Mohamad Faizal Bin Ramli

Introduction

3M’s (MMM) desire to spin off its healthcare business has been rumbling on since July 2022 and was initially expected to close by the end of FY23; that did not come to pass, but the industrial conglomerate finally managed to get it over the line by the start of Q2 this year even though it still maintains a 19.99% share that will be monetized within the next five years.

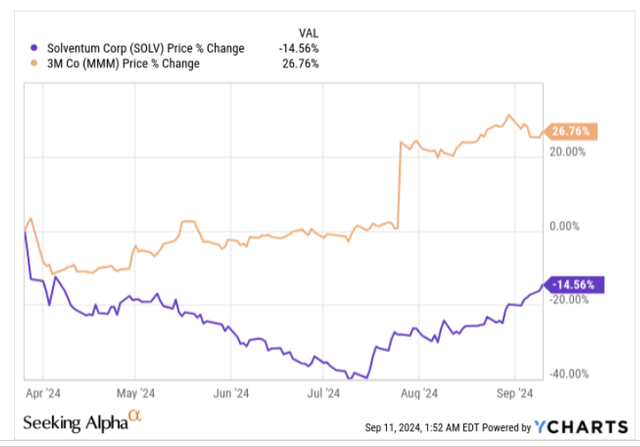

YCharts

Prima facie, the market appears to have liked what 3M has done here, as its stock is up by 27% since the spin-off, while Solventum (NYSE:SOLV), the now standalone healthcare business, which previously contributed a fourth of MMM’s business, is down by nearly -15% since the spin.

So, should investors continue to shun SOLV? Well after reviewing SOLV we feel it has some reasonably good qualities, but we don’t see any major incentive to rush in and buy the stock now.

Near-Term Challenges Are Unlikely To Abate Soon

At the outset, it must be stated that SOLV is in pretty good hands under Bryan Hanson’s stewardship. Of course there won’t be any magic wand to turn things around overnight, but Hanson has experience of being involved in the largest ever medtech spinoff- Covidien’s separation from Tyco. He’s also built a good understanding of this space during an 8-9 year tenure at Medtronic and Zimmer Biomet.

Structurally, SOLV also has some good qualities that won’t be easy to erode, such as market-leading positions in many categories, ownership of some strong brands, 100,000+ customers, deep commercial channel relationships in over 90 countries, and a decent degree of revenue diversification.

Nonetheless, as things stand, SOLV isn’t in the pink of health, and Hanson will have his task cut out for him, particularly in light of business continuity challenges following the spin. The new business now consists of four divisions, and it’s always going to be difficult for an organization to take it on the chin when its two largest divisions – MedSurg (56% of group sales), and Dental Solutions (16% of group sales) are witnessing contracting reported sales growth of -0.1% and -3.8% in H1.

Admittedly on an organic sales basis, the largest division has still seen +1% growth (the reported growth has mainly been affected by FX translation), but yet still, do also note that operating profits of MedSurg have come off quite significantly by -17%, whilst EBIT margins are down by nearly 400bps as of H1 (a similar cadence of margin declines have been noted with Dental Solutions as well).

The one division that is holding up rather well, is HIS or Health Information Systems (15% of group business), which has seen both reported, and organic sales trend up by 2% in H1, backed by EBIT margin progression of nearly 300bps. Much of HIS’s strength is being driven by the popularity of its integrated software system (360 Encompass) which leverages NLP capabilities to reduce inefficiencies and drive significant productivity benefits on inpatient and outpatient coding for its clients. To get a sense of how well-entrenched SOLV is in this space, note that over three-fourths of US hospitals currently employ at least one of the company’s HIS software solutions.

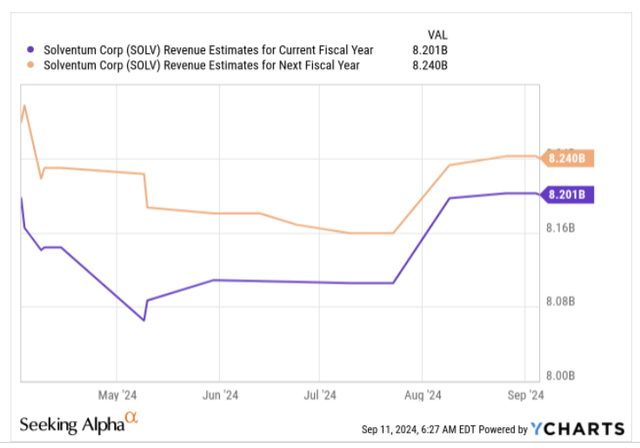

One can make some allowances for spin-related disruptions to business continuity, but all in all, as of H1, SOLV’s entire organic sales is up by just +1.1%. Worryingly, looking ahead to H2, things are expected to slow down (some of this is driven by tougher comps from Q3 last year), as management only expects FY24 organic growth of +0.5%. Even in FY25, the revenue outlook looks quite underwhelming, with consensus numbers implying just 0.5% growth for the year.

YCharts

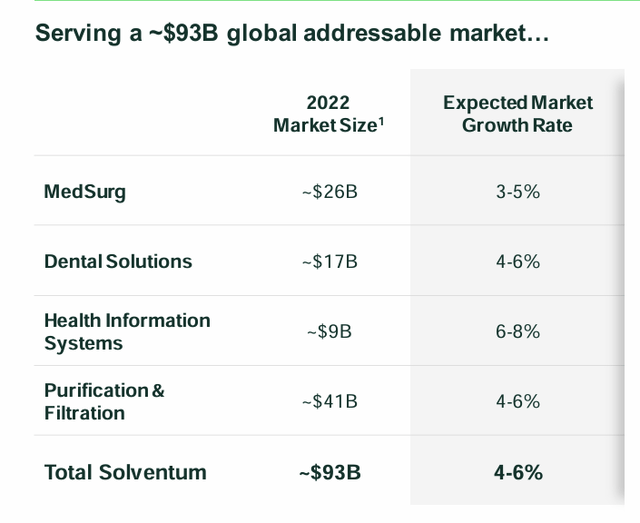

At less than 1% growth, it looks all but certain that SOLV will continue to lose share in a broad market that is expected to grow at 4-6% during 2024-2026.

Investor Day Presentation

The other important aspect to consider is that traditionally 3M’s health business has always been noted for its ability to facilitate robust cash flow; for context, over “each” of the last three years, it has generated over $1.6bn in operating cash flow, and $1.4bn in FCF. In light of its traditionally strong cash-gen qualities, many investors may have expected SOLV to offer a dividend, but that is not going to happen in the near future.

Besides, in H1-24, the pace of FCF generation has dipped (down by 14% YoY) but is still reasonable enough for a half at $637m. However, investors should not brace for another half of similar cash generation, as there will be a marked step-up in investments and CAPEX in H2 to help the company cope better as a standalone entity. Operating cash flow too will be impacted by various separation costs (more on that later). All in all, the FY FCF expectation is just for an underwhelming figure of $700-$800m, which would imply H2 FCF of just $60-$160m.

Even if the FCF position steps up next year, management has been very clear that the first 24 months following the spin will be focused on paying down its humungous debt load. To elaborate, SOLV currently has total financial debt of over $8.3bn, translating to 280% of its equity and 74% of its total capital. In contrast, other healthcare supply stocks typically have debt-to-equity ratios of 116% and debt-to-capital ratios of 35%.

Forward Valuations Don’t Look Prohibitive, But Are A Function of A Weak Earnings Outlook

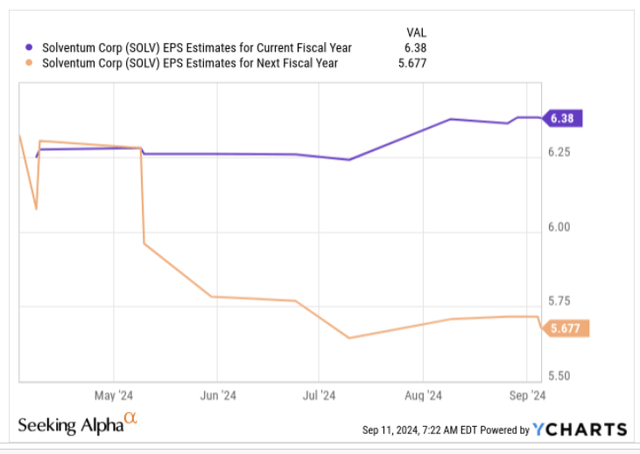

At the end of the Q2 results, SOLV management stated that they expect to hit an FY EPS within a range of $6.30 to $6.50. Consensus currently has an average figure that is a little closer to the low end of that range at $6.38, implying a valuation of 10.7x at current prices. Ideally, that multiple should light up your eyes, particularly when you consider that other healthcare supply stocks currently trade at a much steeper average forward P/E of 28.7x.

YCharts

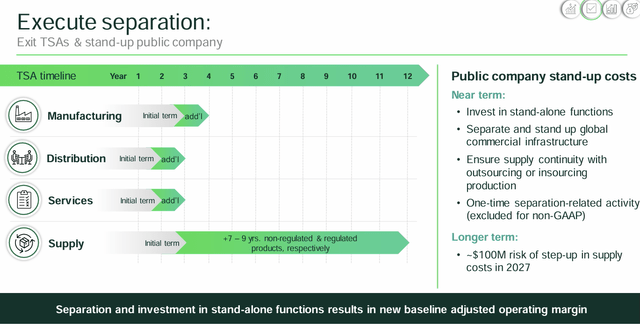

But do note that SOLV will face further earnings pressure next year, with earnings poised to decline by double-digits and come in at only $5.67. Traditionally, SOLV has been able to maintain operating margins of 25%, but is now poised to hit a lower threshold of 21-23%. Besides topline pressure, SOLV will have to deal with higher 3M supply agreement markups in the short-term, not to mention higher manufacturing, distribution, and services costs for the first 2-3 years as it establishes itself as a standalone entity. There’s also the additional risk of a $100m step-up in supply costs that could come into play by 2027.

Investor Day Presentation

Closing Thoughts – Technical Commentary

On the technical front, it is still early days, with less than half a year of price action, and the stock yet to establish any concrete resistance or supply zones.

Investing

However, what we can see from the daily chart is that the stock appeared to bottom out in mid-July, followed by a bullish cross-over where the 5DMA (black line) overtook the 20DMA (red line), signaling the start of bullish momentum. Following the signal, SOLV has made a cool 30% bounce back, but at these levels, it is worth pondering if some of the bullish momentum has gone overboard. We’ve now had eight straight sessions of higher highs and higher lows, but note that the RSI is now signaling overbought conditions, which raises the risk of a long position.

Credit: Source link

{kind=link}