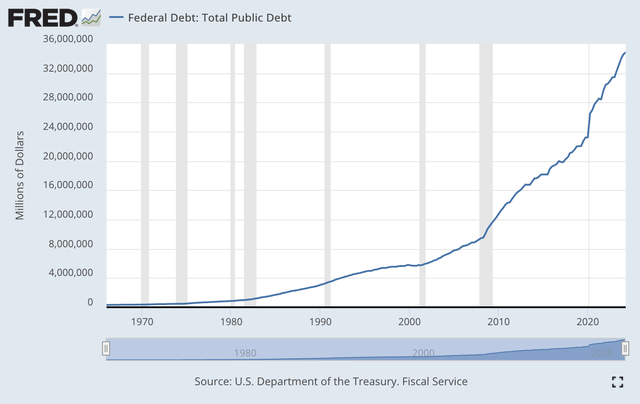

mphillips007 Total Federal Debt (Federal Reserve)

And, the future?

Look for $2.0 trillion annual additions, in the near future, to the debt.

And, there is so little talk about the deficit and the future of the deficit.

The U.S. national government has had its credit rating dropped once.

And, yet, no big deal is made out of the debt.

At one time, it seemed as if federal government spending and the government deficit were tools that contributed to the growth of the economy.

I see little or no connection of the federal government’s taxing or spending or the federal deficit contributing anything to the generation of U.S. economic growth.

The government’s “debt” accelerated after the Great Recession, and the acceleration has continued up to the present time.

And what did we get?

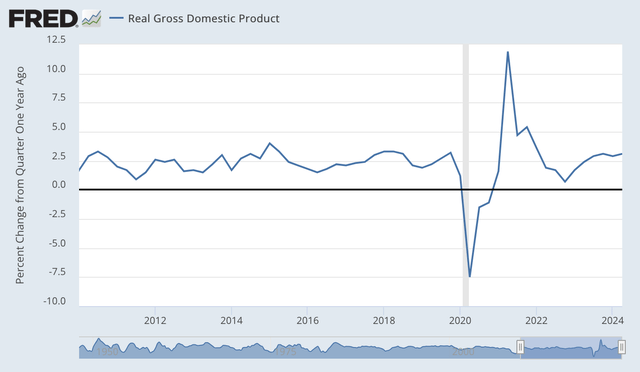

Real Gross Domestic Product–Year-over-Year Growth (Federal Reserve)

The average, year-over-year, rate of growth of real Gross Domestic Product from 2010 through 2023 was 2.28 percent.

The compound annual rate of growth of the U.S. economy during this time was 2.35 percent.

The compound annual rate of growth of the U.S. economy from 2010 to the beginning of the COVD-19 recession was 2.3 percent.

Note, that according to the National Bureau of Economic Research, the Covid-19 recession lasted for two months. It began in February 2020 and its trough was in April 2020.

Where has the U.S. government budget really made an impact on the growth of the U.S. economy during this time?

Also, if you smooth over the COVID-19 recession, we have had 15 years of pretty steady economic growth of about 2.3 percent.

The problem many economists have with these data is that the growth rate during this period of time was so low.

The desire was to have a growth rate closer to 3.0 percent.

The crucial thing to me, however, is that the growth rate has been so steady for so long. And, I am counting fifteen years in this viewpoint, basically because the recession was so short, was caused by an economic shock that quickly was overcome, and returned to much the same growth rate that existed before the recession.

And, there are other reasons for this last conclusion. The primary one is that the technology base of the U.S. has changed and that many businesses work on a time-pacing foundation that keeps innovation going and going and going in order to remain competitive.

This sector, during the recession, was able to “get money” and was able to “keep on going,” steadily during these years.

I work a lot in this space, and I have been thoroughly amazed at how this “innovative” output and growth got money and continued through the two-month recession without really stopping. It was an amazing time for me.

My conclusion from all this is that the economy is now being driven by the supply side.

Just look at the two charts.

In the first chart, the federal debt is going through the roof.

In the second chart, the U.S. economy is growing at a very steady pace.

What impact is the federal government spending achieving relative to the economic growth of the country, and what benefit is the economy getting from all the debt building up?

The U.S. credit rating has declined.

Now, don’t get me wrong. The government spending does some good things, and the federal government should do the things that contribute to the performance of different parts of the economy.

But, the evidence of the past 15 years is that the federal government does very little that contributes directly to the growth rate of the economy. The growth rate of the economy is primarily determined by the supply side.

The response of the federal government and the Federal Reserve System WAS important in minimizing the disruptions caused by the COVID-19 pandemic, but this, hopefully, was a one-time thing.

Given the “new” Ben Bernanke instituted format for the Fed’s monetary policy, it seems as if the U.S. economy can grow in a steady fashion, dependent upon the productivity coming from what is going on in the supply side of the country.

My conclusion…do something about government spending and the government’s financial management. The U.S. government must focus more on the financial position it presents to the world.

The federal government, the Federal Reserve System, manages the reserve currency of the world. It is now under challenge.

The federal government and the Federal Reserve must take responsibility for the U.S. maintaining this position. The U.S. dollar must continue to be number one in the world.

The federal budget and the federal debt must not put this dollar position into any danger.

This is vital for the investors in the U.S. but it is also vital for the businesses in the U.S.

The United States must continue to maintain the position of the U.S. dollar within the world. This must be a part of U.S. leadership.

Leaders are strong producers, but they also must maintain a strong financial position.

Budget deficits must be small, and must be controlled if the government is to maintain leadership.

Myself, I believe in balanced budgets.

President Bill Clinton and Treasury Secretary Robert Rubin are strong examples for me in this respect.

And, the economy was much better positioned in the world when they “ran the shop.”

The first chart presented in this article gives me a bad feeling.

To me, this chart makes investors very, very nervous.

We need to be talking more about the budget of the U.S. government.

Moving to budget deficits of $2.0 trillion or more is very, very short-sighted.

Moving to a debt level of $35.0 trillion is ridiculous, and thinking about $40.0 trillion is…well, you put it into your words… I can’t print mine.

Somebody has got to take this situation seriously.

Credit: Source link

{kind=link}