Paul Souders

My last article was about WEG (OTCPK:WEGZY), an excellent Brazilian company that stands out for its track record of growth, solid moats, and very positive profitability indicators, which is why it is trading at multiples well above companies like Microsoft (MSFT) and NVIDIA (NVDA).

WD-40 Company (NASDAQ:WDFC) has some similar characteristics. It has clear competitive advantages, a very good growth track record (with a CAGR of close to 6% of revenue), and an ROIC of 24%. The double-edged sword is that all this is built on one product, WD-40. This product is known worldwide and used in different industries, and as it is well-established, it adds a vision of resilience.

At the same time, the company becomes dependent on this product and the ecosystem built around it, and even though the risk is somewhat distant and intangible, it is still a risk. All this is made worse by an unattractive valuation, which is even worse than WEG’s and with lower growth.

That said, despite being a good company and a compounder in its financials, its valuation makes the prospect of shareholder returns low, making WDFC stock a “sell” in my view, due to the opportunity cost.

WD-40 Company Has A Strong Brand With Solid Business Model

Even if you don’t work in industries that need WD-40, it’s hard not to know the WD-40. Its product is a multi-use used by professionals and amateurs alike to protect, lubricate, and clean a list of things. This brand strength is one of the factors that the company itself puts on the “Why Invest” page, also positioning it as the brand leader in the category.

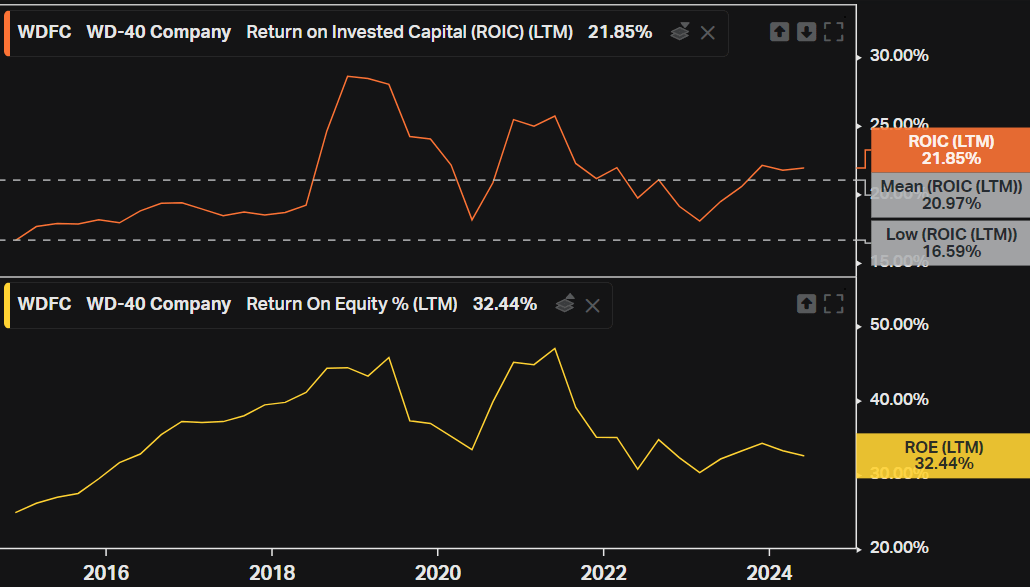

Not only that, but its business model also has other advantages, such as being asset-light, which manages to generate a lot of cash and still has room to maintain a high return on invested capital (above 20%). Over the last 10 years, the mean ROIC has been 21%, with some of the worst times reaching 16.6%.

Koyfin

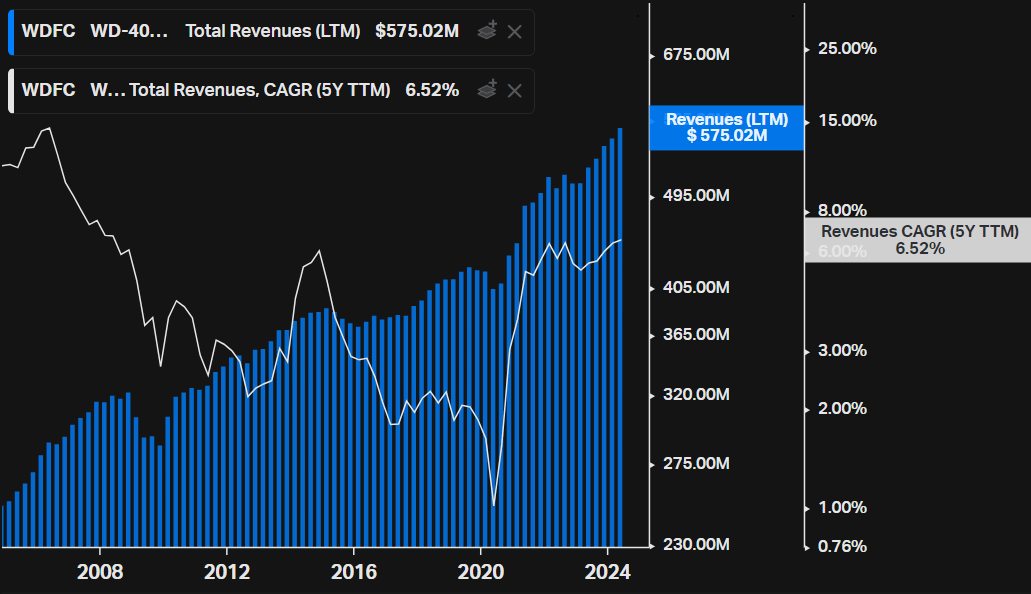

Over the last 20 years, WD-40 Company has managed to consistently grow its net revenue, reinforcing the excellent work of expanding into new industries and geographies, expanding into other product lines, and passing on price increases to customers, the 5-year CAGR of revenue is 6.5%, a level that is not so high, but draws attention for its consistency. What’s even more interesting is that the company has done this with basically an ecosystem around one product, WD-40, which if you consider WD-40 Multi-Use and Specialist, represented 90% of all revenue in the Americas, while the other 10% are other product lines focused on maintenance or Homecare and cleaning.

Koyfin

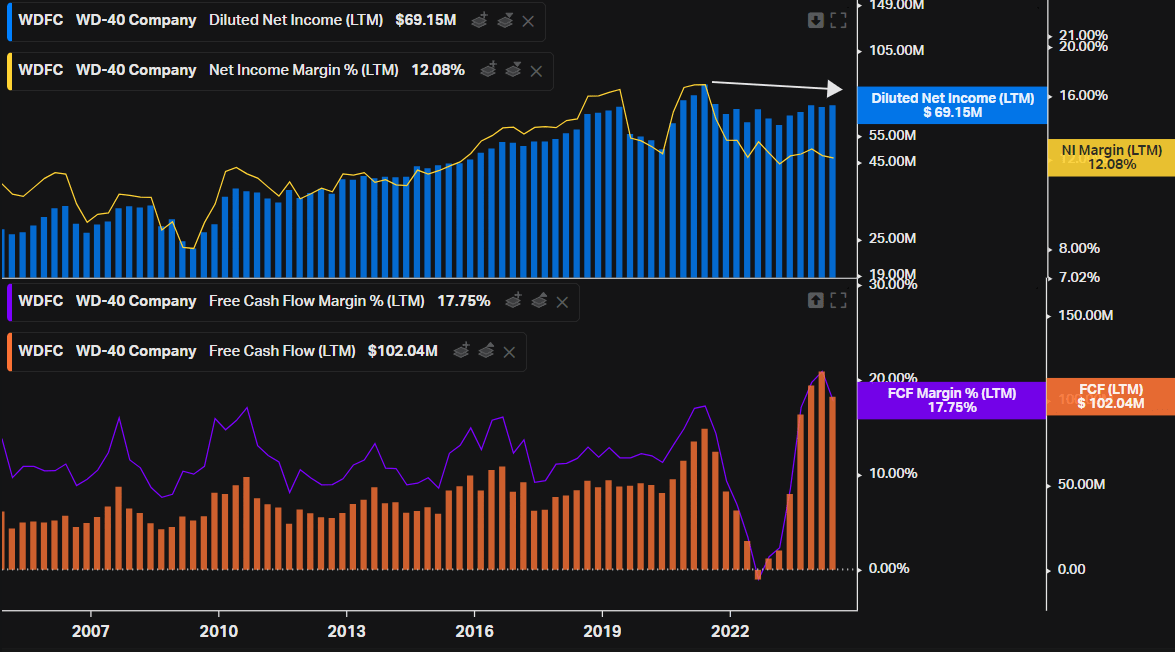

From this revenue, the company is able to make a good net profit and generate good cash flow. The net income margin has fallen in recent quarters, which means that net income has remained stable even though revenue is growing, although it is still at an interesting level. The free cash flow margin is approximately 17.7%, with free cash flow improving in recent quarters and highlighting the low need for capital expenditure. In the last 12 months, while revenue was $575 million, CapEx was only $5.58 million, highlighting the asset-light business model.

Koyfin

In short, the company manages to generate a good and sustainable result through its clear long-term competitive advantages, such as its category-leading recurring use product, which is very well established and still protected by trade secret.

WD-40’s Growth May Be Slow, But It Is Steady

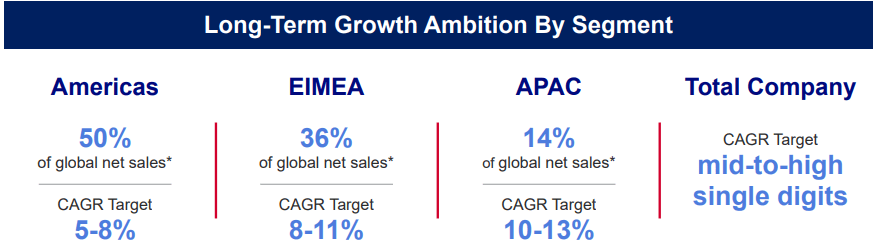

The WD-40 Company has interesting prospects for the coming years. Even though it is already well-established and present in most parts of the world, there is still room for reasonable and gradual growth. The company lists four main avenues for growth, which are geographic expansion, accelerating premiumization, the growth of the WD-40 Specialist line, and finally, Turbo-Charge Digital Commerce. This seems quite feasible based on the company’s track record, as it should enable improved margins with better digital efficiency, scale in new regions, and the like.

However, it’s more likely that this growth won’t be so high when analyzed on a consolidated basis. Its revenue is already almost $600 million, and without new product lines or some truly transformational innovation, it will be difficult to achieve growth above double digits for long in its main markets. On the other hand, as it is the company’s own target in the EIMEA and APAC region, it is possible that growth will be closer to the low-double digits.

WD-40 IR

In any case, when consolidated, the company’s target is something very similar to its historical revenue CAGR: mid-to-high single-digit growth.

It’s worth mentioning that despite the ‘A’ in Growth Grade, the company ends up with projections for some indicators below the sector median, such as diluted EPS growth (forward) of 5.08% against 6.96% in the market, and forward EBITDA of 6.03% against 6.07% in the market. But it wins in revenue growth forward, with 5.94% against 3.29%.

If constant, this mid- or high-single-digit growth is not to be underestimated in the long term, since by compounding revenue at this rate and on a constant basis, it is already possible to reach very high levels and still with a high degree of security due to the solidity of its business model and product.

WD-40’s Price Is Too High For Its Growth Rate

The bad part of the thesis is definitely the valuation, and that’s what makes the rating a sell. Revenue growing steadily at a rate of 6% or even 8% is quite interesting, especially if we consider possible positive surprises or small margin advances. But this fades away when we see that the current price of WDFC stock is already pricing that and a bit more.

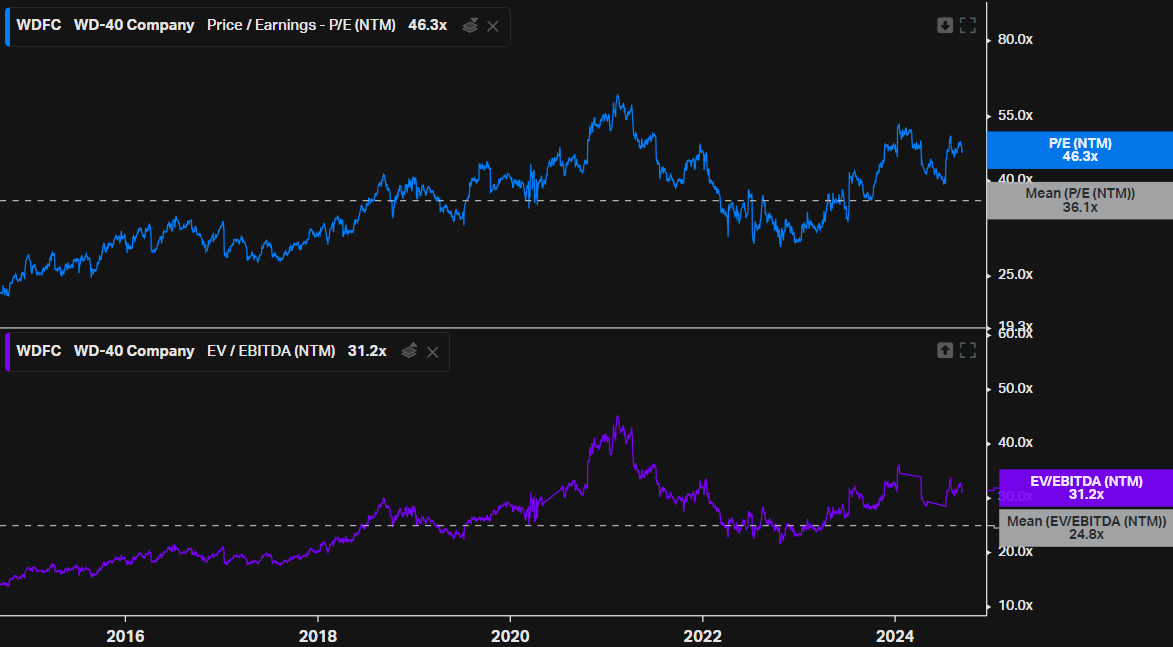

Currently, the NTM price-to-earnings is at 46x, against its average of 36x over the last 10 years. The EV-to-EBITDA NTM doesn’t differ that much either, with a level of 31.2x against 24.8x its average of the last decade.

Koyfin

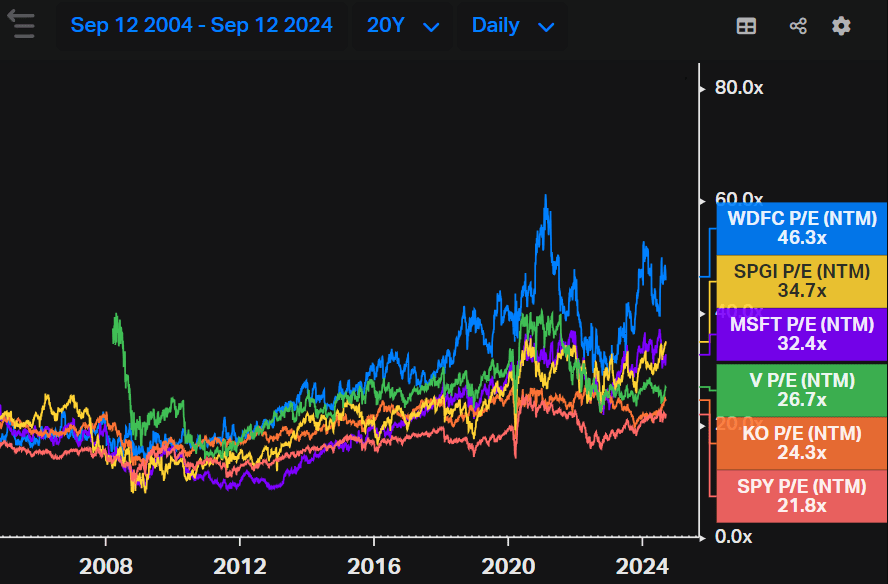

Historically, WDFC stock has not traded at low multiples, consistently trading above the market and other compounders. But it’s interesting to note how over the last 20 years, the NTM price-to-earnings gap has widened when comparing WD-40 Company to the S&P 500 (SPY) and other companies that I consider also to have clear competitive advantages and the ability to advance at a steady pace, such as S&P Global (SPGI), Microsoft, Visa (V) and Coca-Cola (KO).

Koyfin

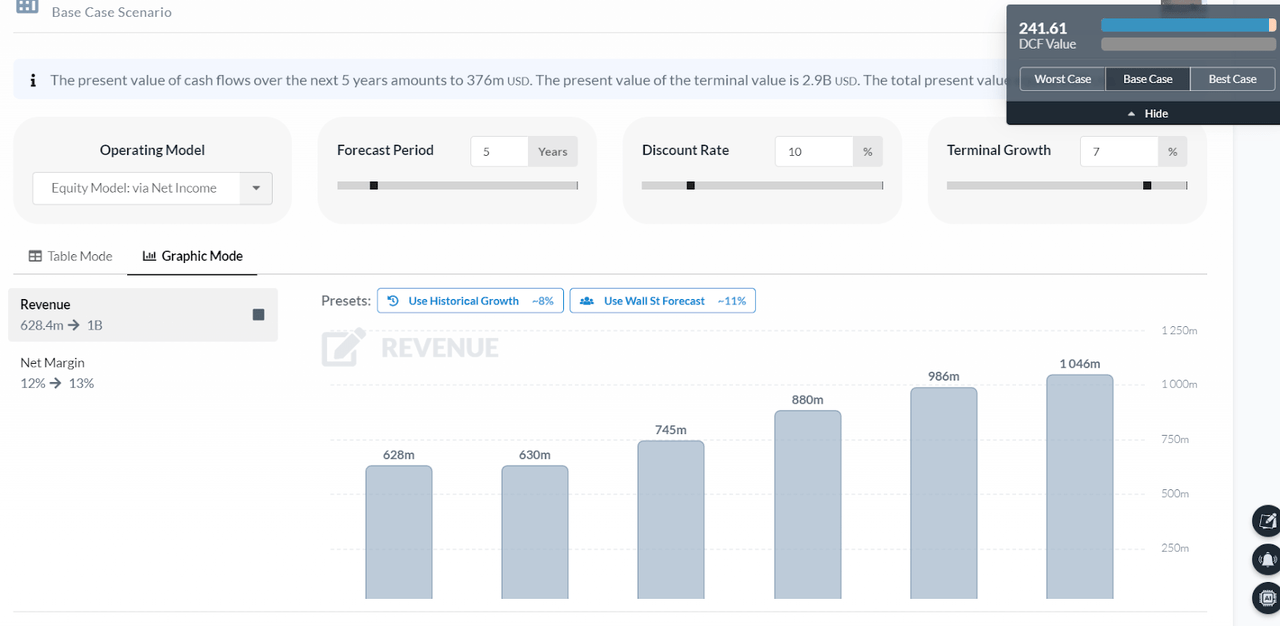

With a DCF model proxy (using net income instead of FCF for simplicity), it is also possible to ascertain that the market incorporates some optimistic assumptions for the market. Considering a growth of ~11% in revenue over the next few years, an increase in the net income margin of ~1 percentage point, and a terminal growth of 7% (which I consider to be quite high), we would still have an overvaluation of 4% when discounting at a rate of 10%.

AlphaSpread

Of course, this model is only an approximation of a Reverse DCF model, but it is already able to convey that the market adds high growth in the short term and either adds high terminal growth or discounts this flow at a low discount rate, rewarding the quality of its business model. In any case, the outcome is that the price to be paid for quality is too high, and ends up squeezing shareholder profitability.

Is it possible that the results will be even better than expected? Yes, but I wouldn’t pay such a high premium to see it because there are companies with a business model just as good (like some of those mentioned) and which also have growth prospects for the coming years, which generates a high opportunity cost.

The Bottom Line

In view of the above sections, I would summarize the WD-40 Company as an excellent one-product company (or product ecosystem). Its moats are wide, and the iconic brand, along with its power of scale and need for use, end up mitigating the risk of competition and the very dependence on being just one product.

On the other hand, all this ends up being overshadowed by a valuation that doesn’t match its future growth, which should be constant but between a mid- and high-single digit, while WDFC stock is trading at more than 46x projected earnings over the next 12 months. That’s why I think it’s hard to find room for WD-40 Company in a portfolio at current prices since the opportunity cost seems too high and other alternatives are just as good or even better, even though I recognize the high quality of the business.

Credit: Source link

{kind=link}