federal Reserve Banks (Federal Reserve)

As one can see from the chart, the Federal Reserve has been reducing the amount of excess reserves that exist in the banking system ever since it began to quantitatively tighten up on monetary policy in the middle of March 2022.

The Federal Reserve stopped this reduction in reserve balances in early March as the commercial banking system began to experience some trouble. The trouble ended up with several commercial banks failing.

But, one can see from the chart that the Fed reacted in early March 2023 by overseeing reserve balances with commercial jumping up in March.

As the disruption to the banking system seemed to wane, the Fed allowed reserve balances to fall again.

However, in the past two weeks, the Fed has seen these balances rise once again. The movement of money into the banking system came from the Fed’s reduction in its General Account at the Fed and with a decline in reverse repos. Overall, almost $60.0 billion moved from the Fed’s balance sheet back into the banking system.

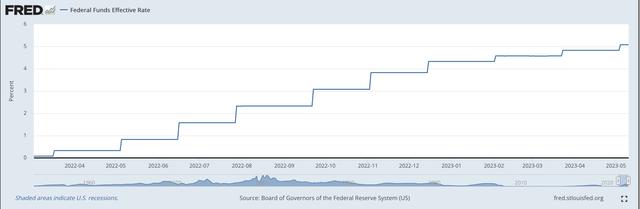

The effective Federal Funds rate remained steady at 5.08 percent during the past banking week.

Effective Federal Funds Rate (Federal Reserve)

Securities Portfolio

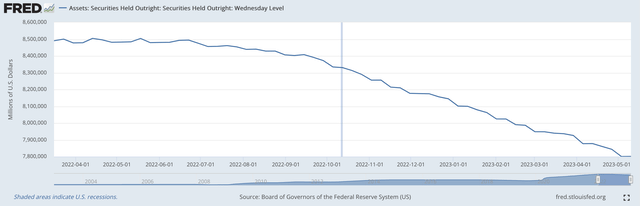

Very little change took place in the Fed’s securities portfolio last week.

In fact, the total securities portfolio rose only by one-half a billion dollars.

Since March 16, 2022, the whole securities portfolio has declined by right around $700.0 billion.

There are no signs that the Fed’s efforts at quantitative tightening are changing.

Here is the picture of the decline in the Fed’s securities portfolio.

Securities Held Outright (Federal Reserve)

Quantitative tightening has gone on now for just about 13 months.

It is my feeling that this quantitative tightening has gone on far longer than many investors thought would take place. These investors kept believing that the Federal Reserve would back off from the reduction in its securities portfolio.

They believed that the Fed would “pivot” because of market pressures.

Well, it hasn’t happened yet. But, this is what quantitative tightening is all about.

M2 Money Stock

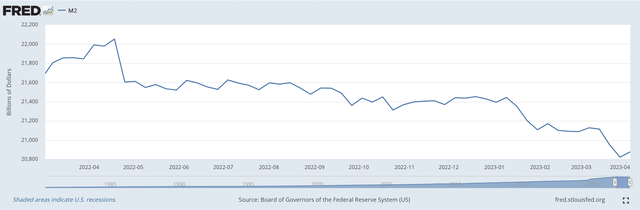

One other story here, the M2 measure of the money stock continues to decline.

M2 Money Stock (Federal Reserve)

From April 18 2022 through April 3, 2023, the M2 money stock has declined by 5.3 percent.

This is not an insignificant number, and the fact that the decline has carried on for a year should raise some eyebrows.

How Tight Is The Banking System?

But, is the Federal Reserve really having an impact on the banking system and is the Federal Reserve really generating an economic recession?

This question is very relevant to the current situation.

The article I posted yesterday addressed this issue.

In the first quarter of 2023, the U.S. commercial banking system posted the most profits in any quarter in history. It did this with banks failing, with the Federal Reserve using quantitative tightening for a full year, and with lots and lots of publicity about what is going on in the banking system.

The truth is that the U.S. commercial banking system still has lots and lots of money “hanging around.”

The Federal Reserve, in combating the spread of the Covid-19 pandemic, generated a huge “asset bubble.”

This “asset bubble” got the U.S. banking system through the pandemic and the economic recession that followed.

But, then, inflation began to show its head.

And, the Federal Reserve responded by raising its policy rate of interest and by entering into a round of quantitative tightening.

But, as I argued in yesterday’s post, the commercial banking system still has a massive amount of “cash” around…about $3.0 trillion of cash assets on bank balance sheets.

The largest banks in the country have massive amounts of cash on their balance sheets.

And, the Fed has, so far, reduced its securities portfolio by only a mere $700 billion.

Is this really tightening?

Especially within the largest commercial banks in the country.

The largest 25 commercial banks in the country have $13.1 trillion in assets as of the last week in April.

These commercial banks hold cash assets amounting to 11.5 percent of these assets.

These large banks, starting with JPMorgan Chase & Co., produced huge amounts of profits in the first three months of 2023.

The 13 months of quantitative tightening seem to have done very little to reign in the performance of these large banks.

Yet, many other banks, especially some of the larger regional banks, seem to be stretching to stay alive.

Is the Fed’s tightening really doing the job the Fed set out to do?

We have got to keep watching this situation very closely.

It seems as if the largest banks in the U.S. banks took advantage of the Fed’s asset bubble, but, unlike the banks that now seem to be in trouble, the largest banks protected themselves from the Fed’s attempt to reduce “the bubble.”

So, the largest banks, especially JPMorgan Chase & Co. (JPM), seem to be doing very well, while many others are caught in the twist generated by the Fed to bring inflation under control.

Credit: Source link

{kind=link}