sculpies/iStock via Getty Images

This is an update on my last Upstart Holdings, Inc. (NASDAQ:UPST) article on 4th April ’23, “Upstart: Ready To Roar With A Newborn’s Heart.” That article detailed six major factors that had precipitated a vicious slide in the company’s market value. This article is an update that shows how each obstacle has been, either absolutely rebutted or largely mitigated, via the March ’23 Earnings released last night. The reader is strongly advised to revisit the article linked above, to grasp the significance of this quarter’s results.

Summary of March ’23 Earnings

-

Q1 total revenue was $103 million, a decrease of 67% from the first quarter of 2022, which hardly seems cause for cheer, even though it eclipsed consensus of $99.8m. But if one reflects on the regional banks’ turmoil during the quarter (a source of credit whose chaos was not evident when outlook announced in February), the revenue-beat is more creditable.

- The main surprise in the earnings was the major jump in contribution margin: 58% compared to a 47% in the same quarter of the prior year. The jump is due mainly to an optimization of “Sales and marketing” ($31m vs $133m YOY). If it wasn’t for a massive increase in “Engineering and product development” costs in the quarter, ($110m vs $49m YOY), the margin would have risen even further.

- Financial Outlook For the second quarter of 2023, Upstart expects Revenue of approximately $135 million with a Contribution Margin of approximately 60%. Here again we see only a slight revenue surprise from current consensus of $127m, but it’s the margin that’s impressive. This demonstrates the operating leverage within the company’s control; since the environment is intrinsically demand-constrained, Upstart can minimize its marketing budget and yet still achieve its revenue target.

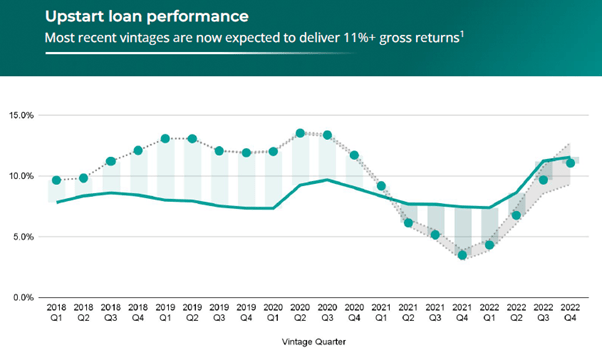

Integrity of AI Model

As any investor is aware, COVID created havoc with numerous economic variables. For Upstart, the impact was felt in the largesse of government assistance to consumers during the pandemic (resulting in default rates markedly lower than that predicted by their AI-model), followed by higher-than-expected default rates when government assistance was withdrawn. This created doubts in the model’s accuracy, as vintages in ’22 underperformed expected outcomes (see graph below).

Upstart accommodated this macro-economic uncertainty by the addition of the UMI (Upstart Macro Index) that can be adjusted to reflect adverse/beneficial changes expected on the macroeconomic front.

The latest graph shows how the accuracy of the model has improved, with the latest vintage forecasting risk with impeccable precision. This puts paid to any criticism that the model “only performs well in a declining interest-rate environment.”

Upstart Slide Deck

New Credit Flows Secured

A highly significant achievement was the progress Upstart made in securing long-term credit. As stated by the CEO in the release:

Despite the headwinds facing our industry, we secured multiple long-term funding agreements, together expected to deliver more than $2 billion to the Upstart platform over the next 12 months.

In simple terms, originators of credit can be regarded as an essential part of the company’s supply chain. It’s those credit flows that Upstart channels into consumer loans via their AI model that calibrates an appropriate risk-adjusted yield.

One could argue that $2bn is not that material, given this quarter yielded a mere $103m revenue when it originated slightly over 84,000 loans totaling just under $1 billion. However an analyst question in the Q&A section of the earnings call revealed these are new credit sources, secured during the quarter.

Analyst

Good afternoon. Thanks for the question. I just wanted to dig a little bit into the secured funding, the $2 billion. I just want to understand, is this – are these funds like securing minimums from existing partners, or is it incremental from new funding partners, if you could just provide a little bit more color on that and how it is compares to the existing run rate, I guess, of business that you have.

Sanjay Datta, CFO

Sure. Yes. Thanks, Pete. This is Sanjay. Yes, I think a lot of it is coming from partners that are new to the platform that we’ve never worked with before. Some of it is coming from existing partners who had either sort of stepped away from funding during the sort of turbulence the past few quarters and are coming back to the platform or they’re re-upping in significant size and committing forward in exchange for the longer-term agreement.

So I think in almost every case, you can view it as sort of being additive to what we’ve been doing recently and sort of underpins the – both the improving guide that we have in our Q2 numbers as well as its sort of more general optimism we’re signaling qualitatively.

Valuation

There has been no need to make any valuation changes in my model. From my previous article, I compiled a simplistic earnings model for 2024 that used 2021 as the best proxy for 2024, being a year before acute rate volatility and when credit flowed somewhat smoothly. The adjustments made (when comparing 2024E to 2022 & 2021) reflected cost containment (20% of staff laid off in 2022), and management’s decision to limit development of new ventures for the near future. This delivered a fully-diluted eps estimate of $2.12 for 2024. The latest results increase my conviction in the forecast.

From 2024, Upstart should be able to grow revenue and earnings at a rate of, at least, 20% per annum, as the superiority of its AI-model begins to gain acceptance in a vast market estimated to be $162Bn for consumer loans. This revenue growth rate merits a PEG ratio of at least 1x; using a P/E of 20 provides a share price of $42 by the end of 2023, after which the share price will move in tandem with earnings growth of 20% pa.

Upstart has overcome the perfect storm over the last year – the share price slide reflects the havoc caused. The March ’23 results offer strong evidence the worst is behind the company, and the first green shoots of recovery are in plain sight.

The latest short report shows a 3.4 m reduction (April 14, 2023) in the short ratio – that’s quite a move in 4 weeks. Yet the share is still very prone to a short squeeze, given the 32% short relative to the float.

Strong Buy on Upstart Holdings, Inc.

Credit: Source link

{kind=link}