hapabapa

Warner Bros. Discovery (NASDAQ:WBD) is not for the faint-hearted. The company’s earnings are contracting due to declining linear TV viewership, it is also saddled with a mountain of debt.

The stock is cheap, though, very cheap! Warner Bros is trading at ~3.5x adjusted earnings and also owns a bunch of valuable intellectual property.

We initiated the coverage of Warner Bros. in June and are now revising our initial buy thesis after it was announced that the company will lose NBA broadcasting rights and as the economy has started weakening.

In our initial thesis, we estimated that Warner Bros will be likely to achieve its 3.0x leverage target by the end of FY2025, we no longer feel that this is reasonable to expect.

The risks behind this speculative investment have increased even further, and we no longer believe that it presents an attractive risk-return tradeoff. For the time being at least.

We are downgrading WBD due to this increased uncertainty.

EBITDA Development so far

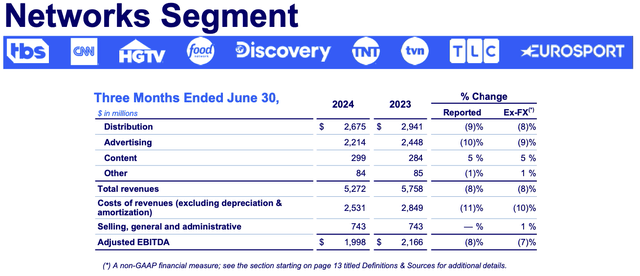

In the second quarter of this year, Linear Networks EBITDA is continuing to decline at high single digits, in line with our initial expectations.

Warner Bros

The advertising market was disappointing, as many had hoped that the presidential election would provide a boon to the industry. Unfortunately, significant domestic network audience declines and a weakening economy has resulted in lower ad prices.

So far, we see no sign that the decline in linear viewership would abate, and therefore we expect continuing EBITDA contraction in this division. The pace of decline will accelerate in the second half of 2025 as TNT will stop broadcasting the NBA.

TNT and NBA part ways

As it was broadly reported, the NBA has decided to transfer the broadcasting rights previously held by Warner Bros. to Amazon, once the current contract expires. Warner Bros was reportedly paying ~$1.2 billion for these rights and earning ~$600 million in profits.

The company will try to replace the NBA with other sports rights to maintain the carriage and fee rates, but we do not expect them to maintain the same level of profitability going forward. The NBA is a marquee property which will be impossible to replace, especially as the costs of sports rights are rapidly appreciating.

The price of WBD popped by 10% on the day of writing this, as the carriage deal with Charter was renewed and included TNT Sports. The two sides reached the new deal a year early, which is quite unusual given the intense recent negotiations with Disney and Paramount.

In a recent investor conference David Zaslav, the CEO of WBD, claimed that in the new Charter carriage deal, Warner Bros was able to maintain the price of TNT.

So we held the price on TNT. And in the aggregate for our cable business, we got paid more money for our 30 channels. And all of our channels are carried. We didn’t — there were no channels that were dropped.

Unfortunately, further financial terms of the deal were not disclosed. TNT’s price could have been maintained, but if TNT is now paying more for sports rights than before, a price increase would have been needed. It is also unclear if the new deal includes some provision concerning NBA litigation outcome.

We will therefore take a conservative stance and assume that the earnings of the Networks division will decline by ~$600 million per annum starting in FY2025. This decline will come on top of any ongoing structural decline.

Leverage targets could be reached by the end of FY2026, but strong Studios and DTC performance will be required

In our updated financial model, we assumed an acceleration in Networks’ decline during FY2025. We broadly expect the business to be able to generate about $4 billion of adjusted earnings and free cash flows per annum, and assume that all the cash will be dedicated to debt pay-down until the leverage target is reached.

We now expect Warner Bros to achieve its leverage target by the end of 2026, one year later than assumed before. The company could therefore begin paying dividends from about 2027.

|

FY2023 |

FE2024 |

FE2025 |

FE2026 |

|

|

Studios |

2,183 |

2,183 |

2,700 |

2,700 |

|

Networks |

9,063 |

8,338 |

6,921 |

6,367 |

|

DTC |

103 |

0 |

1,000 |

1,200 |

|

Corporate |

(1,242) |

(1,242) |

(1,242) |

(1,242) |

|

Inter-segmental |

93 |

0 |

0 |

0 |

|

Adj. EBITDA |

10,200 |

9,171 |

9,379 |

9,025 |

|

PP&E Depreciation |

1,097 |

1,097 |

1,097 |

1,097 |

|

Share-based compensation |

488 |

488 |

488 |

488 |

|

Adj. EBIT |

8,615 |

7,586 |

7,794 |

7,440 |

|

Interest expense |

2,221 |

1,995 |

1,785 |

1,560 |

|

Cash Taxes |

1,599 |

1,398 |

1,502 |

1,470 |

|

Adj. Earnings |

4,796 |

4,193 |

4,506 |

4,410 |

|

Market Cap |

17,000 |

17,000 |

17,000 |

17,000 |

|

Adj. PE |

3.5 |

4.1 |

3.8 |

3.9 |

|

Non-GAAP Net Debt |

39,901 |

35,707 |

31,201 |

26,791 |

|

Net Leverage Ratio |

3.9 |

3.9 |

3.3 |

3.0 |

|

Interest rate |

5.0% |

5.0% |

5.0% |

Financial statements and our estimates

We have to note that our assumptions include rather strong performance in Studios as well as DTC. While Studios should start emerging out of writers-related holdbacks in the second half of 2024, we are less certain about the ability of DTC to generate $1 billion in profits next year.

Studios to start recovering after writers’ strikes

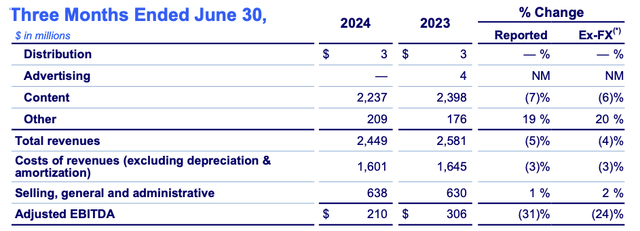

In the second quarter, Studios’ performance was rather weak, as the EBITDA of the division declined by ~30%. During the quarter, TV Studios’ revenue declined by 27% as the company worked through the last of the strike-delayed delivery.

Studios (Warner Bros)

A big swing-up is now expected in the second half as strike effects are fully cycled out. Due to disruption in the first half, Studios’ earnings might fail to reach the level of last year, FY2025 earnings should fully normalise, though. Before writers’ strikes, Studios were generating pro forma EBITDA of ~$2.7 billion, we would expect these profit levels to return.

Having said this, future growth prospects for the division are not entirely clear. Studios are producing content for other streaming platforms, though the content spending in the industry seems to be falling after a period of overspending.

Management seems to be focused on operational improvement rather than top-line growth.

DTC’s path to profitability through subscriber growth

Perhaps the greatest uncertainty to our financial model arises from DTC business earnings projections. Apart from Netflix (NFLX), nobody else in the industry is making money, while the profitability of Warner’s DTC division is artificially inflated due to the inclusion of HBO cable earnings.

So far this year, the Warner’s DTC division is breaking even, weighed down by higher content expenses from the allocation of U.S. sports costs. Incremental revenues, however, are expected to largely fall through to the bottom line as utilise content costs are scaled.

The Max revenues are growing due to international expansion, on the other hand, HBO is losing cable subscribers. International subscribers might have a lower average revenue per user, but price raises in the U.S. are keeping overall global ARPU stable at about $8.

The DTC business now has about 100 million subscribers, generates close to $10 billion of annualised revenues and is breaking even. To generate $1 billion of earnings this largely fixed-cost business would have to increase the top line by at least ~$1.5–2 billion.

Assuming stable pricing, another ~16 million subscribers will be needed over the next year and a half to hit the earnings target. This equates to about 2.6 million additional subscribers per quarter.

Max added 2 million subscribers in Q1 and 3.6 million in Q2, while David Zaslav has claimed that Max plans to add 6 million subs in Q3. So far, the DTC business is ahead of the plan due to the European rollout.

The ad market could weaken even further and derail deleveraging plans

The largest risks of Warner Bros.’s thesis might originate back home, in its core business. After all, the key risk factor of the company is not the ability of the DTC to grow but rather the declining revenues of the Networks’ and the company’s ability to deleverage.

Linear networks are losing viewers as DTC distribution and content are becoming more appealing. This is a structural trend which will continue.

Apart from secular industry decline, Warner Bros is also exposed to the advertising cycle. As the economy deteriorates the demand for ads falls, revenues can contract significantly. Since Warner is above safe leverage levels, even a temporary downturn could hurt them.

As of late, economic issues have started mounting as unemployment started rising and discretionary spending seems to be falling as pandemic savings have mostly been spent.

An economic downturn could cost Warner more than the loss of the NBA. As the economy becomes more challenging, the risks seem to be mounting.

The summary

Warner Bros. Discovery is a legacy traditional media company focused on production and direct-to-consumer content distribution.

The company is trading at only 3.5x adjusted earnings. However, it has a large debt load and needs to deleverage before reinstating shareholder returns. Deleveraging is made more challenging by the structural decline of the legacy linear business.

The financial impact of the loss of the NBA broadcasting rights is not yet certain, but will most likely be negative and accelerate Networks decline even further. An economic downturn could deal a further blow to the business and extend the deleveraging efforts.

The risks are mounting and we are no longer confident that Warner Bros. Discovery offers an attractive risk/return tradeoff.

Credit: Source link

{kind=link}